According to the Philadelphia Federal Reserve Bank [1], delinquencies and forbearance markets may have begun to flatten out as forbearances have posted about a half-million in mortgages, delinquencies posted numbers of around 2 million, and foreclosure starts hovering around 30,000 per month.

According to the Philadelphia Federal Reserve Bank [1], delinquencies and forbearance markets may have begun to flatten out as forbearances have posted about a half-million in mortgages, delinquencies posted numbers of around 2 million, and foreclosure starts hovering around 30,000 per month.

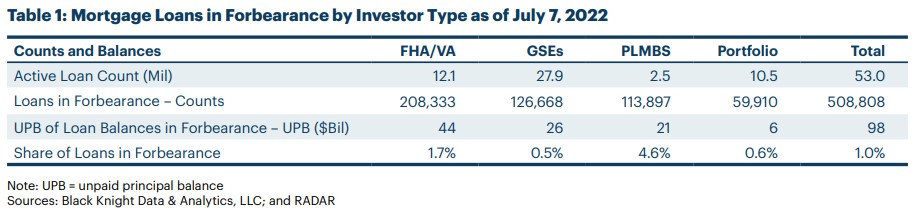

Looking up, most of the 8.9 million borrowers who were in one point in forbearance have now exited. Remaining loans in either forbearance or delinquency will have to deal with the fact that the prospect of much less payment relief going forward. If borrowers cannot find relief, they face the bleak prospect of selling their homes or losing them to foreclosure.

Looking at foreclosures, activity took a near dead-stop in March 2020 as the pandemic began ravaging the country. But these protections expired January 1, 2022 and foreclosure starts rose sharply to 56,000. February, March, April, May, and June recorded 37,000, 36,000, 28,000, 29,000, and 30,000 foreclosure starts, respectively. While these numbers are far higher than those seen during the pandemic, they are now at levels below those observed pre-pandemic. As with other parts of the market, the currently-moderation numbers for foreclosure starts is settling in at around 30,000 per month.

Breaking down past due numbers, 6.8% of all Black homeowners were in some sort of past-due state an of July 7, 2022. This was followed by 4.5% of non-Hispanic homeowners, 4.4% of Hispanic households, 2.8% of white households, and 1.8% of Asian races. “Past due” numbers include all loans in loss mitigation programs, borrowers in forbearance, and borrowers who are delinquent, but an neither in forbearance or loss mitigation.

Click here [2] to view the 9-page report in its entirety.