DSNews The homepage of the servicing industry

DSNews The homepage of the servicing industry

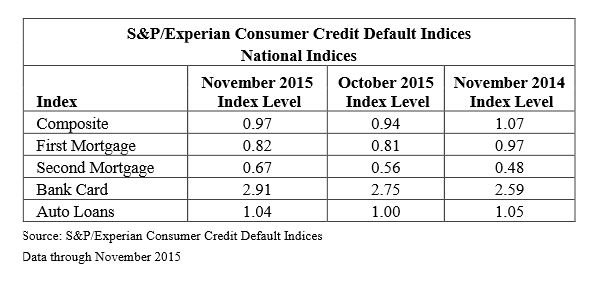

Consumer credit default rose for the second consecutive month in November, which is cause to keep a close eye on consumer finances in the coming year, according to the S&P Dow Jones Indices and S&P/Experian Consumer Credit Default Indices for November 2015 released Tuesday.

Consumer credit default rose for the second consecutive month in November, which is cause to keep a close eye on consumer finances in the coming year, according to the S&P Dow Jones Indices and S&P/Experian Consumer Credit Default Indices for November 2015 released Tuesday.

The composite rate rose by 3 basis points from October to November, up to 0.97 percent, while the first mortgage rate crept up by one basis point from 0.81 to 0.82 percent and the second mortgage rate spiked by 11 basis points up to 0.67 percent during that same period. The remaining two indices that make up the composite rate, auto loans and bank cards, climbed by four basis points (to 1.04 percent) and 16 basis points (up to 2.91 percent), respectively, from October to November.

November’s increases for the first and second mortgage default rates came after an October that saw those rates jump by five basis points and nine basis points, respectively, month-over-month.

“November was the second consecutive month when default rates rose across all types of consumer credit,” says David M. Blitzer, Managing Director and Chairman of the Index Committee at S&P Dow Jones Indices. “While two months isn’t long enough to establish a turning point or a new trend, the consumers’ financial condition should be watched going forward. Consumer spending has been a key source of growth for the economy.”

The good news for the default indices is that despite the monthly increases for the second straight month, the composite index was down by 10 basis points year-over-year (1.07 to 0.97) and the first mortgage default index was down by 15 basis points (0.97 down to 0.82). Blitzer said the recent monthly increases “are small compared to past moves and are well within a range of random monthly shifts.”

“Other factors do not suggest any cause for concern over consumer credit defaults: inflation remains low and expectations of future inflation are low and stable, the labor market continues to improve, and wages—long dormant—may be turning upward,” Blitzer said. “Continued weakness in oil prices are adding to disposable income.”

“Other factors do not suggest any cause for concern over consumer credit defaults: inflation remains low and expectations of future inflation are low and stable, the labor market continues to improve, and wages—long dormant—may be turning upward,” Blitzer said. “Continued weakness in oil prices are adding to disposable income.”

The second default mortgage index was up by 19 basis points year-over-year in November 2015 (0.48 up to 0.67). The historic lows for the first and second mortgage default rates are 0.74 percent and 0.42 percent, respectively, both reached in May 2015. The S&P/Experian Consumer Credit Default Indices were launched in May 2010.