[1]It has been seven years since the mortgage crisis first hit the country, and much has been written about “recovery” for housing and for the consumer lending market. Is that “recovery” finally upon us now?

[1]It has been seven years since the mortgage crisis first hit the country, and much has been written about “recovery” for housing and for the consumer lending market. Is that “recovery” finally upon us now?

According to a study released by TransUnion [2] on Wednesday, yes, the consumer lending market will experience a full recovery from both the mortgage crisis and the subsequent Great Recession by the end of 2016.

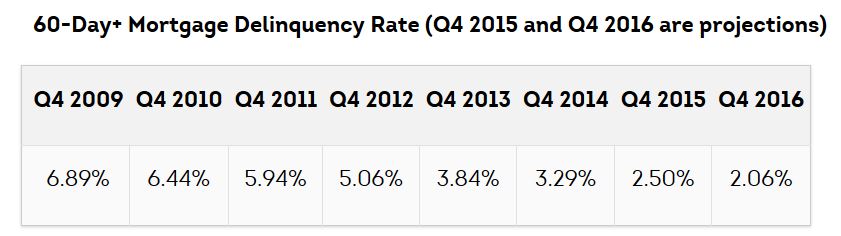

TransUnion predicts that the serious delinquency rate on mortgage loans, which is defined as the percentage of borrowers 60 or more days past due on their mortgage payments, will experience a dropoff from 2.50 percent at the end of 2015 to 2.06 percent at the end of 2016. The serious delinquency rate for mortgages has declined every quarter since hitting a peak of 6.94 percent in Q1 2010, at the height of the housing crisis.

[3] The projected 2.06 percent rate for seriously delinquent mortgage loans would place that number in close proximity to its pre-crisis levels.

[3] The projected 2.06 percent rate for seriously delinquent mortgage loans would place that number in close proximity to its pre-crisis levels.

“We have observed that a ‘normal’ delinquency rate fell between 1.5 and 2 percent in the past, and our forecast puts the nation back at this level,” said Steve Chaouki, EVP and head of TransUnion’s financial services business unit. “Newer vintage mortgage loans have been performing at this level for the last few years, but a combination of factors such as the funneling of bad mortgage loans through the foreclosure process, an improvement in the employment picture and an uptick in housing prices were needed to get back to normal.”

[4]Credit card delinquency rates are expected to be at 1.46 percent at the end of 2016, which would mark their fourth consecutive year at less than 1.5 percent, according to TransUnion.

[4]Credit card delinquency rates are expected to be at 1.46 percent at the end of 2016, which would mark their fourth consecutive year at less than 1.5 percent, according to TransUnion.

“Both the mortgage and credit card markets are performing extremely well, with increased consumer participation and continued low delinquency rates,” said Ezra Becker, VP of Research and Consulting with TransUnion’s financial services business unit. “Millions of borrowers have gained access to credit card loans in just the past few years. And despite the fact that more consumers—and more non-prime consumers—are entering the housing market, delinquency levels have remained in check and balances are growing. This points to responsible lending practices and a consumer base that is clearly in a better position to make payments on their loans.”

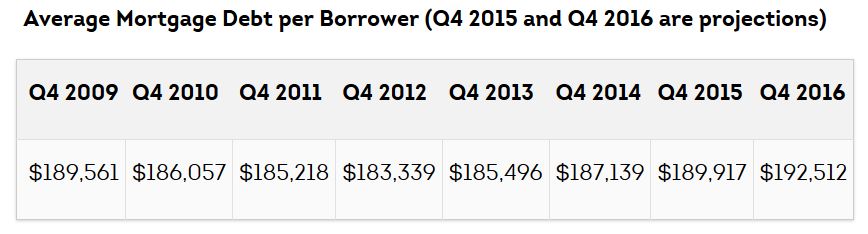

A rebound in housing prices has partly driven an increase in mortgage debt per borrower, which is expected to jump by about $9,000 up to $192,500 by the end of 2016 from its low point of $183,300 reached at the end of 2012, according to TransUnion.

“This is a clear indicator that housing prices are recovering and consumers are gaining access to more mortgage loans,” Chaouki said. “Fannie Mae’s recent announcement that it would use trended data in the assessment of mortgage applicants could also very well boost mortgage originations in the second half of 2016.”

The number of mortgage accounts nationwide has remained relatively low for the last three years, according to TransUnion data; there were 52.6 million mortgage accounts as of the end of Q3 2015, which was about 7 million fewer than there were in Q3 2009. Though the number has remained low, it has seen some growth in the last two years, TransUnion reported.

“We are a long way from returning to pre-recession levels in terms of mortgage accounts, but changing consumer preferences for housing also may play a role in this slow recovery,” Chaouki said. “If the economy continues to perform well, we believe the net number of mortgages will increase over the next year.”