DSNews The homepage of the servicing industry

DSNews The homepage of the servicing industry

Balances on home equity lines of credit (HELOCs) continued their trend of declining in Q3, dropping down to an aggregate balance of about $492 billion as of the end of the quarter, according to data recently released by the Federal Reserve Bank of New York.

Balances on home equity lines of credit (HELOCs) continued their trend of declining in Q3, dropping down to an aggregate balance of about $492 billion as of the end of the quarter, according to data recently released by the Federal Reserve Bank of New York.

HELOCs declined by 1.4 percent (about $7 billion) quarter-over-quarter in Q3 and by 3.9 percent (about $20 billion) year-over-year, and they have been on the decline since hitting their peak in 2009. HELOCs were the only debt category out of five that experienced a decline in Q3. The other categories were mortgage debt, student loan debt, auto loan debt, and credit card debt.

The percentage of HELOCs in 90-plus day delinquency also took a tumble from Q2 to Q3, from 3.2 percent down to 2.4 percent, according to the New York Fed. Overall, total household indebtedness increased by $212 billion from Q2 to Q3 and by $355 billion over the year in Q3, up to approximately $12.07 trillion.

The decline in aggregate outstanding balance of HELOCs is a reflection of a decrease at larger banks, according to Michael Neal, Senior Economist with the National Association of Home Builders. Neal cited bank-level analysis of the Consolidated Reports of Condition and Income which are referred to as call reports.

By comparison, the number of HELOCs originated at smaller-sized banks has seen an increase in recent years, Neal pointed out.

By comparison, the number of HELOCs originated at smaller-sized banks has seen an increase in recent years, Neal pointed out.

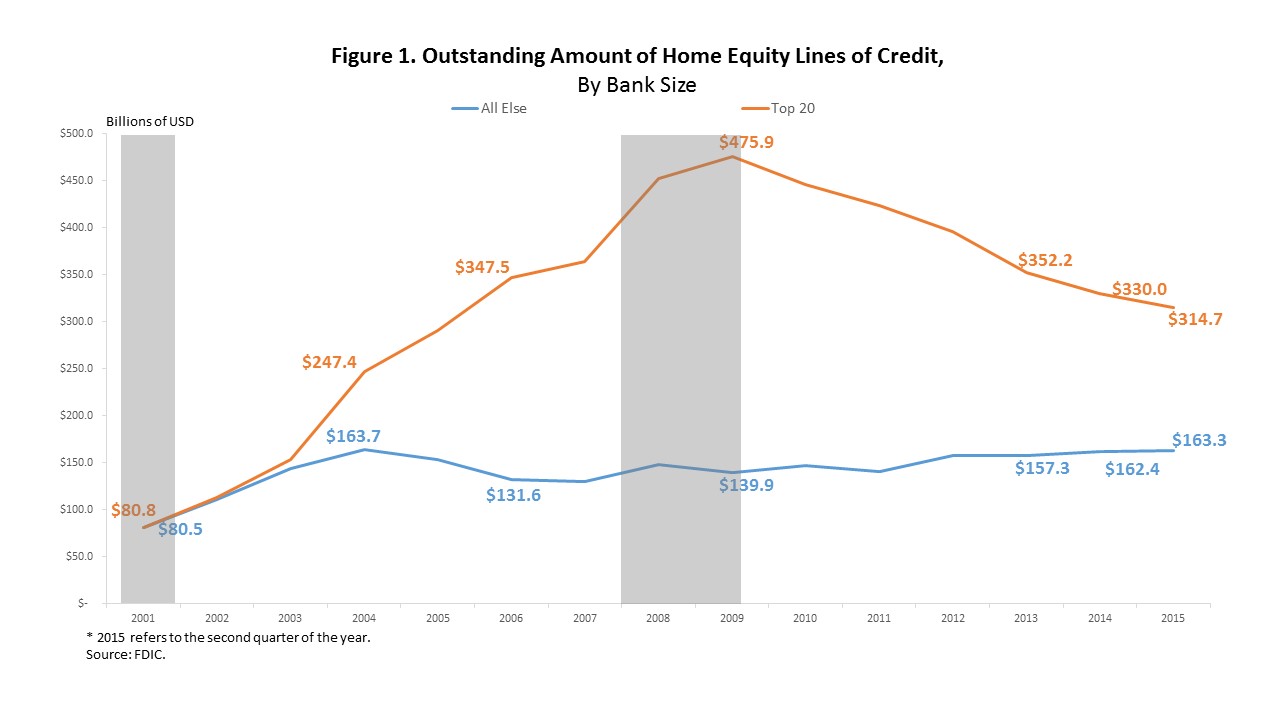

“[I]n 2001 the outstanding amount of HELOCs at the 20 largest banks as measured by total loans and leases, was equal to the combined amount of HELOCs on the balance sheets of all other banks,” Neal said. “The outstanding amount of HELOCs was split nearly evenly until 2003, even as the total amount was rising.”

The outstanding balance of HELOCs at the top 20 banks skyrocketed beginning in 2003, however, and hit a peak of $475.9 billion in 2009. In the six years since, that share has plummeted to $314.7 billion; in the pre-bubble years, the HELOC share at all other banks outside the top 20 doubled in the three-year period between 2001 and 2004. But by 2006, it had fallen to $131.6 billion.

“Instead of an up-and-down cycle, the outstanding amount of HELOCs held at all other banks remained steady through the financial crisis,” Neal said. “In recent years, the outstanding amount of HELOCs held at other banks has risen slightly. Since the outstanding amount of HELOCs on the balance sheets of all other banks is rising while declining at the Top 20 banks, then the gap between the two cohorts is converging.”