DSNews The homepage of the servicing industry

DSNews The homepage of the servicing industry

While mortgage risk performance has improved significantly over the last few years, the industry should still be watching out for two areas that raise red flags: risk posed to the industry by legacy loans and higher home price correlations in different markets, according to CoreLogic Deputy Chief Economist Sam Khater.

While mortgage risk performance has improved significantly over the last few years, the industry should still be watching out for two areas that raise red flags: risk posed to the industry by legacy loans and higher home price correlations in different markets, according to CoreLogic Deputy Chief Economist Sam Khater.

Indications of improvements in the mortgage risk performances space include tightened underwriting standards compared to the early 2000s, serious delinquencies for recent originations at a 20-year low, home prices increasing at a healthy rate, and default-related metrics such as negative equity, foreclosure starts, and distressed sales all on a steady decline, according to Khater. Also, the overall economy is improving and the job market is tightening.

“Going forward, watch for traditional red flags like employment, job and home price growth,” Khater said. “However, we also have look for non-traditional red flags, like the performance of legacy loans, mortgage transition rates and home price volatility to get an early read on which way the market is heading.”

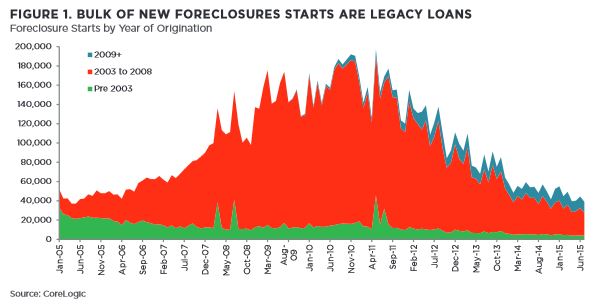

One of the areas that is a cause for concern is legacy loans, Khater said. The percentage of “scratch and dent” loans, which are loans that were 60 or more days delinquent at some point but are now current, is currently reported at 12 percent of all outstanding mortgages, which is lower than its peak of 15 percent in December 2011 but still more than double its normal level of 5 percent.

The majority of these loans were originated during the housing bubble years from 2003 to 2008, a group that made up 62 percent of foreclosure starts in July 2015. By comparison, mortgages originated prior to 2003 made up only 10 percent of foreclosure starts during July.

“In other words, legacy loans are the bad gifts that keep on giving,” Khater said. “The persistence of legacy loans to drive foreclosures a decade later indicates how sensitive mortgage market performance is to underwriting decisions made long ago, even in an otherwise sanguine economic environment. Clearly, this means that a large segment of mortgage loans remains very sensitive to the economy and home prices.”

“In other words, legacy loans are the bad gifts that keep on giving,” Khater said. “The persistence of legacy loans to drive foreclosures a decade later indicates how sensitive mortgage market performance is to underwriting decisions made long ago, even in an otherwise sanguine economic environment. Clearly, this means that a large segment of mortgage loans remains very sensitive to the economy and home prices.”

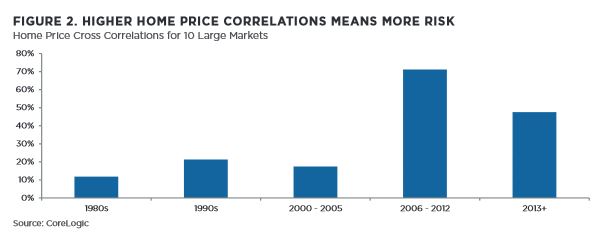

Another area of concern is the affordability of the national housing market. Price volatility is elevated, driven by high home price cross correlations across various markets. Also, the home price to rent ratio has been on the rise since 2012 and is currently very high, Khater said.

The lower end has comprised much of the overall home price appreciation; according to Khater, real lower-end home price growth is currently higher than 10 percent, partially due to the FHA reducing mortgage insurance premiums by 50 basis points at the beginning of the year. But while declining home affordability has been a much-discussed topic among mortgage professionals,

Much of the rise in overall home prices has come from the lower end. Real lower-end home (at 75 percent or less of median sales prices) price growth is currently over 10 percent and it was partly driven by the Federal Housing Administration’s decision to cut premiums earlier this year in the presence of tight supply. While decreasing affordability is not a new topic to be explored, home price cross correlations and volatility have not much less approached topics; Khater said home price correlations for the nation’s 10 largest housing markets markets are three times the rate they have been in the past three decades.

“Higher price cross correlations are driving higher home price volatility,” Khater said. “Real home price volatility, as defined by the standard deviation of the inflation adjusted three-year moving average in price changes, is currently twice the historical average. Higher home price correlations increase home price volatility and risk of national booms and busts because the benefits of geographic diversification is reduced.”

Click here to see CoreLogic’s November 2015 edition of the MarketPulse.