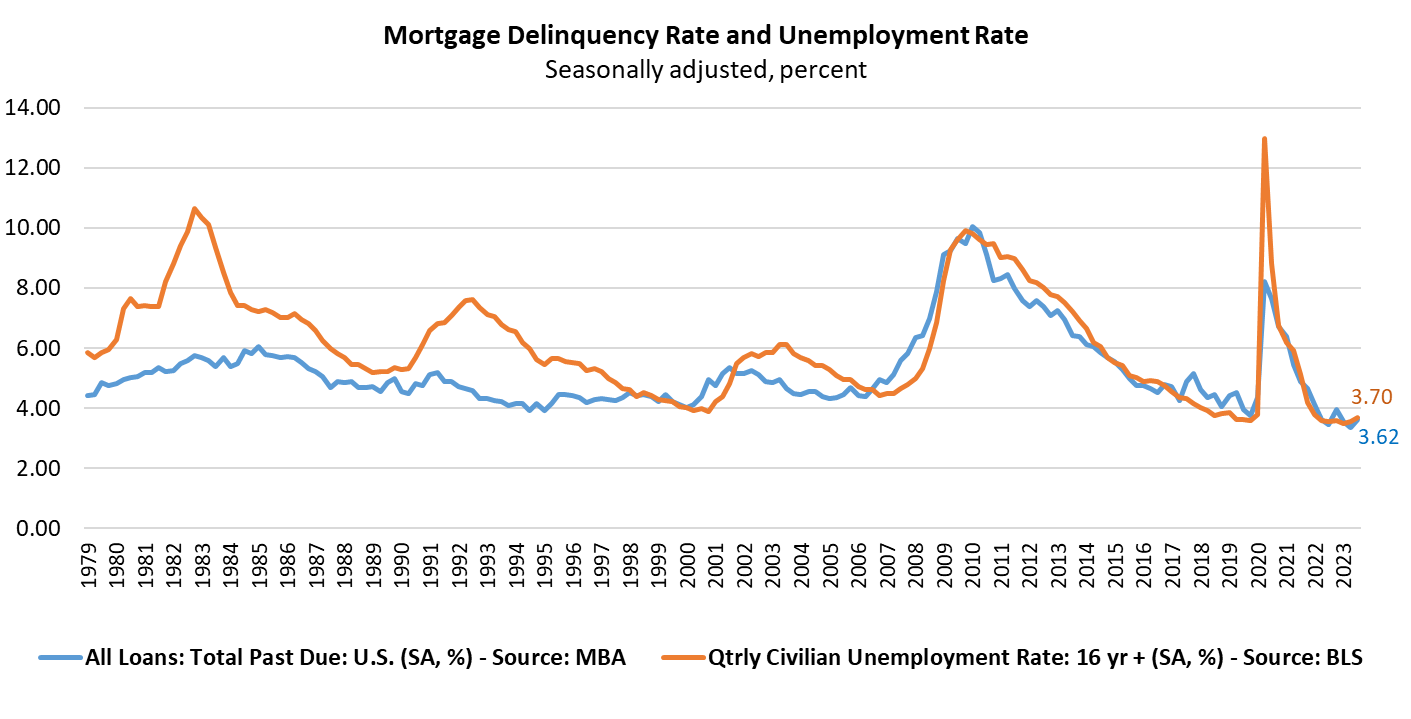

With the labor market having shown recent signs of weakening, and the unemployment rate rising to 3.9% in October, the Mortgage Bankers Association’s (MBA) latest National Delinquency Survey [1] has found that the delinquency rate for mortgage loans on one-to-four-unit residential properties increased to a seasonally adjusted rate of 3.62% of all loans outstanding at the end of the third quarter of 2023.

With the labor market having shown recent signs of weakening, and the unemployment rate rising to 3.9% in October, the Mortgage Bankers Association’s (MBA) latest National Delinquency Survey [1] has found that the delinquency rate for mortgage loans on one-to-four-unit residential properties increased to a seasonally adjusted rate of 3.62% of all loans outstanding at the end of the third quarter of 2023.

