DSNews The homepage of the servicing industry

DSNews The homepage of the servicing industry

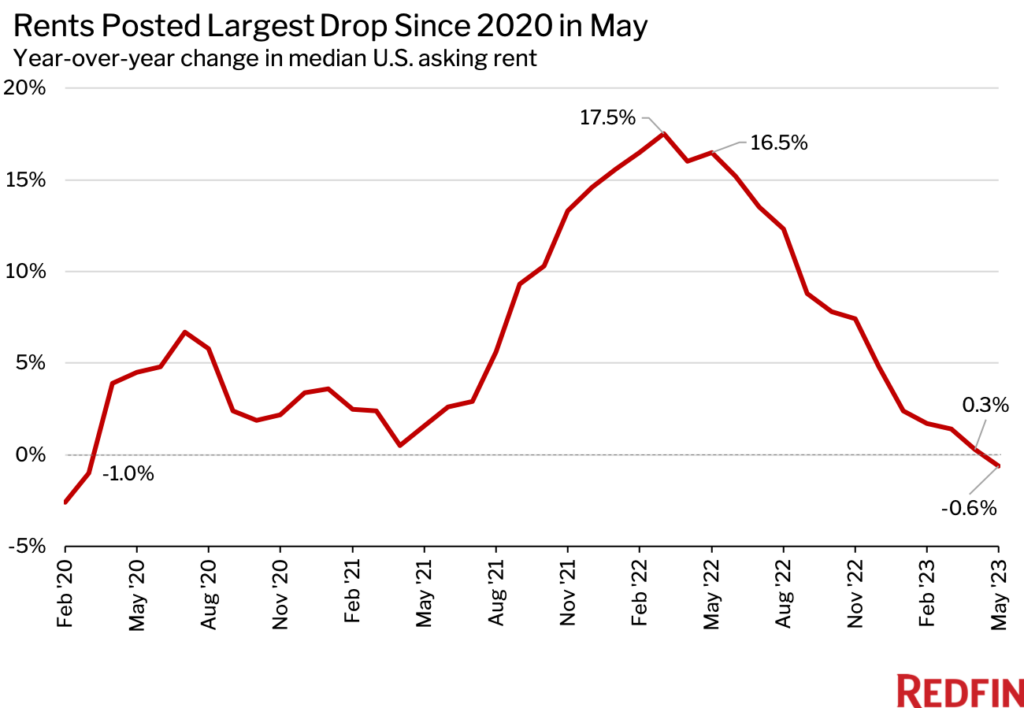

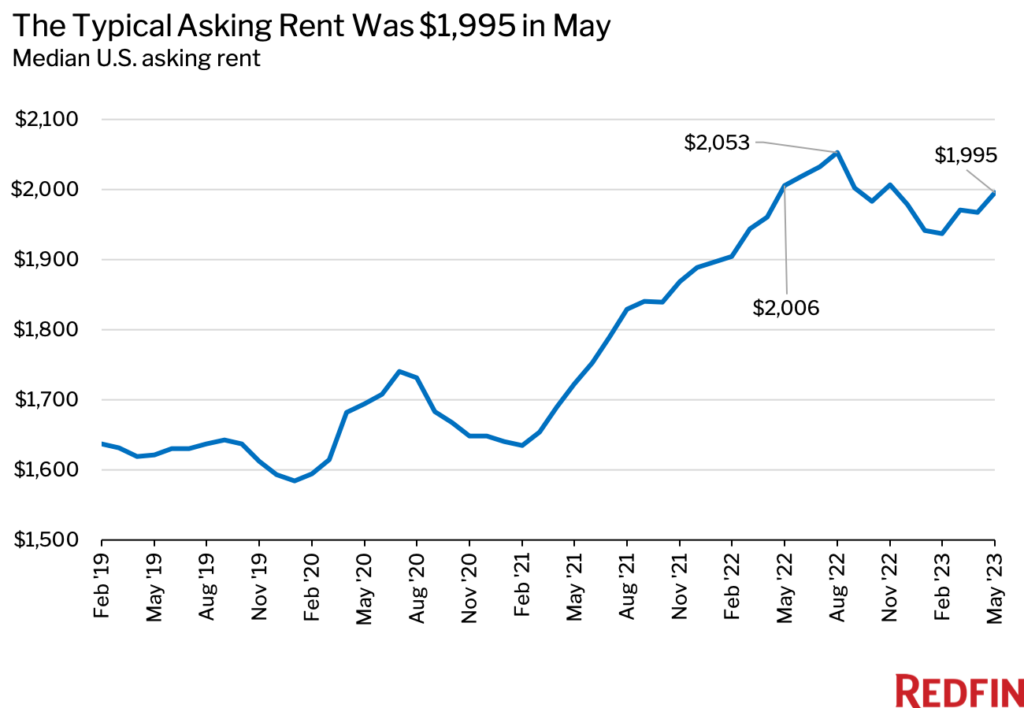

While housing supply remains on the upswing, the median U.S. asking rent fell 0.6% year-over-year to $1,995 in May—the largest annual decline since March 2020—according to a new report from Redfin.

That number compares with a near-record 16.5% increase one year earlier. May’s drop also represented the first annual decline since March 2020 on a revised basis. The median asking rent rose an overall 1.4% from a month earlier in May.

In the West, asking rents declined 2.1% from a year earlier—nearly four times the national pace. But other U.S. regions saw increases, with rents climbing 5.4% in the Northeast, 4.9% in the Midwest, and 0.8% in the South.

Rents have cooled in part because the number of rentals on the market has grown, giving landlords less leeway to hike prices because they’re grappling with a rise in vacancies as renters get more options to choose from.

One reason rental supply has been growing is many homeowners are opting to rent their homes out instead of selling. Some have already moved into their next home, and are renting their previous home out to cash in on still-high rents and continue building equity on a house with a relatively low mortgage payment. The average 30-year-fixed mortgage rate is 6.8%, up from 5.09% a year ago and a record low of 2.65% in January 2021. The average monthly payment is $320 higher than it was at this time last year.

“Many homeowners are deciding that instead of selling, they’re going to renovate their current home or rent it out while they wait for the market to improve,” said David Orr, a Redfin Premier real estate agent in Sacramento, CA. Some homeowners are likely waiting for housing prices to bounce back so they can make a larger profit when they do sell.

Rental supply has also increased because America has been building more multifamily housing. Completed residential projects in buildings with five or more units rose 24.2% year-over-year on a seasonally-adjusted basis to 400,000 in April—the most recent month for which data is available. This is likely part of the reason the rental vacancy rate has ticked up; it was 6.4% in the first quarter—the highest level in two years.

