DSNews The homepage of the servicing industry

DSNews The homepage of the servicing industry

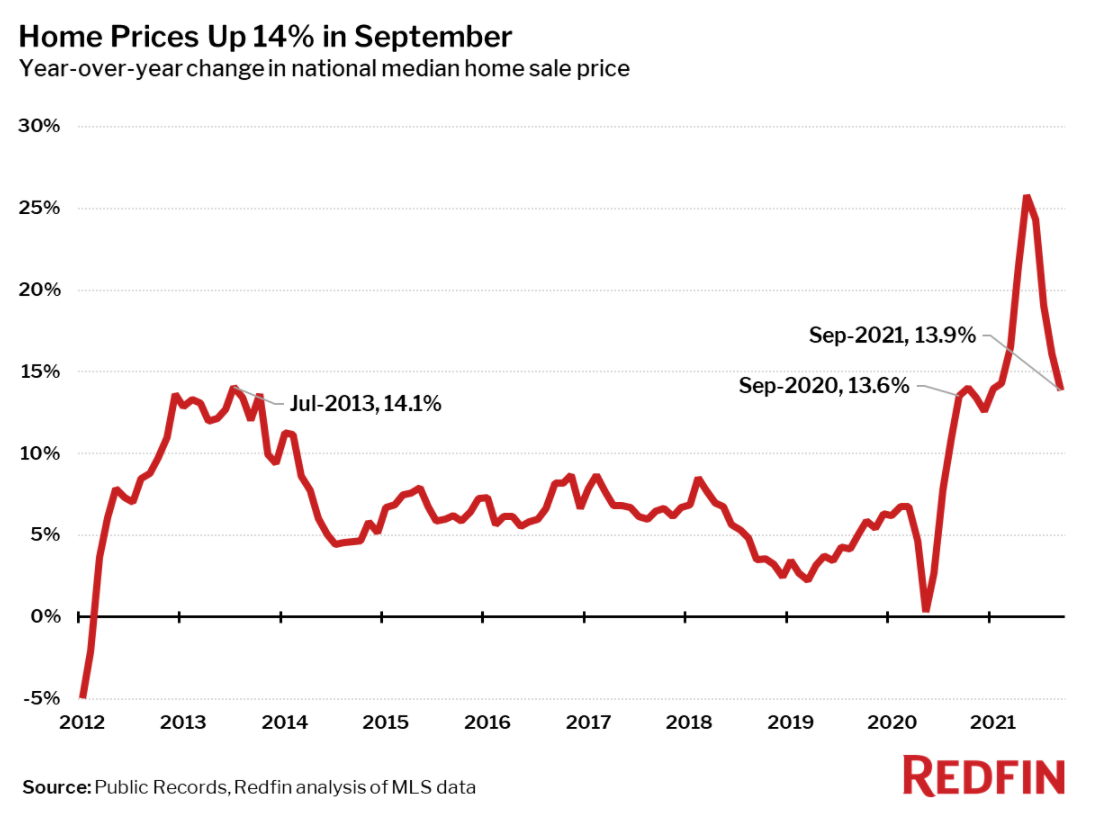

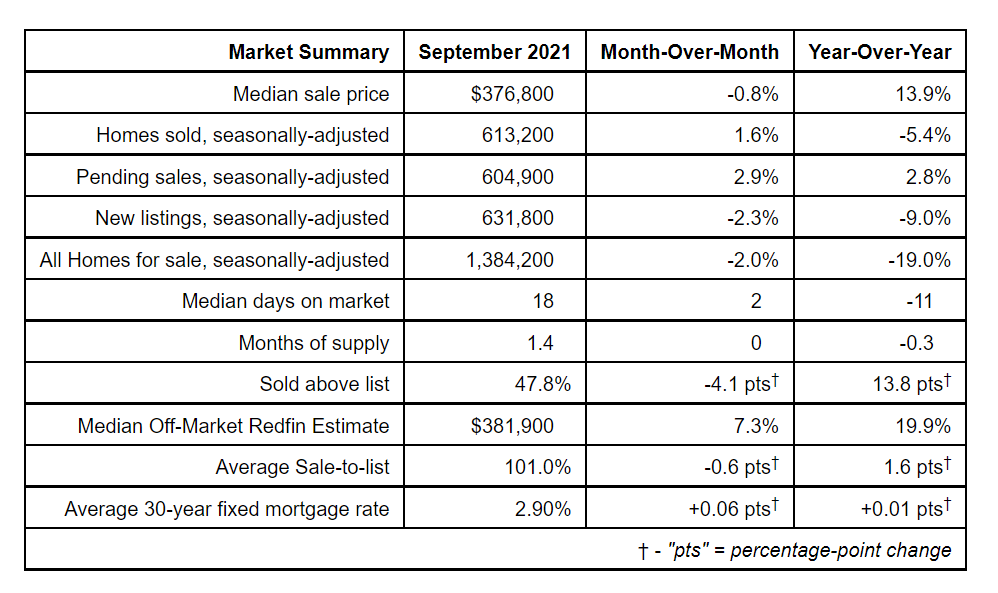

According to a new report from Redfin, the median home sale price rose 14% year-over-year to $376,800 in September 2021, the lowest growth rate since December 2020. The month of September marked the 14th consecutive month of double-digit price gains. Closed home sales and new listings of homes for sale both fell from a year earlier, by 5% and 9%, respectively.

According to a new report from Redfin, the median home sale price rose 14% year-over-year to $376,800 in September 2021, the lowest growth rate since December 2020. The month of September marked the 14th consecutive month of double-digit price gains. Closed home sales and new listings of homes for sale both fell from a year earlier, by 5% and 9%, respectively.

"The severe lack of inventory is restricting home sales," said Redfin Chief Economist Daryl Fairweather. "Even though plenty of people bought homes last year, many homebuyers waited while the pandemic went from bad to worse and remote-work policies were finalized. The homebuyers who are just beginning their search are finding that the well has run dry. But I am hopeful that as it becomes easier to get building materials, we will finally have a strong year for new construction in 2022. That's what the market needs more than anything."

In testimony today before the House Small Business Subcommittee on Oversight, Investigations, and Regulations, National Association of Home Builders (NAHB) Chairman Chuck Fowke detailed the struggle of small home builders face in the wake of the nation’s bottleneck in building materials supply chain.

Contributing to the lack of supply is the scarcity of building supplies, which are being marked up to record highs in some cases. The price of framing lumber a record-high of more than $1,500 per thousand board feet in mid-May, according to Random Lengths. The previous record before prices began their ascent at the outset of the pandemic in April 2020 was just below $600 per thousand board feet.

