DSNews The homepage of the servicing industry

DSNews The homepage of the servicing industry

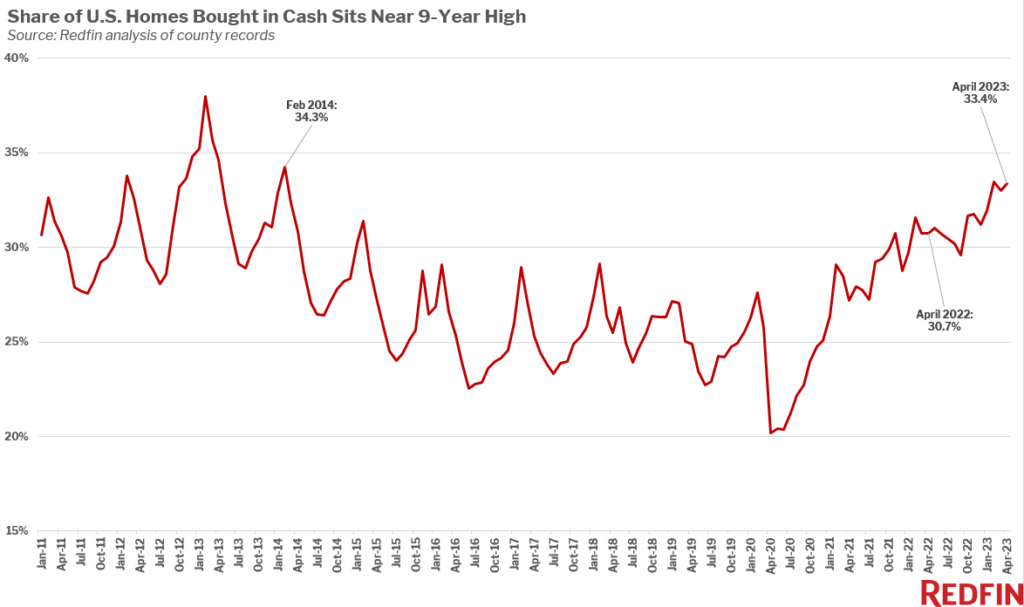

One-third—an estimated 33.4%—of U.S. home purchases were made in cash in April, up from 30.7% a year earlier and the highest share in nine years, according to a new report from Redfin.

All-cash purchases are making up a bigger portion of the homebuying pie, as elevated mortgage rates are deterring homebuyers who take out mortgages more than they’re deterring all-cash buyers. Overall home sales were down 41% from a year earlier in April in the metros included in Redfin’s analysis, which comprised 40 of the most populous U.S. metros. That’s compared with a 35% decline for all-cash sales.

Mortgage rates are near their highest level in 15 years, sidelining many would-be homebuyers—especially those who need to take out a mortgage. However, high rates can also deter all-cash buyers because they may decide their money is better spent on investments that benefit from high rates—like bonds.

“A homebuyer who can afford to pay in all cash is weighing two potential paths,” said Redfin Senior Economist Sheharyar Bokhari. “They can use cash to pay for the home and avoid high monthly interest payments, or take out a loan and pay a high mortgage rate. In that case, they could use the money that would have gone toward an all-cash purchase to invest in other assets that offer bigger returns, which could partly cancel out their high mortgage rate.”

Competition among homebuyers is a smaller but still noteworthy reason for the uptick in all-cash sales. A lack of homes for sale is prompting competition in some metro areas, motivating buyers to make all-cash offers to win homes.

