DSNews The homepage of the servicing industry

DSNews The homepage of the servicing industry

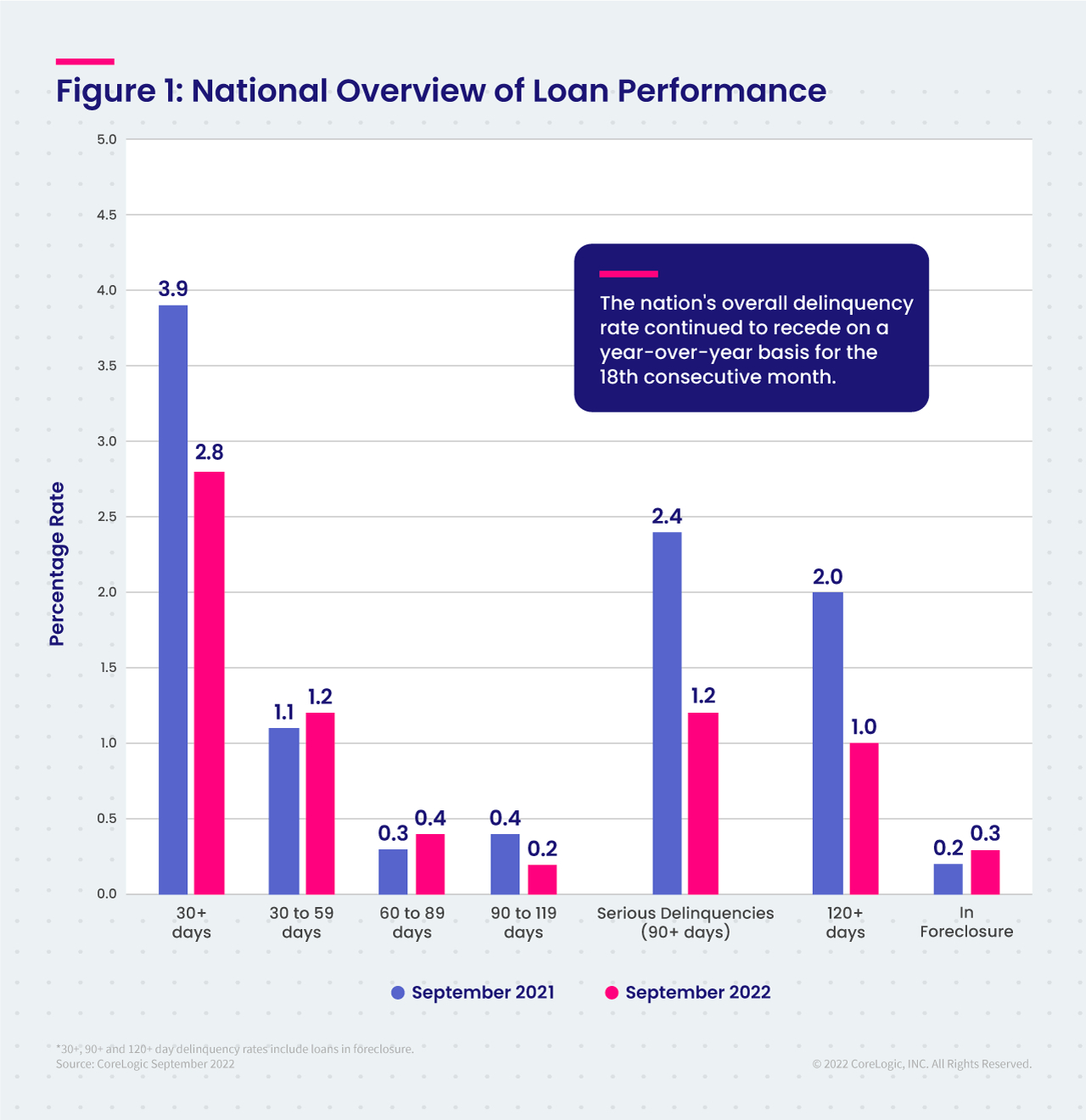

CoreLogic’s Loan Performance Insights Report for September 2022 has found that 2.8% of all mortgages nationwide (approximately 1.4 million loans) were in some stage of delinquency (30 days or more past due, including those in foreclosure), representing a 1.1 percentage point decrease compared to 3.9% in September 2021. The nation’s overall delinquency rate dropped for the 18th straight month on an annual basis.

