DSNews The homepage of the servicing industry

DSNews The homepage of the servicing industry

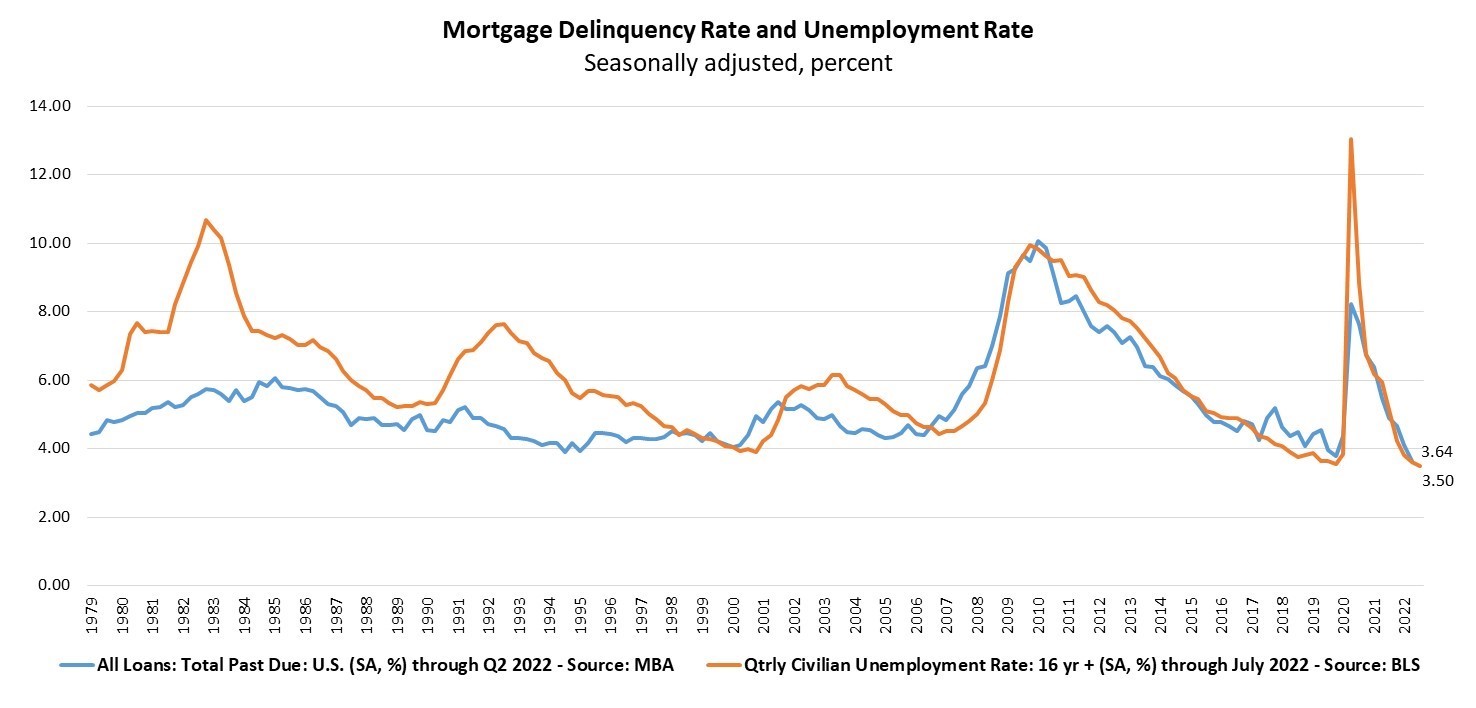

Delinquency rates hit an all-time low during the second quarter of 2022 finally settling at a seasonally adjusted rate of 3.64% of all outstanding residential loans according to the latest iteration of the National Delinquency Survey published by the Mortgage Bankers Association (MBA).

From the first quarter of 2022, the delinquency rate is down 47 basis points and is also down 183 basis points year-over-year.

The survey, which covers mortgages for one-to-four-unit residential properties, also asked servicers to report loans in forbearance as delinquent if payment has not been made based on the original terms of the note.

“At 3.64%, the mortgage delinquency rate in the second quarter fell to its lowest level since MBA’s survey began in 1979—even beating out the previous pre-pandemic, survey low of 3.77% in the fourth quarter of 2019,” said Marina Walsh, MBA’s Vice President of Industry Analysis. “Most of the improvement across all product types—FHA, VA, and conventional loans—resulted from a decline in the loans that were 90 days or more delinquent but not in the foreclosure process.”

According to Walsh, of all the economic indicators that can lead to mortgage delinquencies, the U.S. unemployment rate seems to be the best gauge of loan performance. Despite inflationary pressures, stock market volatility, increases in mortgage rates, and two quarters of economic contraction—often defined as a recession—the job market remains incredibly strong. The unemployment rate was 3.5% in July—a half-century low that tracks closely with the record-low mortgage delinquency rate.

Added Walsh, “Foreclosure inventory levels and foreclosure starts remain well below historical averages for the survey—a strong indication that servicers are able to help delinquent borrowers find alternatives to foreclosure. Such alternatives include curing, loan workouts, home sales—with possible equity to spare, or cash-for-keys and deed-in-lieu options.”

Other key information revealed in the survey include:

- Compared to last quarter, the seasonally adjusted mortgage delinquency rate decreased for all loans outstanding to 3.64%, the lowest level in the history of the survey dating back to 1979. By stage, the 30-day delinquency rate increased 7 basis points to 1.66%, the 60-day delinquency rate decreased 7 basis points to 0.49%, and the 90-day delinquency bucket decreased 47 basis points to 1.49%.

- By loan type, the total delinquency rate for conventional loans decreased 39 basis points to 2.64% over the previous quarter—the lowest level in the history of the survey since 2004. The FHA delinquency rate decreased 73 basis points to 8.85%, and the VA delinquency rate decreased by 64 basis points to 4.22% over the previous quarter.

- On a year-over-year basis, total mortgage delinquencies decreased for all loans outstanding. The delinquency rate decreased by 125 basis points for conventional loans, decreased 392 basis points for FHA loans and decreased 225 basis points for VA loans from the previous year.

- The percentage of loans in the foreclosure process at the end of the second quarter was 0.59%, up 6 basis points from the first quarter of 2022 and 8 basis points higher than one year ago. The foreclosure inventory rate remains below the quarterly average of 1.43% dating back to 1979.

- The percentage of loans on which foreclosure actions were started in the second quarter fell by 1 basis point to 0.18%. The foreclosure starts rate remains below the quarterly average of 0.41% dating back to 1979.

- The non-seasonally adjusted seriously delinquent rate, the percentage of loans that are 90 days or more past due or in the process of foreclosure, was 2.12%. It decreased by 27 basis points from last quarter and decreased by 191 basis points from last year. The seriously delinquent rate decreased 19 basis points for conventional loans, decreased 69 basis points for FHA loans, and decreased 32 basis points for VA loans from the previous quarter. Compared to a year ago, the seriously delinquent rate decreased by 127 basis points for conventional loans, decreased 484 basis points for FHA loans and decreased 219 basis points for VA loans.