DSNews The homepage of the servicing industry

DSNews The homepage of the servicing industry

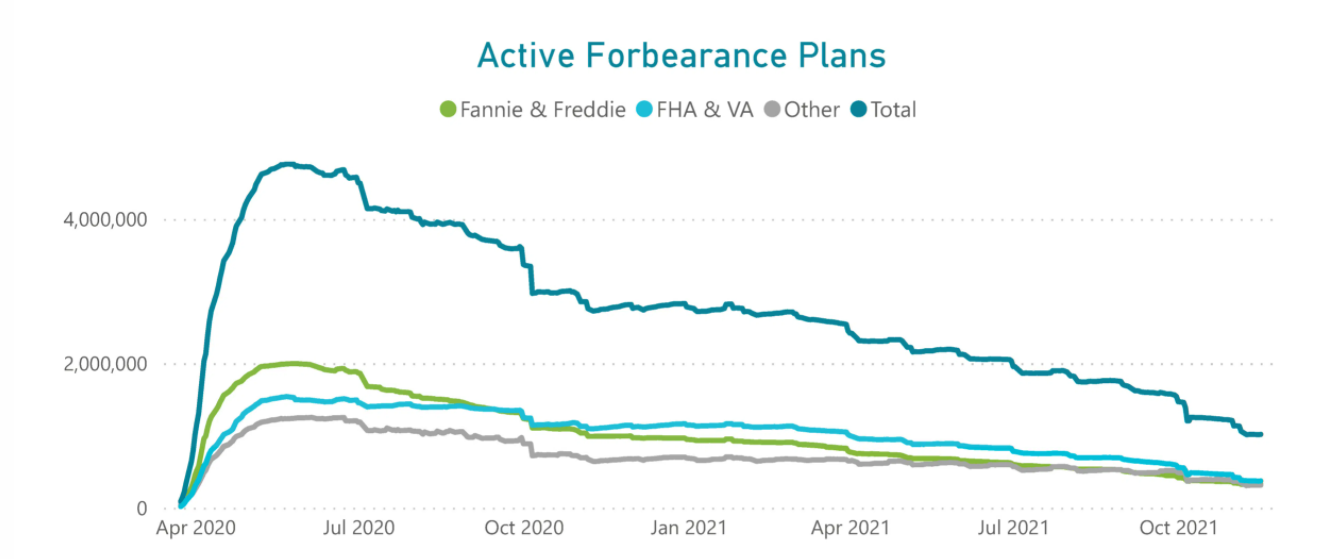

An examination of the latest forbearance data from Black Knight Inc. has found the number of active U.S. forbearances remained on a relatively steady and predictable pattern entering the final month of 2021.

An examination of the latest forbearance data from Black Knight Inc. has found the number of active U.S. forbearances remained on a relatively steady and predictable pattern entering the final month of 2021.

Andy Walden, Economist and Director of Market Research at Black Knight, examined the company’s McDash Flash daily forbearance data, and found that the number of active forbearance plans increased by 2,000 (0.2%) this week.

“As of November 16, 1.01 million mortgage holders remain in COVID-19 related forbearance plans, representing 1.9% of all active mortgages, including 1.2% of GSE, 3.1% of FHA/VA, and 2.4% of portfolio held, and privately securitized loans,” said Walden in the report.

Black Knight reported that of the 1,015,000 total loans in forbearance, 326,000 represented Fannie Mae and Freddie Mac (GSE) loans; 373,000 represented FHA and VA loans; while 316,000 loans were held by portfolios, private labeled securities, or other entities.

The total loans in forbearance accounts for approximately $188 billion in unpaid principal balance (UPB). Of that total, $67 billion was comprised of GSE loans, $64 billion in FHA and VA loans, and $57 billion from portfolios, private labeled securities or other entities.

“Modest declines among FHA/VA loans (-2,000) and GSE (-1,000) were offset by a 5,000 rise in plan volumes among portfolio and PLS mortgages as plan activity hit its lowest level since mid-August,” noted Walden in the report. “Start volumes edged higher, driven by an increase in new plans among FHA/VA loans, which hit their highest level since early October.”

Overall forbearance plans were down 18% month-over-month.

“More than 200,000 plans remain with October/November reviews for extension/removal, and nearly 300,000 more are slated for review in December–half of which are expected to be reaching their final expirations,” said Walden.

Continued improvements in unemployment claims could support a further rise in forbearance exits, as this week, the U.S. Department of Labor reported the advance figure for seasonally-adjusted initial claims was 268,000, a decrease of 1,000 from the previous week's revised level, marking the lowest level for initial claims since March 14, 2020, when it was 256,000.

One byproduct of the ending of forbearances is a rise in the nation’s housing supply, an inventory which currently sits at all-time lows, according to RE/MAX. The company’s latest National Housing Report found that the number of homes for sale in October 2021 was down 12.7% from September, and down 28% year-over-year. Factoring into the increase in inventory is the expiration of forbearance plans for many, as some homeowners will be forced to sell their homes at the conclusion of their forbearance plan.

In addition, the end of forbearances for many is pumping life back into the rental market, as those exiting forbearance who choose to sell their homes may opt to rent until a feasible option can be locked down.

“The end of forbearance has forced many lower-income Americans to put their homes up for sale and become renters,” said Redfin Chief Economist Daryl Fairweather.