In terms of the nation’s housing supply, Austin, Texas experienced the highest increase in the number of homes for sale, up 3.3% year-over-year, followed by Tacoma, Washington (2.6%), and Columbus, Ohio (0.3%).

The Baton Rouge, Louisiana region saw the largest drop off in overall active listings, falling 52.6% since last September. Salt Lake City, Utah (-50.3%); Rochester, New York (-46.9%); and North Port, Florida (-42.6%) also saw far fewer homes available on the market than a year ago.

Median sale prices increased in September year-over-year in all but one of the 85 largest metro areas that Redfin tracks: Bridgeport, Connecticut, where prices were down 2.2%. A year ago, prices were up 32% in Bridgeport, as the area experienced a sudden flood of interest from homebuyers looking to leave New York. The current price decline is likely a cooling from an extremely overheated state. The largest price increases in September 2021 were found in North Port, Florida (+30%), Salt Lake City, Utah (+28%), and Austin, Texas (+27%).

The Indianapolis, Indiana market saw homes selling at the quickest pace, with half of all homes pending sale in just five days, down from seven days a year earlier. Denver, Colorado was the next fastest market, with six median days on market, followed by Grand Rapids, Michigan; Seattle, Washington; and Tacoma, Washington all with seven days on market.

The market where the most competition for limited supply in September was found in Oakland, California, where 77.6% of homes sold above list price, followed by 75.5% in San Jose, California; 71.4% in San Francisco, California; 69.5% in Rochester, New York; and 67.3% in Buffalo, New York.

In terms of sales growth, Redfin found that New York led the nation year-over-year, up 25.9%, followed by Honolulu, Hawaii, up 23.6%. San Jose, California rounded out the top three with sales up 14.7% from just one year ago.

On the other end of the spectrum, New Orleans, Louisiana saw the largest decline in sales since last year, falling 41.7%, while sales in Bridgeport, Connecticut and Salt Lake City, Utah declined by 23.5% and 23.3%, respectively.

Click here for more information on Redfin’s latest market analysis.