DSNews The homepage of the servicing industry

DSNews The homepage of the servicing industry

The analysts at Fitch Ratings credit rating agency report that profitability for America's title insurers should continue to exceed rating expectations over the near term, supported by a robust housing market, continued home price appreciation from elevated market demand, and a constrained housing supply amid persistently low interest rates, according to an H121 Fitch Ratings analysis.

The analysts at Fitch Ratings credit rating agency report that profitability for America's title insurers should continue to exceed rating expectations over the near term, supported by a robust housing market, continued home price appreciation from elevated market demand, and a constrained housing supply amid persistently low interest rates, according to an H121 Fitch Ratings analysis.

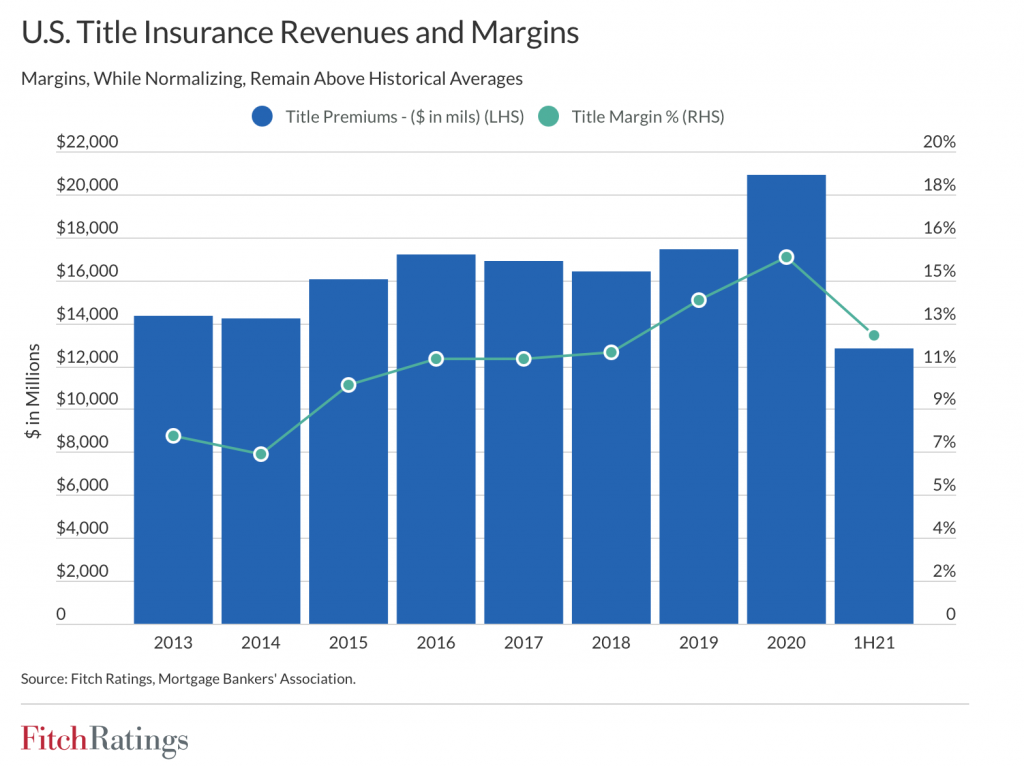

Title operating margins at Fidelity National Financial, First American Financial, Old Republic International, and Stewart Information Services remained above historical averages, according to the release on Fitch Wire, while title-related claims hovered near historical lows.

The analysts say they expect pretax operating margins to remain above long-term industry averages. Aggregate pretax operating margins were 17% for first-half 2021, with aggregate combined ratio of 85% as of June 30, improving from 87% in 2020 and 89% in 2019.

Also at near historical lows are 30-year mortgage rates—that's despite a modest rise in 10-year Treasury yields, supporting robust housing demand and home price appreciation.

"This continues to favorably impact pricing for title underwriters and is expected to limit title-related losses, which will also benefit profitability within the title industry," the analysts report. "However, rising 30-year mortgage rates and normalizing refinance volumes are expected to cut total loan originations by 26% this year and a further 27% in 2022, with revenue declining from 2021 levels but remaining above historical averages. Refis are expected to fall from 65% of originations in 2020 amid the height of the pandemic to 24% by 2023, according to Mortgage Bankers’ Association."

Meanwhile, commercial activity buoyed title insurer revenue, and the analysts concluded that, for title insurers overall, results are expected to be well within ratings expectations.

"However, downside risk to the broader economy remains, especially in light of the most recent surge in pandemic-related disruptions," they concluded. "Title insurers are better capitalized than in 2008 during the Great Financial Crisis, but a prolonged economic downturn leading to falling wages, rising unemployment, rising property foreclosures or lower housing investment would be negative for the industry."