While a building boom has driven up the number of rentals on the market, the boom is slowing. The number of permitted residential projects in buildings with five or more units fell 22.9% year-over-year on a seasonally-adjusted basis to 503,000 in April. Permits, or approvals given by local jurisdictions to start construction projects, are a leading indicator of what’s happening in the housing market. Completions are a lagging indicator. Still, there remains a backlog of under-construction rentals that have yet to hit the market, meaning rents likely still have room to fall.

Finally, rents have eased because fewer people are moving due to economic uncertainty, slowing household formation, still-high rental prices in many markets, and the rising cost of other goods and services due to inflation.

While asking rents fell from a year earlier in May, they were still only 2.8% below their August peak of $2,053, meaning many renters are still taking on high rents. That isn’t the case in every market, though; in areas where rents are cooling more, renters are more likely to get deals and concessions from landlords.

Rents Are Falling in the West, Rising in the Northeast

In the West, the median asking rent fell 2.1% year-over-year to $2,409 in May. That’s the only region Redfin analyzed that saw an annual decline. Asking rents rose 5.4% to $2,495 in the Northeast, 4.9% to $1,406 in the Midwest and 0.8% to $1,663 in the South.

Rents are cooling fastest in the West and South in part because they rose so much during the pandemic as scores of people moved into places including Phoenix and Miami. Now, rents in those regions have relatively more room to fall as supply catches up with demand. Rent growth has been steadier in the Midwest, which is home to many relatively affordable markets.

The West is also seeing rents decelerate quickly because it is building a lot of multifamily housing, which means landlords in some areas are grappling with rising vacancies. There were 440,000 new non single family homes completed in the West in the first quarter, compared with roughly 200,000 in each of the other three U.S. regions. Expensive West Coast tech hubs like Seattle and San Francisco may also be experiencing rent declines due to remote work and tech layoffs.

Overall, experts predict rents will continue to moderate throughout the year, although economic uncertainty lingers for many homeowners and renters nationwide.

To read the full report, including more data, charts and methodology, click here.