DSNews The homepage of the servicing industry

DSNews The homepage of the servicing industry

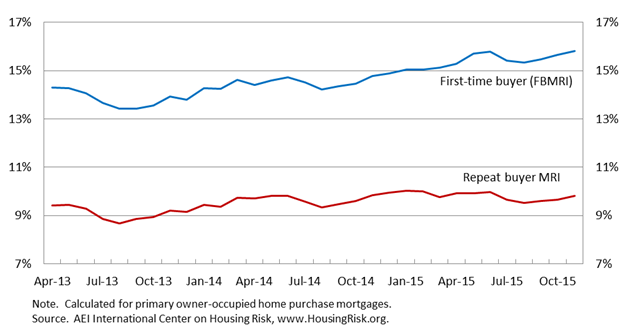

The gap between Agency indices measuring risk of default for first-time homebuyers compared to repeat buyers is widening, according to data released by the American Enterprise Institute (AEI)’s International Center on Housing Risk on Monday.

The gap between Agency indices measuring risk of default for first-time homebuyers compared to repeat buyers is widening, according to data released by the American Enterprise Institute (AEI)’s International Center on Housing Risk on Monday.

The AEI’s Agency First-Time Buyer Mortgage Risk Index (FBMRI), which estimates the share of first-time buyer mortgages that would default if the U.S. economy experienced economic stress or a downturn similar to conditions in 2007 and 2008, found that the Agency FBMRI for first-time buyers is currently 6 percentage points higher than the risk index for repeat homebuyers and the gap has been growing.

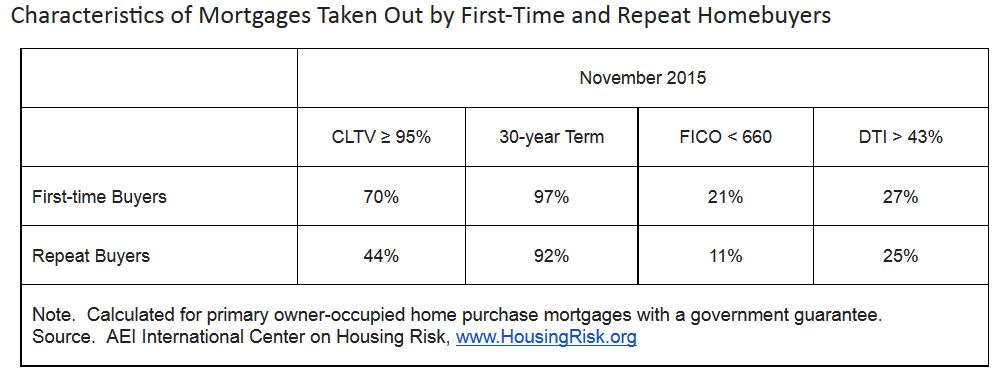

What is the reason for the widening gap? According to AEI, it is largely driven by risk layering. As of the end of November 2015, about 70 percent of first-time buyer mortgages had a combined loan-to-value ratio of higher than 95 percent. According to AEI, about 97 percent of those first-time buyers had a 30-year term mortgage.

“Given the combination of little money down and slow amortization, these buyers will have very little home equity for a number of years unless their house appreciates substantially,” AEI stated in the report.

“Given the combination of little money down and slow amortization, these buyers will have very little home equity for a number of years unless their house appreciates substantially,” AEI stated in the report.

In November 2015, the down payment for a median first-time homebuyer with an agency mortgage was only 3 percent, which calculates to about $7,200. That group also had a median FICO score of 706, which is 7 points lower than the national average of all individuals in the U.S. with a score, which was 713. For first-time buyers with FHA loans in November, the median FICO score was only 676—suggesting that mortgage credit access for first-time buyers may not be as tight as some news cycles have been suggesting.

“The typical first-time buyer these days puts little money down and has a credit profile that is far from stellar,” said Stephen Oliner, codirector of AEI’s International Center on Housing Risk. “Those who assert that credit is tight are ignoring the facts.”

According to AEI, About one-fifth of first-time buyers had a FICO score below 660 (the traditional definition of subprime mortgages), and more than one-quarter of them had total DTI ratios of higher than 43 percent, which is the limit set by the government’s qualified mortgage rule.