DSNews The homepage of the servicing industry

DSNews The homepage of the servicing industry

Credit bureau TransUnion has released its second quarter Credit Industry Insights Report which highlighted how the number of consumers with credit cards and personal loans has reached record highs, driven by an increase in loans to non-prime consumers.

“Consumers are facing several challenges that are impacting their finances on a day-to-day basis, namely high inflation and rising interest rates. These challenges, though, are happening against a backdrop where employment opportunities are still plentiful and jobless levels remain low. We see lenders offering more access to credit to non-prime consumers, some of whom are new to credit,” said Michele Raneri, VP of U.S. Research and Consulting at TransUnion. “This is a welcome development as more consumers have gained access to credit during a time when high inflation has placed a greater burden on their wallets. While delinquencies generally rise after a period when more non-prime borrowers secure loans, the rates of delinquency remain mostly at or below pre-pandemic levels, particularly for cards and personal loans.”

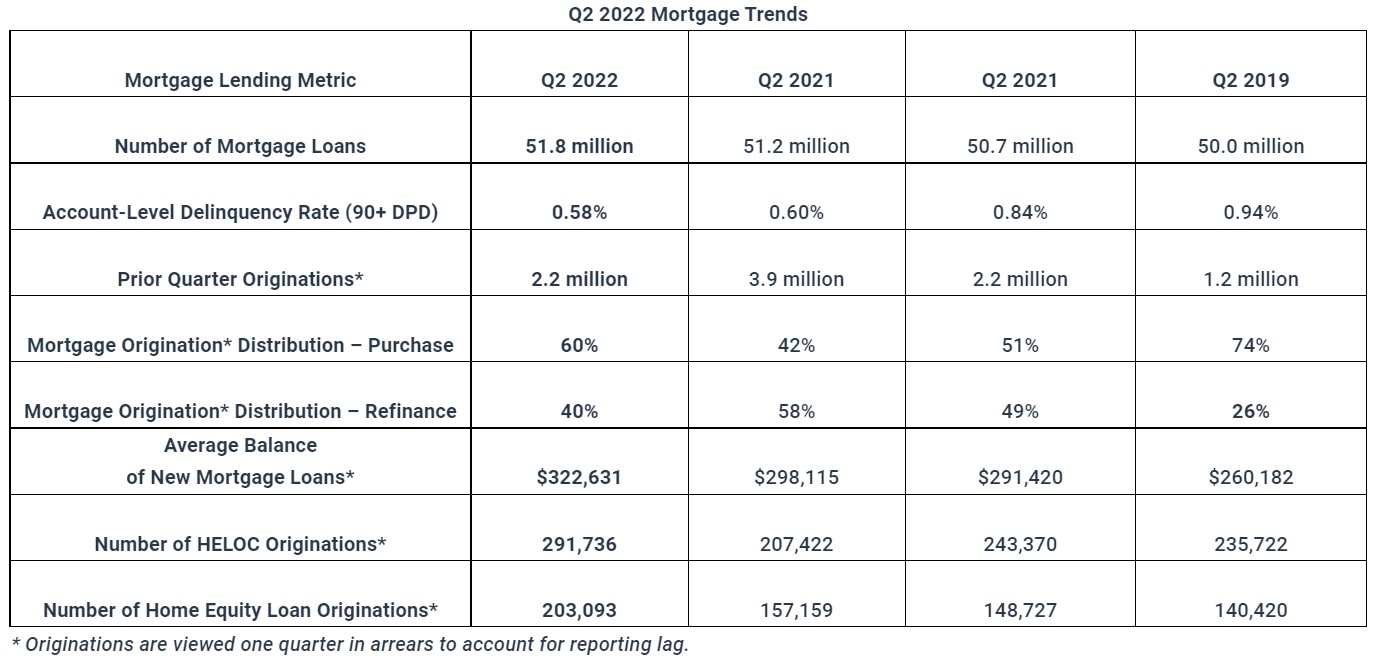

According to TransUnion, available home equity of mortgage holders continued to grow, hitting an aggregate total of $18.4 trillion during the first quarter and is up 22% year-over-year and 52% over the last five years.

Approximately 80 million consumers have available equity in their homes, averaging $223,000. This has caused an increasing number of homeowners to explore HELOC and home equity loan originations resulting in a 41% and 29% year-over-year increase in both of these offerings.

TransUnion went on to say “as home equity grew, the slowdown in mortgage originations accelerated in Q1 2022 with purchases dominating originations for the fourth consecutive quarter. Compared to the previous year, where refinance dominated origination volumes and accounted for 58% of new mortgage loans, in 2022, purchase volumes outpaced refinance volumes, up by 18 percentage points from 42% in Q1 2021 to 60% in Q1 2022. Purchase volumes decreased from 1.6 million in Q1 2021 to 1.3 million in Q1 2022 (down by 20% YoY) while refinance volumes decreased from 2.3 million in Q1 2021 to 870,000 in Q1 2022 (down by 62% YoY).”

There were about 2.2 million originations during the first quarter, a number down 45% year-over-year, while serious mortgage loan delinquencies remain near record lows.

“Mortgage lenders are now considering adding home equity lending to their portfolios as they look for growth in a declining refinance market and seek opportunities to cross-sell to their existing customer base by tapping into historic amounts of home equity,” said Joe Mellman, SVP and Mortgage Business Leader at TransUnion Consumers are increasingly interested in HELOC and home equity loan lending—leveraging rising home values to access affordable capital.”

“Having a comprehensive understanding of industry dynamics in relation to the home equity market can help mortgage lenders identify homeowners in the market for home equity. Utilizing tools that can identify how much equity a homeowner has in their property such as CLTV insights becomes critical in targeted campaigns. This is ever-important as rising interest rates place additional pressure on the housing market and on consumers.”

Click here to view the report in its entirety.