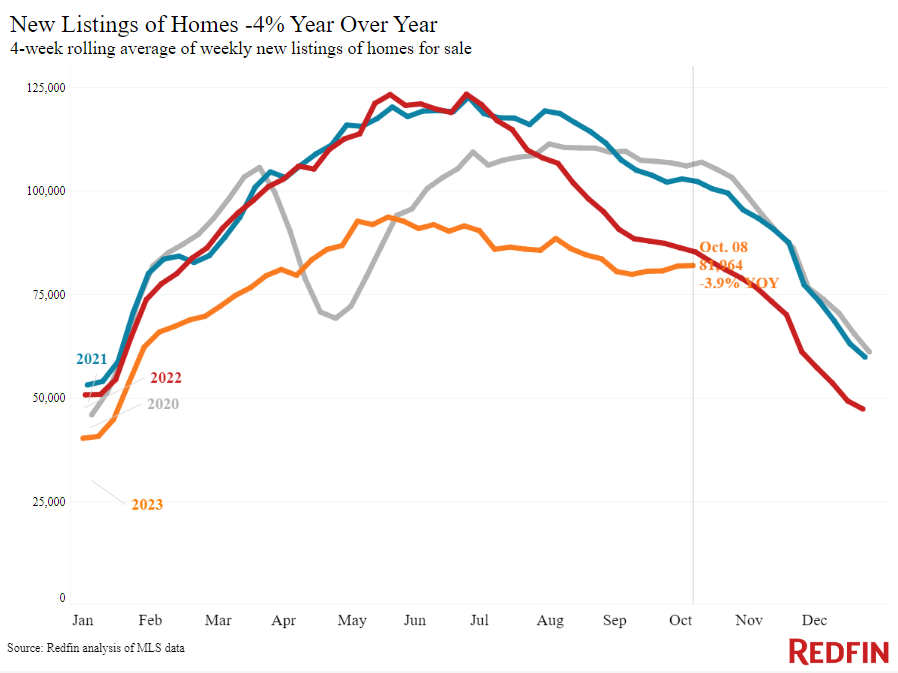

New listings of U.S. homes for sale have ticked up 2% since the start of September, and they haven’t fallen as much from summer to fall as they typically do, according to a new report from Redfin [1].

This is due in part to more homeowners putting their homes on the market, despite being locked into relatively low mortgage rates, as the total number of homes for sale is down 14% from a year earlier during the four weeks ending October 8—the smallest decline since July.

“Despite last week’s hotter-than-expected jobs report, rates have fallen after the Fed signaled this week that it is unlikely to hike interest rates again and war broke out in Israel,” said Redfin Economic Research Lead Chen Zhao. “Buyers should also remember that the average mortgage rate in the news is just that: an average. Many buyers can secure a lower rate by shopping around; the difference between rates among lenders is bigger when rates are higher. Buying down a mortgage rate is always an option, too.”

Leading Indicators of Homebuying Demand and Activity:

- The daily average 30-year fixed mortgage rate was 7.57% as of Oct. 12, down from last week’s two-decade peak of 7.81% and up from 7.1% year-over-year (YoY), according to Freddie Mac data [2].

- The weekly average 30-year fixed mortgage rate was 7.49% as of the week ending Oct. 5, representing the highest level in over two decades, and up from 6.7% YoY, also according to Freddie Mac.

- Mortgage-purchase applications are up 1% from a week earlier as of of week ending Oct. 6, down an estimated 19% YoY, according to the Mortgage Bankers Association [3] (MBA).