CoreLogic’s Loan Performance Insights Report for September 2022 has found that 2.8% of all mortgages nationwide (approximately 1.4 million loans) were in some stage of delinquency (30 days or more past due, including those in foreclosure), representing a 1.1 percentage point decrease compared to 3.9% in September 2021. The nation’s overall delinquency rate dropped for the 18th straight month on an annual basis.

To gain a complete view of the mortgage market and loan performance health, CoreLogic examines all stages of delinquency. In September 2022, the U.S. delinquency and transition rates, and their year-over-year changes, were as follows:

- Early-Stage Delinquencies (30 to 59 days past due): 2%, up from 1.1% in September 2021.

- Adverse Delinquency (60 to 89 days past due): 4%, up from 0.3% September 2021.

- Serious Delinquency (90 days or more past due, including loans in foreclosure): 2%, down from 2.4% in September 2021 and a high of 4.3% in August 2020.

- Foreclosure Inventory Rate (the share of mortgages in some stage of the foreclosure process): 3%, up from 0.2% in September 2021.

- Transition Rate (the share of mortgages that transitioned from current to 30 days past due): 6%, unchanged from September 2021.

Overall U.S. mortgage delinquencies again hovered near record lows in September, with every state and all but one metro in Illinois posting at least slight annual declines. However, with a potential recession and projected increase in the national unemployment rate looming, some uptick in delinquency rates could be expected in 2023. That said, 99% of homeowners with a mortgage have locked in rates below 6%. As a result, even if delinquency activity posts a minor increase, it is unlikely to cause the type of housing downturn seen during the Great Recession, when questionable underwriting practices allowed buyers to take out mortgages that exceeded their budgets.

“All stages of delinquency remained low in September,” said Molly Boesel, Principal Economist at CoreLogic. “Early-stage, overall and serious delinquencies were either at or below their pre-pandemic rates. Low unemployment, which has also returned to the level seen before the COVID-19 outbreak, is contributing to strong mortgage performance. However, if the U.S. enters a recession, increases in delinquency rates can be expected.”

According to the U.S. Department of Labor (DOL), for the week ending November 19, the advance figure for seasonally adjusted initial unemployment claims was 240,000, an increase of 17,000 from the previous week's revised level. The advance seasonally adjusted insured unemployment rate was 1.1% for the week ending November 12, an increase of 0.1 percentage point from the previous week's unrevised rate. The advance number for seasonally adjusted insured unemployment during the week ending November 12 was 1,551,000, an increase of 48,000 from the previous week's revised level. The previous week's level was revised down by 4,000 from 1,507,000 to 1,503,000. The four-week moving average was 1,509,750, an increase of 28,250 from the previous week's unrevised average of 1,481,500.

In September, all states posted annual declines in overall delinquency rates. The states with the largest declines were Louisiana (down 2.9 percentage points); as well as Hawaii, Nevada, and New Jersey (all 1.8 percentage points). The remaining states, including the District of Columbia, registered annual delinquency rate drops between 1.7 percentage points and 0.3 percentage points.

All but one U.S. metro area posted at least a small annual decrease in overall delinquency rates, with only the Decatur, Illinois metro registering a 0.2 percentage point gain since September 2021.

All U.S. metro areas posted at least a small annual decrease in serious delinquency rates, with Odessa, Texas (down 4.1 percentage points), Laredo, Texas (down 3.2 percentage points) and Midland, Texas (down 2.9 percentage points) posting the largest decreases.