DSNews The homepage of the servicing industry

DSNews The homepage of the servicing industry

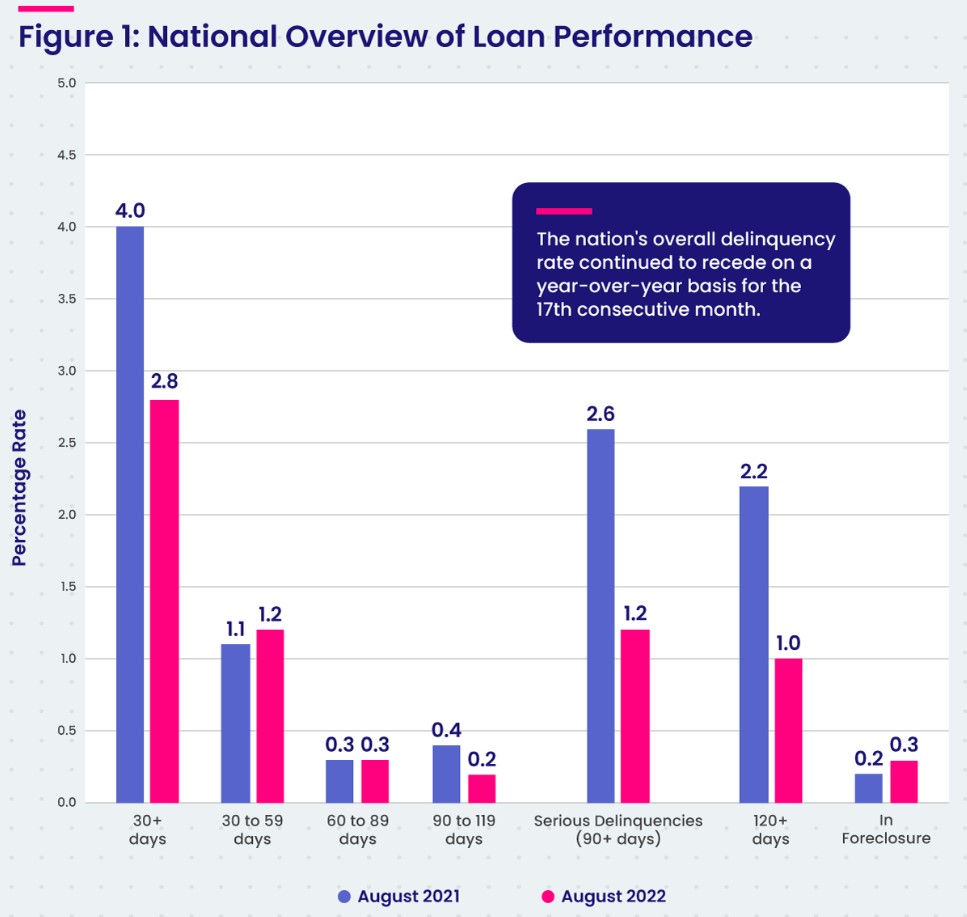

CoreLogic’s Loan Performance Insights Report for August 2022 has found that for the month of August 2022, 2.8% of all mortgages in the U.S. were in some stage of delinquency (30 days or more past due, including those in foreclosure), representing a 0.2%-percentage point decrease month-over-month and a decrease of 1.2 percentage points compared to August 2021 when the rate was 4%.

CoreLogic’s Loan Performance Insights Report for August 2022 has found that for the month of August 2022, 2.8% of all mortgages in the U.S. were in some stage of delinquency (30 days or more past due, including those in foreclosure), representing a 0.2%-percentage point decrease month-over-month and a decrease of 1.2 percentage points compared to August 2021 when the rate was 4%.

This information comes by way of the CoreLogic August 2022 Loan Performance Insights Report, which reports on first-lien mortgages, covering delinquency, transition, and foreclosure rates. CoreLogic estimates that this report covers 75% of available foreclosure data.

In August 2022, the U.S. delinquency and transition rates, and their year-over-year changes, were as follows:

- Early-Stage Delinquencies (30 to 59 days past due): 1.2%, up from 1.1% in August 2021.

- Adverse Delinquency (60 to 89 days past due): 0.3%, unchanged from August 2021.

- Serious Delinquency (90 days or more past due, including loans in foreclosure): 1.2%, down from 2.6% in August 2021 and a high of 4.3% in August 2020.

- Foreclosure Inventory Rate (the share of mortgages in some stage of the foreclosure process): 0.3%, up from 0.2% in August 2021.

- Transition Rate (the share of mortgages that transitioned from current to 30 days past due): 0.6%, unchanged from August 2021.

This data revealed that the number of borrowers classified as seriously delinquent on their mortgage payments in August, the lowest level since April 2020, as the overall delinquency rate remained near a record low.

These numbers have been helped by a low 4% unemployment rate, which helps homeowners continue to make timely payments.

“The share of U.S. borrowers who are six months or more late on their mortgage payments fell to a two-year low in August and was less than one-third of the pandemic high recorded in February 2021,” said Molly Boesel, Principal Economist at CoreLogic. “Furthermore, the foreclosure rate remained near an all-time low, which indicates that borrowers who were moving out of late-stage delinquencies found alternatives to defaulting on their mortgages.”

On a state and local level, the report also found:

- In August, all states posted annual declines in their overall delinquency rates. The states with the largest declines were Hawaii, Nevada and New York (all down 2.1 percentage points). The remaining states, including the District of Columbia, registered annual delinquency rate drops between 2 percentage points and 0.3 percentage points.

- All but five U.S. metro areas posted at least a small annual decrease in overall delinquency rates, with increases in those metros ranging from 0.1 to 0.4 percentage points.

- All U.S. metro areas posted at least a small annual decrease in serious delinquency rates, with Odessa, Texas (down 4.4 percentage points), Laredo, Texas (down 3.3 percentage points) and Midland, Texas and Kahului-Wailuku-Lahaina, Hawaii (both down 3.2 percentage points) posting the largest decreases.

Click here to view the report, including breakdowns for the top-performing metropolitan areas.