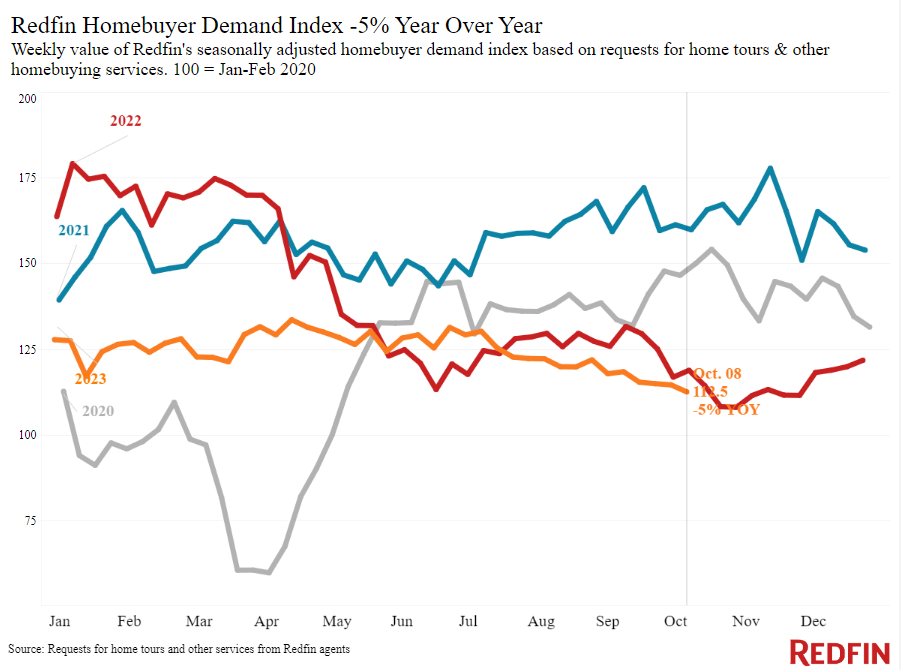

- Redfin Homebuyer Demand Index was down slightly from a month earlier as of the 4 weeks ending Oct. 8, reaching its lowest level in nearly a year, and down an overall 5% YoY, according to Redfin.

- Google searches for “home for sale” are down 12% from a month earlier as of Oct. 7, down approximately 12% YoY, according to Google Trends [4].

Key Housing Market Data (for the four weeks ending October 8):

- The median sale price was $370,000, representing a 2.7% year-over-year (YoY) increase. Prices are up partly because elevated mortgage rates were hampering prices during this time last year.

- The median asking price was $388,223, a 5.2% YoY increase, marking the biggest increase in a year.

- The median monthly mortgage payment was $2,736 at a 7.49% mortgage rate, up 10% YoY, just shy of the all-time high set a week earlier.

- Pending sales totaled 73,943, representing a -11.6% decrease YoY.

- New listings totaled 81,964, representing a -3.9% decrease YoY, marking the smallest decline since July 2022.

- Active listings totaled 827,406, representing a -14% decrease YoY, tied with the previous week for the smallest decline in four months.

- Months of supply remained at 3.2 months, up +0.2 points YoY (4 to 5 months of supply is considered balanced, with a lower number indicating seller’s market conditions).

- The share of homes off the market in two weeks was an estimated 39.5%, up from 36% YoY.

- Median days on market were 32, down an average of -2 days YoY.

- The share of homes sold above list price was 30.7%, up from 30% YoY.

