Utilizing internal data covering the nation’s 50-largest metropolitan statistical areas to determine the average down payment across the country, LendingTree [1] has released a new report that analyzed 580,000 homes that were purchased using a standard 30-year fixed-rate mortgage that included a down payment. The dataset ranges from Jan. 1 to the end of September.

Utilizing internal data covering the nation’s 50-largest metropolitan statistical areas to determine the average down payment across the country, LendingTree [1] has released a new report that analyzed 580,000 homes that were purchased using a standard 30-year fixed-rate mortgage that included a down payment. The dataset ranges from Jan. 1 to the end of September.

High home prices and rates are causing problems across the board including lagging buyer demand and higher down payments. The standard recommended down payment buyers should put up for a home still stands at 20%, which has not changed in recent years, continues to balloon in line with rising home prices.

All-in-all, LendingTree found that average down payments in the nation’s 50 largest metros top at least $47,900 but jump to more than $200,000 in some especially expensive parts of the country.

Key findings as highlighted by the report:

- A down payment on a home across the nation’s 50 largest metros averages $84,499. That’s similar to an average of $84,983 over the same period in 2022. While down payments can vary significantly by location, no metro in this year’s study has an average of less than $47,900.

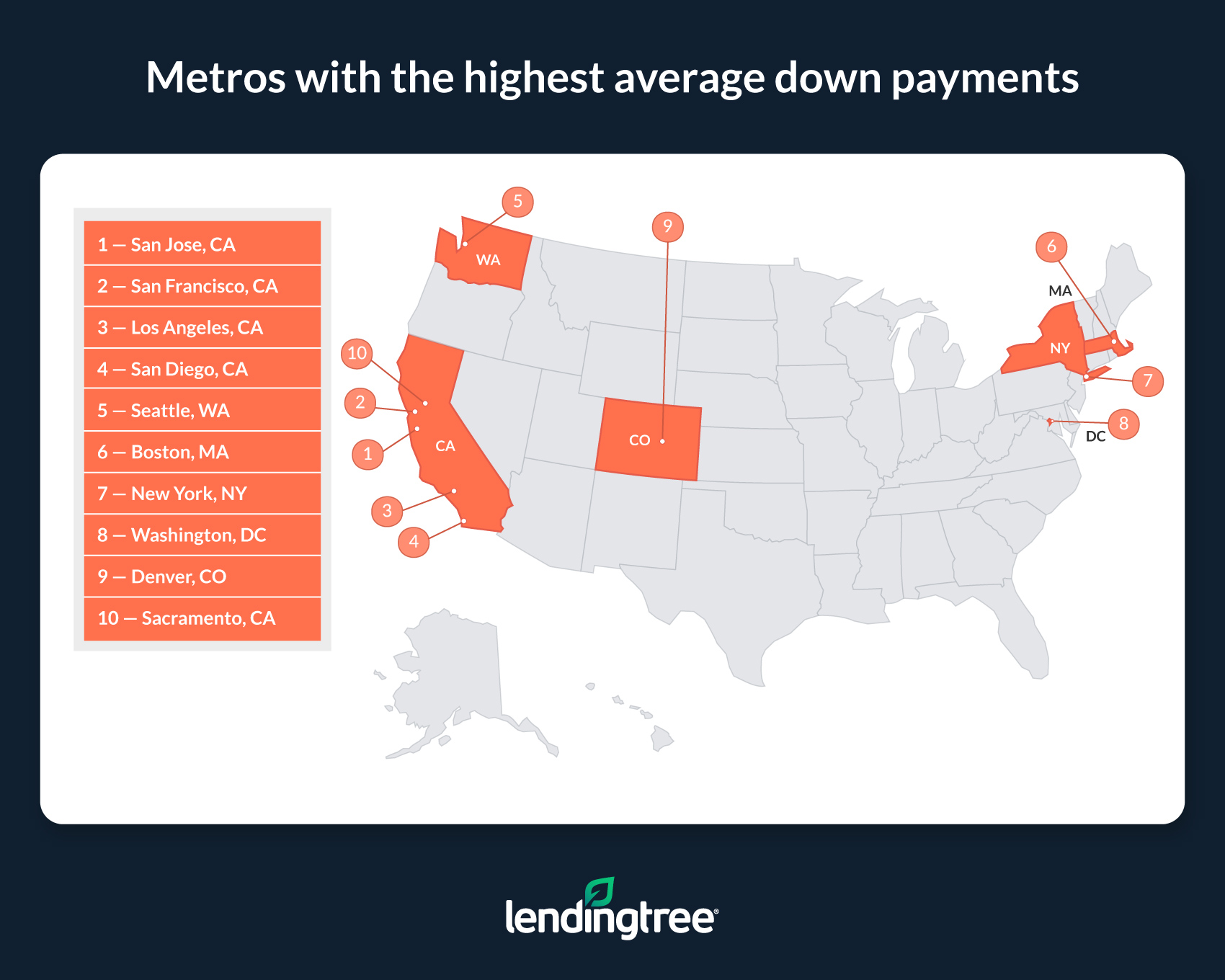

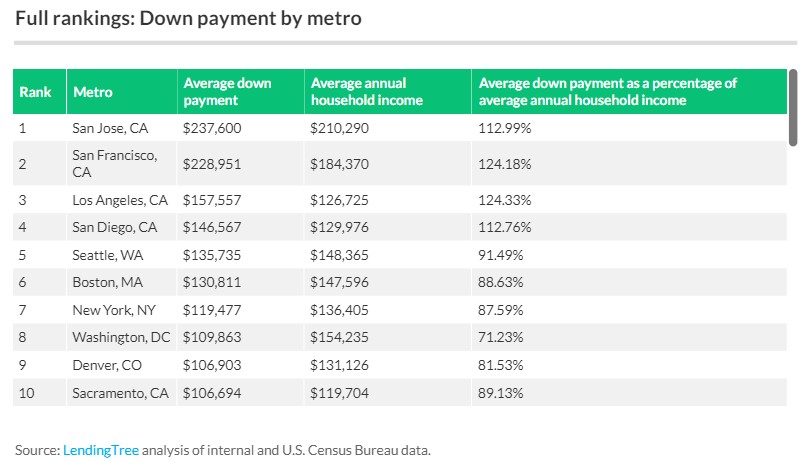

- California is home to the three metros where down payments are highest — San Jose, California, San Francisco and Los Angeles. The average down payments in San Jose and San Francisco are $237,600 and $228,951, respectively—making the two tech hubs the only in our study where down payments top $200,000. While not quite as steep, the average down payment in Los Angeles is still high at $157,557.

- Average down payments are higher than $100,000 in 10 metros. Apart from the previously mentioned California metros, San Diego, Seattle, Boston, New York, Washington, D.C., Denver and Sacramento, California, all have six-figure average down payments.

