DSNews The homepage of the servicing industry

DSNews The homepage of the servicing industry

Heightened regulatory and counterparty oversight, the rising cost of holding mortgage servicing rights as an asset, and post-crisis changes to servicing practices that have substantially increased the cost of servicing a loan are three factors driving changes in the mortgage servicing industry since the housing crisis, according to Freddie Mac's November 2015 Insight & Outlook report released on Monday.

Heightened regulatory and counterparty oversight, the rising cost of holding mortgage servicing rights as an asset, and post-crisis changes to servicing practices that have substantially increased the cost of servicing a loan are three factors driving changes in the mortgage servicing industry since the housing crisis, according to Freddie Mac's November 2015 Insight & Outlook report released on Monday.

According to Freddie Mac, in the five year-period between 2008 and 2013, the cost of servicing a performing loan increased 2.6 times (from $59 to $156) while the cost of servicing a non-performing loan spiked by 4.9 times (from $482 to $2,357) during the same period. The cost to service a nonperforming loan exceeds the servicer’s compensation; prior to the crisis, per-loan losses on non-performing loans didn’t threaten the servicing business’s overall profitability because non-performing loans represented a small enough share of the servicer’s portfolio. This changed due to the massive surge in volume of non-performing loans as a result of the crisis, making the share of non-performing loans in servicers’ portfolios significantly higher; the increased cost per year by nearly 5 percent to service non-performing loans; and the increase in regulatory oversight has increased the cost of servicing all loans.

Some servicers are also factoring in a mental “reserve” for regulatory uncertainty due to increased concern on the part of servicers over potential liability for mistakes; these mental reserves are expected to diminish as servicers gain more certainty about the regulatory environment, according to Freddie Mac.

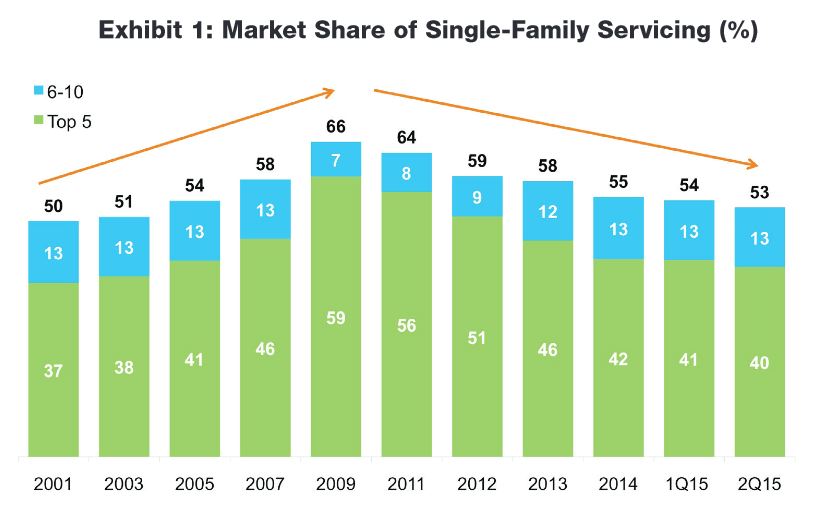

“Prior to the housing crisis and Great Recession, mortgage servicing had followed a decades-long trend of consolidation,” Freddie Mac Chief Economist Sean Becketti said. “In 2001, the top five servicers handled 37 percent of all servicing. By 2009, the market share of the top five had grown to 59 percent. But during the recession, this trend reversed, and by the second quarter of 2015 the share of the top five servicers shrank to 40 percent. In many ways, today's market resembles the 1980s where smaller servicers and nonbank servicers held a higher share before the industry started to consolidate. Housing finance is still evolving, and mortgage servicing is likely to continue to change along with it. It's too soon to say if recent trends will persist or be reversed.”

Increased regulatory oversight since the crisis includes the addition of the Consumer Financial Protection Bureau in July 2011 and the CFPB’s subsequent heightened servicing standards that became effective in January 2014. The GSEs and the FHA have always had scorecards to gauge performances of servicers, but those scorecards have been refined in the last few years due to the experiences of the housing crisis.

Increased regulatory oversight since the crisis includes the addition of the Consumer Financial Protection Bureau in July 2011 and the CFPB’s subsequent heightened servicing standards that became effective in January 2014. The GSEs and the FHA have always had scorecards to gauge performances of servicers, but those scorecards have been refined in the last few years due to the experiences of the housing crisis.

Also in recent years, the capital cost of holding an MSA (mortgage servicing asset) has increased. The estimated value of the MAS has counted toward a bank’s regulatory capital, but revised Basel III capital rules that went into effect this year are limiting the amount of an MSA that can be counted toward a bank’s regulatory capital. Also under the new regulatory environment, the MSA’s risk weight included in the capital will spike by about two and a half times.

“These two changes—limiting an MSA’s use as regulatory capital and increasing the asset’s risk weight—make it more challenging for banks to achieve target capital ratios, especially in the required CCAR and DFAST stress tests. At present, these changes don’t appear to place the largest banks at risk of falling below their target capital levels,” Freddie Mac wrote in the report. “However, some mid-sized banks with large mortgage operations may have to reduce their holding of MSAs, increase their holdings of other types of capital, or reduce their assets to maintain their desired capital ratios.”

Those three factors have resulted in the following changes in the structure of the servicing industry, according to Freddie Mac:

- A reverse in the decades-long trend of consolidation; smaller servicers now handle the majority of mortgage servicing. The top five servicers handled 37 percent of servicing in 2001, seven years before the crisis; at the peak of the crisis in 2009, that share swelled to 59 percent. By 2015, it was back down to 40 percent.

- An increase in the share of mortgage servicing handled by nonbanks. Among the top 20 servicers in 2009, nonbanks accounted for 9 percent of the servicing; that share had more than doubled up to 19 percent five years later in 2014.

- Growth in subservicing, and specialty servicing has become a significant sector in servicing overall. Some of the subareas in which subservicing is becoming increasingly specialized are servicing non-performing loans, servicing loans that are likely to be modified, or focusing on loans that are likely to end in foreclosure, according to Freddie Mac.