DSNews The homepage of the servicing industry

DSNews The homepage of the servicing industry

Tuesday’s CoreLogic May 2016 National Foreclosure Report provides further evidence that the housing market may be reaching a “new normal.”

Tuesday’s CoreLogic May 2016 National Foreclosure Report provides further evidence that the housing market may be reaching a “new normal.”

The report showed that foreclosure inventory as well as completed foreclosures continued to declined in May 2016 from where it stood the prior year in May 2015. Despite the decline, the foreclosure rate (1 percent) remains twice that of the national long-term average (0.5 percent). This is due to the individual rates on a state level and is not, in fact, conducive to the progress already made nationally.

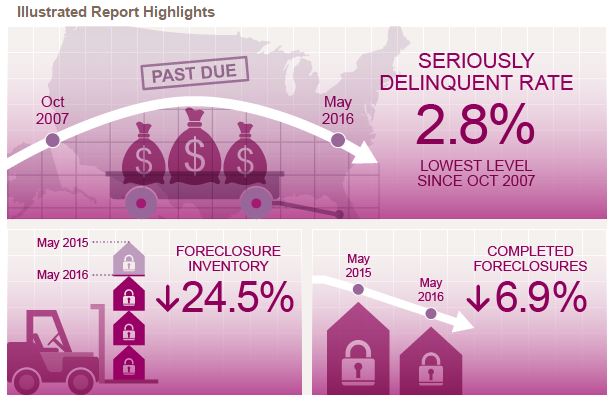

The foreclosure inventory declined by 24.5 percent and completed foreclosures declined by 6.9 percent compared with May 2015. Additionally, the number of completed foreclosures nationwide decreased to 38,000 in May 2016 from 41,000 in May 2015. These results also represent a decrease of 67.9 percent from the peak of 117,813 completed foreclosures in September 2010.

The national foreclosure inventory held approximately 390,000, or 1.0 percent, of all homes with a mortgage in May 2016 compared with the May of 2015 foreclosure inventory of 517,000 homes, or 1.3 percent. It was also determined that the May 2016 foreclosure inventory rate is the lowest it has been for any month since October 2007.

“The foreclosure rate fell to 1 percent in May, which is twice the long-term average of 0.5 percent. However, this masks the underlying progress at the state level,” stated Dr. Frank Nothaft, chief economist for CoreLogic. “Twenty-nine states had foreclosure rates below the national average, and all but North Dakota experienced declines in their foreclosure rate compared to the prior year.”

Because of the progress CoreLogic felt was derived from the state level, the report felt it was important to note that the five states with the highest number of completed foreclosures consisted of Florida with 63,000, Michigan with 45,000, Texas with 27,000, Ohio with 23,000, and California with 23,000. These five states account for almost half of all completed foreclosures nationally. This is compared to the four states and the District of Columbia with the lowest number of completed foreclosures. They are the District of Columbia with 139, North Dakota with 323, West Virginia with 494, Alaska with 648, and Montana with 690.

Because of the progress CoreLogic felt was derived from the state level, the report felt it was important to note that the five states with the highest number of completed foreclosures consisted of Florida with 63,000, Michigan with 45,000, Texas with 27,000, Ohio with 23,000, and California with 23,000. These five states account for almost half of all completed foreclosures nationally. This is compared to the four states and the District of Columbia with the lowest number of completed foreclosures. They are the District of Columbia with 139, North Dakota with 323, West Virginia with 494, Alaska with 648, and Montana with 690.

Additionally, the report also included the four states and the District of Columbia that had the highest foreclosure inventory rate. They were New Jersey holding 3.6 percent, New York holding 3.2 percent, Hawaii holding 2.1 percent, the District of Columbia holding 2.0 percent, and finally Maine holding 1.9 percent. The report compared these results with those for the five states with the lowest foreclosure inventory rate. Alaska held 0.3 percent, Arizona held 0.3 percent, Colorado held 0.3 percent, Minnesota held 0.3 percent, and Utah held 0.3 percent.

CoreLogic found the number of mortgages in serious delinquency decreased by 21.6 percent in May 2016 from the previous year to 1.1 million mortgages, or 2.8 percent of total mortgages. The serious delinquency rate for May 2016 is the lowest it has been in more than eight years, according to the report.

On a month-over-month basis, CoreLogic reported that the foreclosure inventory fell 3.0 percent in comparison to April 2016. It was also reported that completed foreclosures rose 5.5 percent from the 36,000 reported for April 2016 to 38,000 in May 2016. CoreLogic compares these particular results to data in 2007 taken before the decline in the housing market. During that time, completed foreclosures between 2000 and 2006 averaged 21,000 per month nationwide.

“Delinquency and foreclosure rates continue to drop as we experience the benefits of a combination of tight underwriting, job and income growth and a steady rise in home prices. We expect these factors to remain in place for the remainder of this year and for delinquency and foreclosure rates to decline even further,” said Anand Nallathambi, president and CEO of CoreLogic. “As we finally move past the housing crisis, we need to increase our focus on expanding the supply of affordable housing and access to credit for first-time homebuyers in sustainable ways to ensure the long-term health of the U.S. housing market.”

Click here to view the entire report.