DSNews The homepage of the servicing industry

DSNews The homepage of the servicing industry

JPMorgan Chase's recent $1.9 billion residential mortgage-backed security (RMBS) transaction may not spur demand for similar transactions from other banks in the next few years for several reasons, according to a report from Moody’s Investors Service.

JPMorgan Chase's recent $1.9 billion residential mortgage-backed security (RMBS) transaction may not spur demand for similar transactions from other banks in the next few years for several reasons, according to a report from Moody’s Investors Service.

According to the report, which was released this Thursday, not all banks will see the benefits or have the same costs as JPMorgan Chase when securitizing loan portfolios. Though deals like Chase’s could offer banks risk-weighted capital relief, the report says that banks will also consider the effect it will have on shareholder equity returns (ROE), as well as other unweighted leverage ratio capital requirements.

In fact, the report says, with many of these deals, shareholder ROE could actually decline significantly. In a market where banks have seen ROE below the cost of capital since 2007, this will likely be a huge deterrent to similar RMBS purchases.

Banks would need to return capital to the shareholders or choose to redeploy proceeds of the transactions into assets for those shareholders if they want to keep ROE steady. But even this, the report says, poses a problem.

“Reinvesting released deal proceeds into assets yielding more than the non-retained securitization bonds could alter banks' investment portfolios and risk profiles, something they might be unwilling, or unable, to do.”

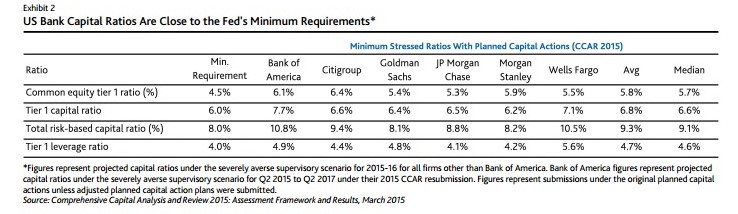

Though under the Basel III regulatory framework, banks may be able to use RMBS purchases to reduce risk weights and the burden of certain regulatory capital requirements, they also need to keep in mind the impact that securitization will have on other capital limitations. The Fed’s supplementary leverage ratio (SLR) constraints will be a big consideration.

“The banks are already in excess of their 5 percent SLR requirement, with their most recently reported, fully phased-in ratios as follows: Bank of America (6.8 percent), JP Morgan (6.6 percent), and Wells Fargo (7.6 percent).”

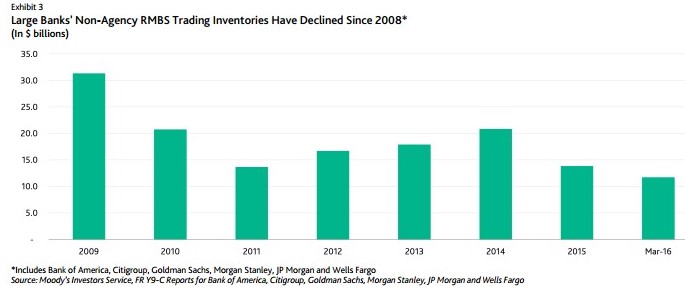

Another big concern for banks will be the weak secondary market, which has seen significant decreases in liquidity as of late, and high RMBS governance, which requires deal agents as well as compensation for those agents. According to the report, both of these issues will likely keep most major banks from following in JP Morgan Chase’s footsteps – at least for the short term.

“Anecdotal evidence from investors indicates that a lack of secondary market liquidity is giving investors pause before they invest in subordinate tranches of RMBS securitizations. Investors have asked for yield premium to account for lower market liquidity, but determining how much that should be is likely to be challenging.”