The delinquency rate was up 25 basis points from Q2 of 2023, and up 17 basis points year-over-year in Q3. The percentage of loans on which foreclosure actions were started in Q3 rose by just one basis point to 0.14%.

“The national mortgage delinquency rate increased in the third quarter from the record survey low reached in the second quarter of this year, with an uptick in delinquencies across all loan types–conventional, FHA, and VA,” said Marina B. Walsh, CMB, MBA’s VP of Industry Analysis [2]. “The increase was driven entirely by a rise in earliest-stage delinquencies–those 30-days and 60-days past due. Later-stage delinquencies–those 90 days or more past due–declined to the lowest level since the first quarter of 2020.”

Mortgage delinquencies and employment conditions continue to track very closely, according to Walsh, as the Bureau of Labor Statistics (BLS) reported [3] that unemployment rates were higher in September than a year earlier in 231 of the 389 metropolitan areas polled, lower in 131 areas, and unchanged in 27 areas. The BLS also reported [3] that a total of 10 areas had jobless rates of less than 2% and four areas had rates of at least 8%. Nonfarm payroll employment increased over the year in 64 metropolitan areas, decreased in just one area, and was essentially unchanged in 324 areas. The national unemployment rate in September was 3.6%, not seasonally adjusted, up from 3.3% a year earlier.

MBA forecasts slower hiring and rising unemployment, with the unemployment rate rising to 5% by the end of 2024.

“The increase in unemployment will likely mean further increases in mortgage delinquencies, particularly for FHA borrowers,” said Walsh.

Key findings of MBA's Q3 National Delinquency Survey:

- Compared to last quarter, the seasonally adjusted mortgage delinquency rate increased for all loans outstanding. By stage, the 30-day delinquency rate increased 28 basis points to 2.03%, the 60-day delinquency rate increased seven basis points to 0.62%, and the 90-day delinquency bucket decreased nine basis points to 0.98%.

- By loan type, the total delinquency rate for conventional loans increased 21 basis points to 2.50% over the previous quarter. The FHA delinquency rate increased 55 basis points to 9.50%, and the VA delinquency rate increased by six basis points to 3.76%.

- On a year-over-year basis, total mortgage delinquencies increased for all loans outstanding. The delinquency rate decreased by two basis points for conventional loans, increased 98 basis points for FHA loans, and increased five basis points for VA loans from the previous year.

- The delinquency rate includes loans that are at least one payment past due, but does not include loans in the process of foreclosure. The percentage of loans in the foreclosure process at the end of Q3 was 0.49%, down four basis points from Q2 of 2023, and down seven basis points lower than one year ago, marking the lowest foreclosure inventory rate since Q4 of 2021.

- The non-seasonally adjusted seriously delinquent rate, the percentage of loans that are 90 days or more past due or in the process of foreclosure, was 1.52%, the lowest level since 1984. It decreased by nine basis points from last quarter and decreased by 38 basis points from last year. The seriously delinquent rate decreased five basis points for conventional loans, decreased 37 basis points for FHA loans, and decreased 16 basis points for VA loans from the previous quarter. Compared to a year ago, the seriously delinquent rate decreased by 31 basis points for conventional loans, decreased 92 basis points for FHA loans, and decreased 52 basis points for VA loans.

- The five states reporting the largest quarterly increases in their overall delinquency rate were: South Dakota (124 basis points), New Mexico (61 basis points), Hawaii (54 basis points), Mississippi (49 basis points), and Louisiana (49 basis points).

“The decline in later-stage delinquencies, along with a foreclosure starts rate of 0.14%–which is well below the historical quarterly average of 0.40%–suggest that distressed homeowners may be utilizing available loss mitigation options that prevent a foreclosure start,” said Walsh. “Additionally, accumulated home equity may also be enabling some homeowners to sell their homes well before foreclosure becomes a possibility.”