DSNews The homepage of the servicing industry

DSNews The homepage of the servicing industry

Despite rising prices and Despite rising prices and speculation about looming recession, the Office of the Comptroller of the Currency (OCC) has reported through a new report that the performance of first-lien mortgages held by the federal banking system improved throughout the course of the second quarter of 2022.

Despite rising prices and Despite rising prices and speculation about looming recession, the Office of the Comptroller of the Currency (OCC) has reported through a new report that the performance of first-lien mortgages held by the federal banking system improved throughout the course of the second quarter of 2022.

The quarterly report, entitled OCC Mortgage Metrics Report, showed that 97% of mortgages included in the report were “current and performing” at the end of the quarter, a 3% year-over-year increase.

This report is required by law under the Helping Families Save Their Homes Act of 2009, a provision of the Dodd-Frank Wall Street Reform and Consumer Protection Act.

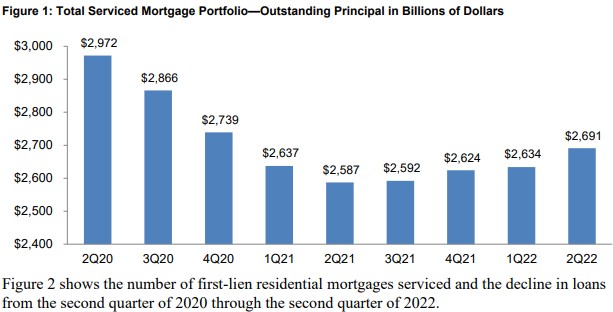

As of the end of the second quarter on June 30, 2022, the reporting banks serviced approximately 12.2 million first-lien residential mortgage loans with $2.7 trillion in unpaid principal balances. This $2.7 trillion was 22% of all residential mortgage debt outstanding in the United States.

Overall, servicers initiated 11,015 new foreclosures during the quarter, a decrease from the prior quarter, but a higher volume than the same period last year. The numbers reveal that new foreclosure volume is now than what was recorded pre-pandemic.

“Home forfeiture actions during the second quarter of 2022—completed foreclosure sales, short sales, and deed-in-lieu-of-foreclosure actions—increased 48.8% from a year earlier to 2,872,” the OCC wrote in its report. “Events associated with the COVID-19 pandemic, including foreclosure moratoriums that began March 18, 2020, and were extended to July 31, 2021, have significantly affected these metrics.”

In terms of modifications, servicers completed 28,109 loan mods, a 33.7% decrease from the previous quarters 42,427, additional performance data is as follows:

- Of these 28,109 modifications, 26,883 or 95.6%, were “combination modifications”—modifications that included multiple actions affecting the affordability and sustainability of the loan, such as an interest rate reduction and a term extension. Of the remaining 1,226 loan modifications, 850 received a single action and 376 were not assigned a modification type.

- Among the 26,883 combination modifications completed during the quarter, 23,492, or 87.4%, included capitalization of delinquent interest and fees; 21,926, or 81.6%, included an interest rate reduction or freeze; 22,499, or 83.7%, included a term extension; 7,144, or 26.6%, included principal deferral; and 39, or 0.1%, included principal reduction.

- Of the 28,109 modifications completed during the quarter, 21,979, or 78.2%, reduced the loan’s pre-modification monthly payment.

- By June 30, 2022, all loans modified during the fourth quarter of 2021 would have aged at least six months. Of the 47,448 modifications completed during the fourth quarter of 2021, servicers reported that 3,731, or 7.9%, were 60 or more days past due or in the process of foreclosure at the end of the month that the modification became six months old (see table 4).

Click here to see the 14-page OCC report in its entirety, including state-level breakdown of data.