DSNews The homepage of the servicing industry

DSNews The homepage of the servicing industry

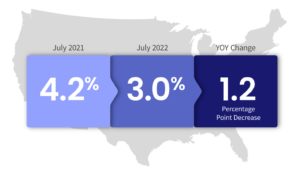

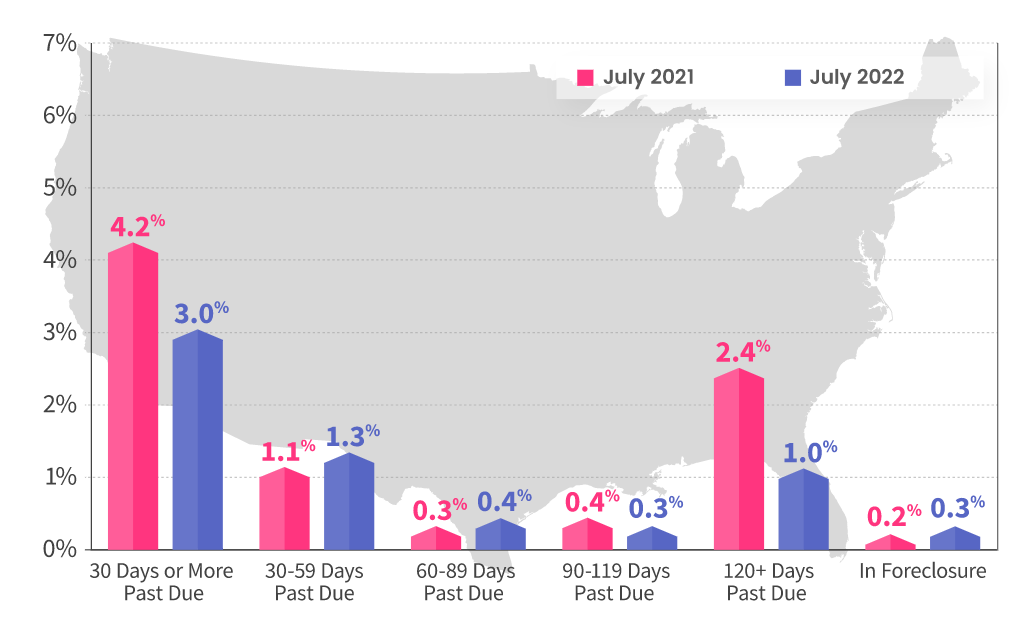

CoreLogic’s Loan Performance Insights Report for July 2022 has found that for the month of July 2022, 3% of all mortgages in the U.S. were in some stage of delinquency (30 days or more past due, including those in foreclosure), representing a 1.2-percentage point decrease compared to 4.2% in July 2021.

CoreLogic’s Loan Performance Insights Report for July 2022 has found that for the month of July 2022, 3% of all mortgages in the U.S. were in some stage of delinquency (30 days or more past due, including those in foreclosure), representing a 1.2-percentage point decrease compared to 4.2% in July 2021.

The data in this report accounts for only first liens against a property and does not include secondary liens. The delinquency, transition and foreclosure rates are measured only against homes that have an outstanding mortgage. Homes without mortgage liens are not subject to foreclosure and are, therefore, excluded from the analysis.

“Early-stage delinquencies are showing a small but clear increasing trend on a month-over-month and year-over-year basis,” said Molly Boesel, Principal Economist at CoreLogic. “While the share of mortgages that are 30 to 89 days past due remains below the pre-pandemic level, the slight increase is occurring in most areas of the country and could indicate that more borrowers are having trouble making their monthly payments.”

Although overall U.S. mortgage delinquencies crept up again in July from earlier in 2022, they declined for the 16th straight month year-over-year and remained near historic lows. The national foreclosure rate has held steady at 0.3% since March, but rose by 0.1-percentage point from July 2021. This slight bump mirrors metro-level trends, with almost two-thirds of areas that CoreLogic tracks posting small annual foreclosure gains. The minor uptick in foreclosures may be due to mortgage forbearance periods and moratoriums ending for some homeowners, while the increase in delinquencies could indicate that inflation is negatively impacting others’ abilities to make monthly payments.

Early-stage delinquencies, those 30 to 59 days past due, stood at 1.3%, up from 1.1% in July 2021. Those measured as “Adverse Delinquency,” or 60 to 89 days past due, measured 0.4%, up from 0.3% in July 2021.

Mortgage loans deemed in “Serious Delinquency,” 90 days or more past due, including loans in foreclosure, stood at 1.3%, down from 2.8% in July 2021, and a high of 4.3% in August 2020.

The Foreclosure Inventory Rate, representing the share of mortgages in some stage of the foreclosure process, was at 0.3% in July 2022, up from 0.2% in July 2021, while the Transition Rate, measured as the share of mortgages that transitioned from current to 30 days past due, stood at 0.7%, up from 0.6% year-over-year in July 2021.

Regionally, all states posted annual declines in their overall delinquency rates in July of 2022. The states with the largest declines were Hawaii and Nevada (both down 2.3 percentage points), New Jersey (down 2.1 percentage points), and New York (down 2.0 percentage points), the third consecutive month that these states have led the country for delinquency declines. The remaining states, including the District of Columbia, registered annual delinquency rate drops between 1.9 percentage points and 0.2 percentage points. All but eight U.S. metro areas posted a small annual decrease in overall delinquency rates, with increases in those metros ranging from 0.1 percentage points to 0.4 percentage points.

All U.S. metro areas posted at least a small annual decrease in serious delinquency rates, with Odessa, Texas (down 4.7 percentage points); Laredo, Texas (down 3.7 percentage points) and Kahului-Wailuku-Lahaina, Hawaii (down 3.6 percentage points) posting the largest decreases.