According to a new report from CoreLogic’s [1] Property Data Science Team, [2] California is experiencing a serious issue: a number of home insurance carriers are either withdrawing from the state, ceasing to write new policies, or are reducing coverage in wildfire-prone areas.

According to a new report from CoreLogic’s [1] Property Data Science Team, [2] California is experiencing a serious issue: a number of home insurance carriers are either withdrawing from the state, ceasing to write new policies, or are reducing coverage in wildfire-prone areas.

Just as recently as May, State Farm [3] and Allstate [4] announced they will no longer accept new applications for homeowners insurance in California.

This decision followed AIG’s exit from the Golden State market at the beginning of the year. Additionally, several insurance carriers have ceased issuing policies for homes in specific regions of California. As a result, home insurance rates are increasing as options for coverage diminish.

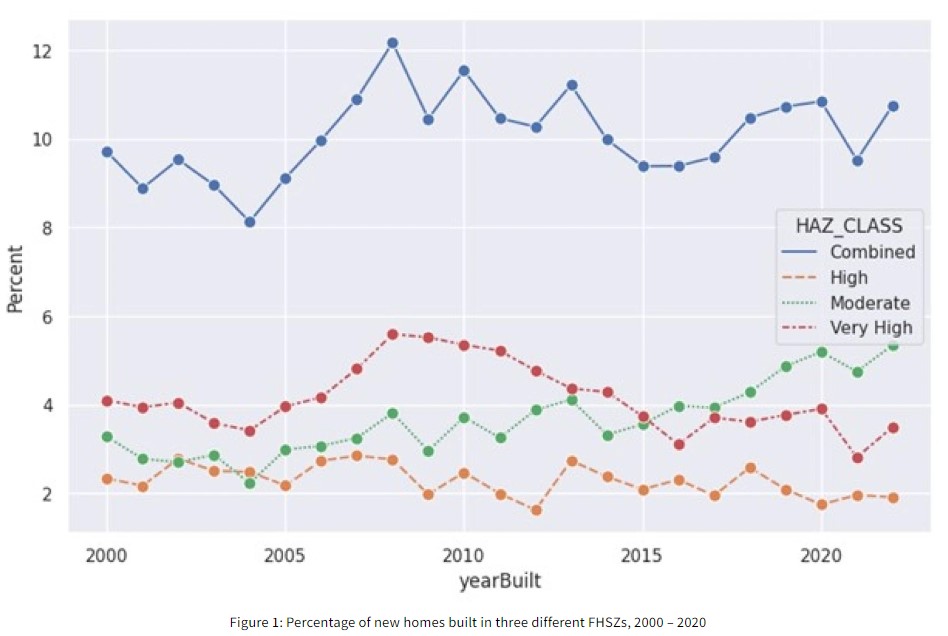

New construction is continuing to happen in California wildfire hazard zones, which the California State Fire Marshall puts Fire Hazard Severity Zones (FHSZ) into three levels of danger: moderate, high, and very high. For this report, CoreLogic combined their data with FHSZ data to provide new insights on the risks of newly built homes in the state.

Notably, the share of homes built in the “very high” FHSZ has declined over the past 15 years, which could be attributed to the implementation of a new building code instituted on Jan. 1, 2008. Building a wildfire-resistant home in California can cost an additional $2,800 to $27,100, as reported by Wildfire Today [5]. These costs, coupled with elevated homeowner insurance premiums, adds to the financial burden of buying a home in California.

On the other hand, the share of new homes constructed in the “moderate” FHSZ has nearly doubled since 2008. However, it is important to note that building homes in Moderate FHSZs does not entirely eliminate wildfire risks.

Following the Great Recession of the 2000s, home prices in California have steadily rose with an average annual appreciation of rate of 9.4%. During the pandemic, however, several factors led to price spikes including social distancing measures, remote work options and an outbound migration away from large metropolitan areas.

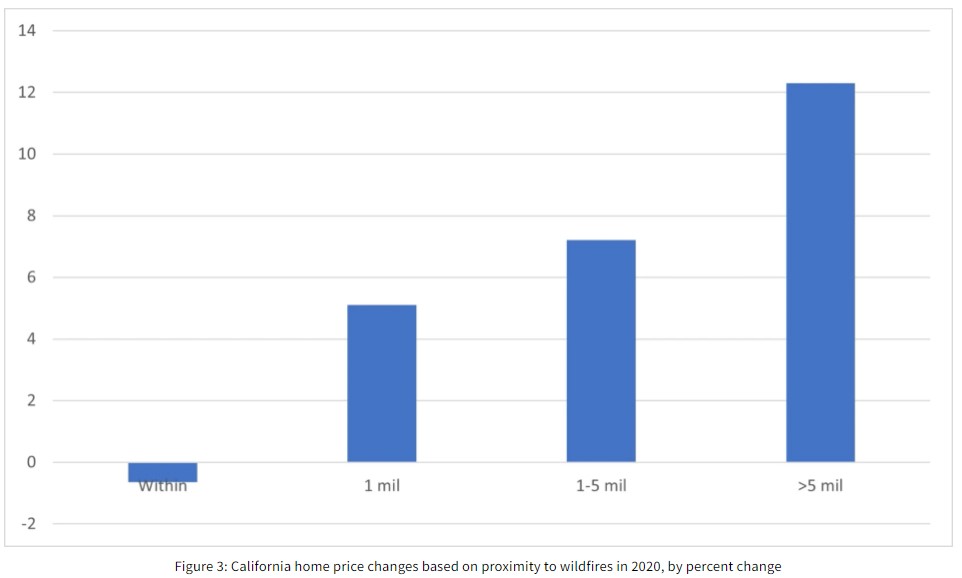

So how have California’s largest wildfires affected home price changes? To find out this figure, CoreLogic examined the five largest fires recorded in state history (all of which occurred in 2020, impacting 19 counties) and assessed the change in value one year from the date of the disaster.

The Property Data Science Team’s initial theory was that all damage would be repaired one year after the wildfires, so the fair value of the property, measured by CoreLogic’s Total Home Value AVM, would not be negatively impacted by property damage. Then they compared the price change between June 2021 and May 2023 for properties located within the fire perimeters, as well as those outside the fire perimeters in all 19 affected counties.

The chart below shows that the price of properties located within a fire perimeter actually declined by 0.64%. In contrast, properties located within one mile from the fire experienced price appreciation of 5.1%, while those situated one to five miles away saw a 7.21% gain.

It is important to note that the average price appreciation for California during the same two-year period was 12.3%. These findings clearly indicate that buyers took past wildfires into careful consideration, which is reflected in housing price movements.

As California’s population continues to grow and residential development expands into higher wildfire hazard areas, an increasing number of properties are more exposed to these catastrophes. Taking a proactive approach to this challenge and addressing its effects on the housing market is essential to promote a healthy and resilient housing ecosystem for homeowners, lenders, insurers and policymakers.