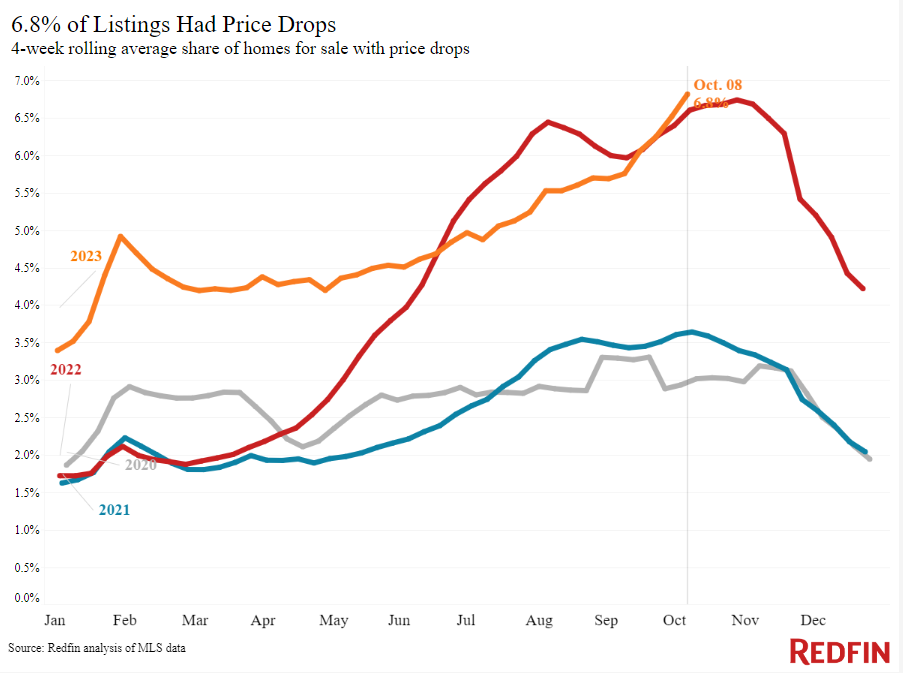

- The share of homes with a price drop was roughly 6.8%, up +0.2 points YoY, representing the highest level in a year.

- The average sale-to-list price ratio was 99.3%, up approximately +0.3 points YoY.

Metros with biggest YoY increases in median sale price:

- Anaheim, CA (13.5%)

- San Jose, CA (11%)

- New Brunswick, NJ (10.5%)

- Providence, RI (10.2%)

- West Palm Beach, FL (9.9%)

Metros with biggest YoY declines in median sale price:

- Austin, TX (-4.1%)

- San Antonio (-2.5%)

- Houston (-2.1%)

- Las Vegas (-0.9%)

- Dallas (-0.6%)

While the average median sale price decreased in nine U.S. metros, in six of those metros, the decline was smaller than 1%.

Metros with biggest YoY increases in new listings:

- West Palm Beach, FL (17%)

- Orlando, FL (16%)

- Miami (14.8%)

- Jacksonville, FL (11.3%)

- Fort Lauderdale, FL (10.2%)

Metros with biggest YoY declines in new listings:

- Atlanta (-26.9%)

- Anaheim, CA (-14.5%)

- Portland, OR (-13.5%)

- Newark, NJ (-13,4%)

- Seattle (-12.8%)

New listings declined in all but 10 metros, with the five biggest increases all in Florida. Overall pending sales declined in all but three metros analyzed: West Palm Beach, FL (7.7%), Orlando, FL (5.5%), and San Jose, CA (4.3%).

Experts are encouraging home sellers to take advantage of still-rising prices, as the median sale price is up 3% YoY despite low housing demand. However, with the share of for-sale homes with a price drop at its highest level in nearly a year and high mortgage rates cutting into homebuyers’ budgets, Redfin agents recommend setting a fair price, as in some parts of the country, many move-in-ready, fairly priced homes are selling quickly.

In comparison, homebuyers are retreating as mortgage rates sit near their highest level in more than two decades and the median U.S. monthly mortgage payment approaches a whopping $3,000. Mortgage-purchase applications inched up slightly this week, but they’re still near their lowest level in nearly 30 years, and Redfin’s Homebuyer Demand Index dropped to its lowest level in nearly a year.

While mortgage rates near their highest level in more than two decades, Redfin experts insist all hope is not lost for homebuyers looking to purchase soon. Although mortgage rates are likely to remain elevated, homebuyers on the fence may consider jumping into the housing market sooner than later. Along with the small uptick in new listings to choose from, daily average rates have come down some from the peak they reached last week.

To read the full report, including more data, charts, and methodology, click here [1].