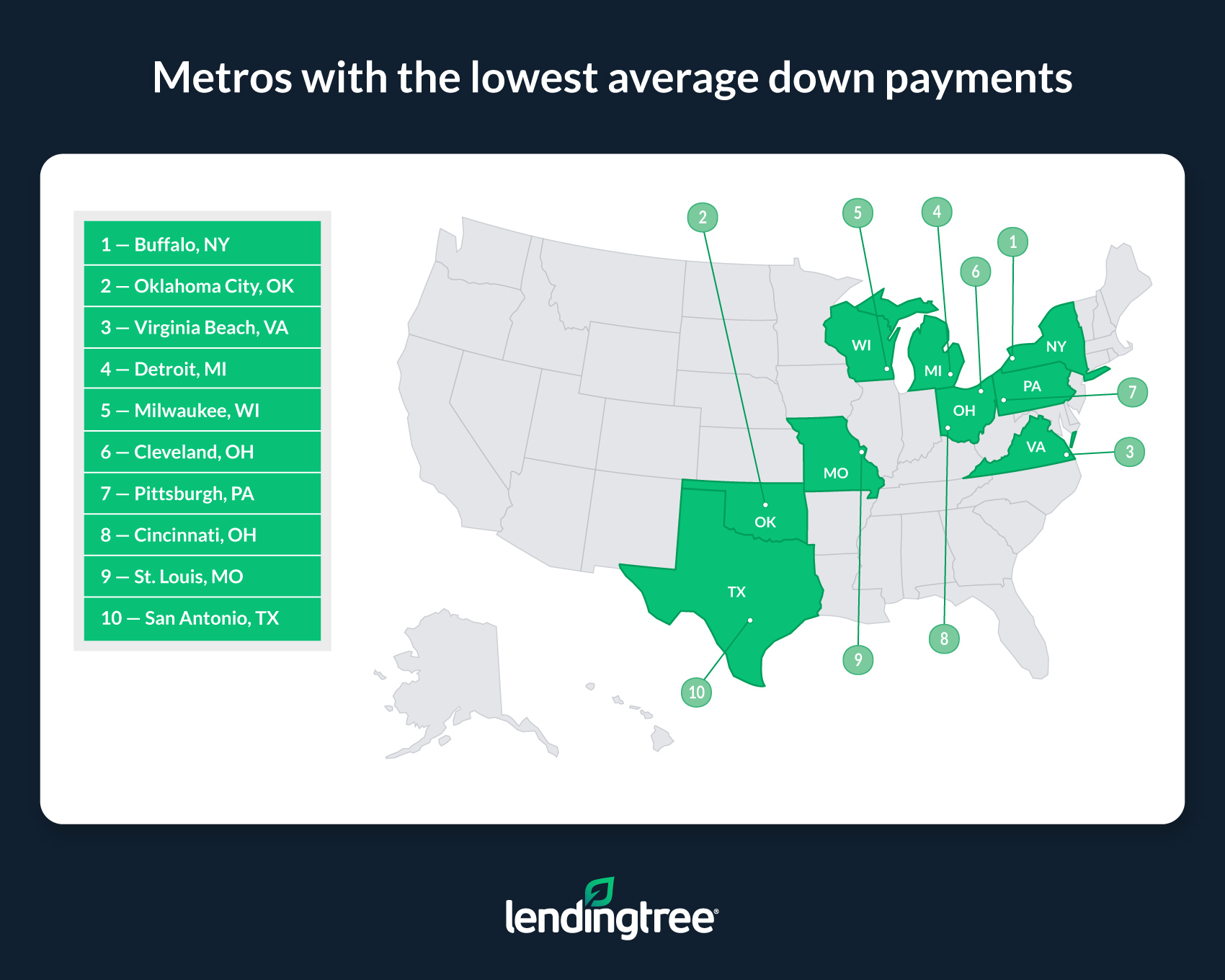

- Buffalo, New York, Oklahoma City and Virginia Beach, Virginia, have the lowest average down payments. Down payments in these metros average $47,976, $49,713 and $52,858, respectively.

- An average down payment on a home across the nation’s 50 largest metros equates to 71.48% of that area’s average annual household income. While there are likely exceptions — like instances where people rely on profits from a past home sale to pay for a down payment on a new place — this figure suggests saving for a down payment is going to be, if nothing else, a time-consuming endeavor in most areas.

- Down payments are the most affordable relative to income in Minneapolis, Buffalo and Virginia Beach. Across these metros, the average down payment is worth 50.96%, 51.97% and 53.40% — respectively — of a given area’s average annual household income.

- Down payments in Los Angeles, San Francisco, San Jose and San Diego are least affordable relative to income. Average down payments in these metros are all higher than their area’s average annual household incomes. An average down payment in these areas is worth 119% of their average annual household income.

Metropolitan areas that necessitate the highest down payments include:

1: San Jose, California

- Average down payment: $237,600

- Average annual household income: $210,290

- Average down payment as a percentage of average household income: 112.99%

2: San Francisco, California

- Average down payment: $228,951

- Average annual household income: $184,370

- Average down payment as a percentage of average household income: 124.18%

3: Los Angeles, California

- Average down payment: $157,557

- Average annual household income: $126,725

- Average down payment as a percentage of average household income: 124.33%

Metros with the lowest average down payments include:

1: Buffalo, New York

- Average down payment: $47,976

- Average annual household income: $92,319

- Average down payment as a percentage of average household income: 51.97%

No. 2: Oklahoma City, Oklahoma

- Average down payment: $49,713

- Average annual household income: $91,696

- Average down payment as a percentage of average household income: 54.22%

No. 3: Virginia Beach, Virginia

- Average down payment: $52,858

- Average annual household income: $98,994

- Average down payment as a percentage of average household income: 53.40%

So what does this mean for buyers? Basically, buyers are having to cough-up more money up front to secure a home—in most cases that means sourcing money from family, or simply saving more by cutting back or taking on a second job.

However, not all homebuyers have to save up for a full 20% down payment. There are a multitude of programs through government and private programs that can reduce necessary down payments to under 5% even though putting down less money means a higher mortgage payment. For instance, the more a person can put down on a home, the more likely they are to get approved for a mortgage and/or be offered a lower interest rate. Higher down payments can also be more attractive to sellers, especially in competitive real estate markets.

Coming up with a down payment isn’t always going to be a walk in the park, and doing so could be challenging and involve jumping through more hoops than buyers might realize. Nonetheless, down payments are important. Even if a large one isn’t always necessary or possible, the more you can put down on a house, the more benefits you’ll likely see.

Click here [2] to see the report, including the list of the top-50 cities, here.