DSNews The homepage of the servicing industry

DSNews The homepage of the servicing industry

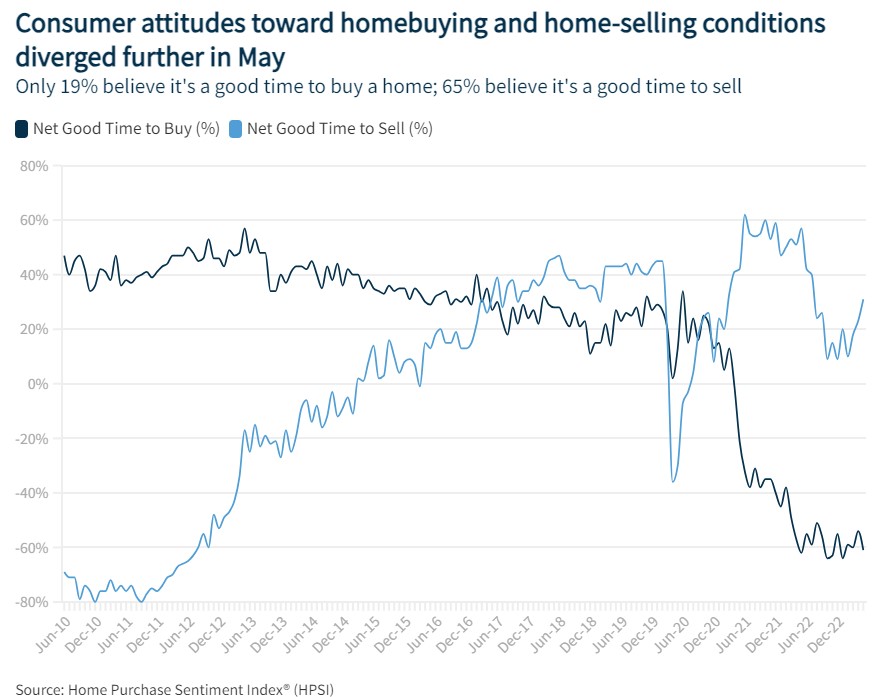

According to the latest Home Purchase Sentiment Index (HPSI) published by Fannie Mae, the index decreased 1.2 points in May 2023 to an index level of 65.6 due to affordability constraints continue to color consumers’ perceptions of homebuying and home-selling conditions.

According to the latest Home Purchase Sentiment Index (HPSI) published by Fannie Mae, the index decreased 1.2 points in May 2023 to an index level of 65.6 due to affordability constraints continue to color consumers’ perceptions of homebuying and home-selling conditions.

Of the six major components of the index, four decreased on a monthly basis, notably in the “good time to buy” and “good time to sell” categories in which survey respondents pushed down the good time to buy metric to near all-time lows.

However, the good time to sell component increased in May to its highest level since July 2022. And for the second month, a greater share of consumers indicated that they expect home prices to increase over the next year.

On a yearly basis, the full index is down 2.6 points. The index was benchmarked to 100 based on housing market activity in June 2010.

By the numbers, the six major components of the index revealed:

- Good/Bad Time to Buy: The percentage of respondents who say it is a good time to buy a home decreased from 23% to 19%, while the percentage who say it is a bad time to buy increased from 77% to 80%. As a result, the net share of those who say it is a good time to buy decreased 7 percentage points month-over-month.

- Good/Bad Time to Sell: The percentage of respondents who say it is a good time to sell a home increased from 62% to 65%, while the percentage who say it’s a bad time to sell decreased from 38% to 34%. As a result, the net share of those who say it is a good time to sell increased 8 percentage points month-over-month.

- Home Price Expectations: The percentage of respondents who say home prices will go up in the next 12 months increased from 37% to 39%, while the percentage who say home prices will go down decreased from 32% to 28%. The share who think home prices will stay the same increased from 31% to 33%. As a result, the net share of those who say home prices will go up increased 6 percentage points month-over-month.

- Mortgage Rate Expectations: The percentage of respondents who say mortgage rates will go down in the next 12 months decreased from 22% to 19%, while the percentage who expect mortgage rates to go up increased from 47% to 50%. The share who think mortgage rates will stay the same remained unchanged at 31%. As a result, the net share of those who say mortgage rates will go down over the next 12 months decreased 5 percentage points month-over-month.

- Job Loss Concern: The percentage of respondents who say they are not concerned about losing their job in the next 12 months decreased from 79% to 77%, while the percentage who say they are concerned increased from 21% to 22%. As a result, the net share of those who say they are not concerned about losing their job decreased 3 percentage points month-over-month.

- Household Income: The percentage of respondents who say their household income is significantly higher than it was 12 months ago decreased from 24% to 20%, while the percentage who say their household income is significantly lower increased from 11% to 12%. The percentage who say their household income is about the same increased from 64% to 67%. As a result, the net share of those who say their household income is significantly higher than it was 12 months ago decreased 5 percentage points month-over-month.

“As we near the end of the spring homebuying season, the latest HPSI results indicate that affordability hurdles, including high home prices and mortgage rates, remain top of mind for consumers, most of whom continue to tell us that it’s a bad time to buy a home but a good time to sell one,” said Mark Palim, Fannie Mae VP and Deputy Chief Economist. “Consumers also indicated that they don’t expect these affordability constraints to improve in the near future, with significant majorities thinking that both home prices and mortgage rates will either increase or remain the same over the next year.”

“Notably, the same factors impacting affordability may also be affecting the perceived ease of getting a mortgage,” Palim concluded. “This was particularly true among renters: 81% believe it would be difficult to get a mortgage today, matching a survey high.”

Click here to view the HPSI in its entirety.