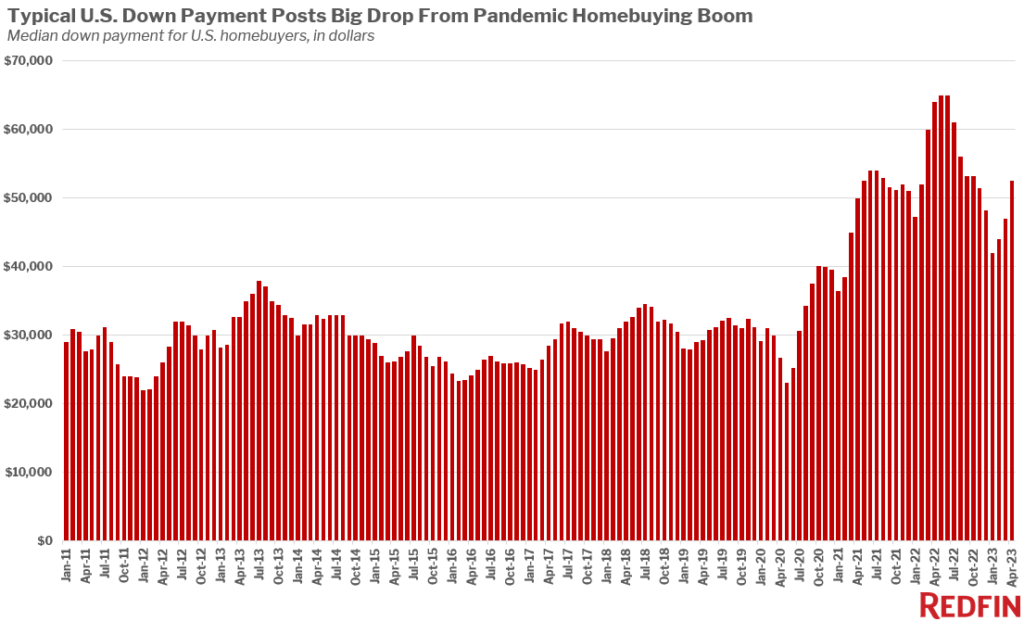

Down payments post one of the biggest drops since start of pandemic

The typical U.S. homebuyer’s down payment was $52,500 in April, down 18% from a year earlier. That’s the second-biggest drop since May 2020, when the housing market ground to a halt at the start of the pandemic (the biggest was a 22% drop in March 2023). Down payments have been falling on a year-over-year basis since November.

In percentage terms, the median down payment was equal to 13.1% of the purchase price, down from 16.5% a year earlier.

Even though the inventory shortage is causing more competition for homes than one might expect given today’s relatively tepid demand, the bidding-war rate is much lower than it was a year ago. Forty-six percent of home offers written by Redfin agents faced competition in April, down from roughly 59% a year earlier. Less competition means fewer buyers need to offer a big down payment to prove their financial stability and stand out from the crowd. It also means FHA loans, which require lower down payments, are becoming more prevalent.

The typical U.S. home sold for 4% less in April than a year earlier, and the drop is much bigger in some metro areas. Lower home prices mean lower dollar down payments.

Share of homebuyers using FHA loans hits highest share since before the pandemic

Roughly one in six—or 16.4%—U.S. mortgaged home sales used an FHA loan in April, the highest share since February 2020, just before the pandemic began. That’s up from 10.4% a year earlier; representing the largest year-over-year gain on record.

Just under 7% of mortgaged home sales used a VA loan, down from an eight-year high of 8% in February but up from 5.9% a year earlier.

Conventional loans are the most common type, making up more than three-quarters (76.8%) of mortgaged home sales. But the share of buyers using a conventional loan dropped from 83.7% from a year earlier, the biggest year-over-year decline on record. Redfin agents in pandemic homebuying boomtowns Boise, ID, Austin, TX, and Orlando, FL, report that they saw an uptick in FHA loans in early spring.

High mortgage rates may also make buyers more likely to choose an FHA loan instead of a conventional loan, as FHA rates tend to be slightly lower; the average daily FHA rate was 6.54% on June 6, versus 6.89% for a conventional loan.

Even though FHA loans are becoming more common, the fact that one-third of home purchases are made in cash reflects the unequal nature of today’s housing market. Affluent buyers who can afford to pay for a home in cash still have an advantage because not only is it easier to get offers accepted, but they don’t have to take on high mortgage rates.

“Buyers who can’t afford to pay in all cash also have two potential—but different—paths,” said Bokhari. “They can avoid a high mortgage rate by dropping out of the housing market altogether, or they can take on a high rate. That discrepancy is the reason the all-cash share is near a decade high even though all-cash purchases have dropped: Affluent buyers have the choice to pay cash instead of dropping out of the market.”

To read the full report, including more data, charts and methodology, click here.