DSNews The homepage of the servicing industry

DSNews The homepage of the servicing industry

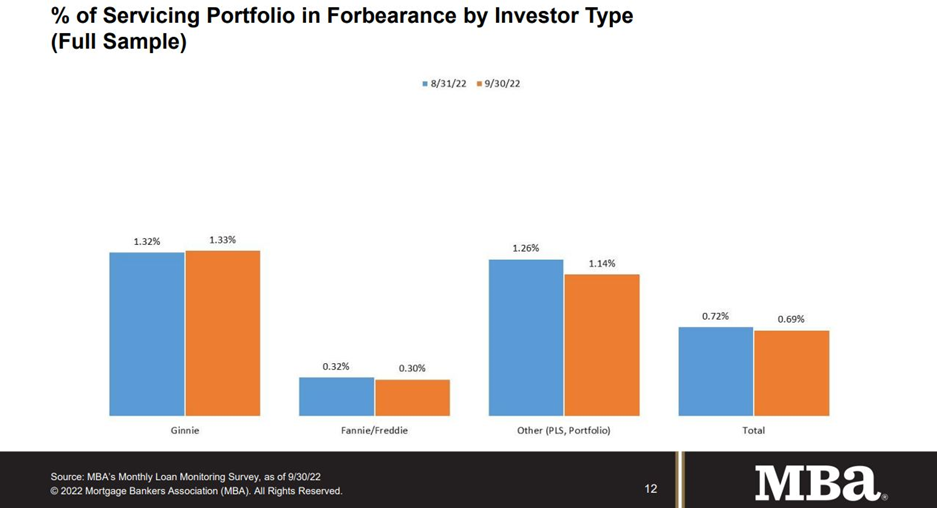

The Mortgage Bankers Association (MBA) has reported that the total number of loans now in forbearance as of September 30, 2022 fell by three basis points from 0.72% of servicers’ portfolio volume in the prior month to 0.69%. The MBA estimates there are currently 345,000 U.S. homeowners in forbearance plans.

The Mortgage Bankers Association (MBA) has reported that the total number of loans now in forbearance as of September 30, 2022 fell by three basis points from 0.72% of servicers’ portfolio volume in the prior month to 0.69%. The MBA estimates there are currently 345,000 U.S. homeowners in forbearance plans.

In the MBA’s latest Loan Monitoring Survey, the share of Fannie Mae and Freddie Mac loans in forbearance decreased two basis points from 0.32% to 0.30%, while Ginnie Mae loans in forbearance increased one basis point from 1.32% to 1.33%. The forbearance share of portfolio loans and private-label securities (PLS) declined 12 basis points from 1.26% to 1.14%.

“The overall number of loans in forbearance dropped in September, but the pace of forbearance exits slowed to a new survey low and new forbearance requests continued to come in. This dynamic in turn prevented any substantial improvement in the forbearance rate,” said Marina Walsh, CMB, MBA’s VP of Industry Analysis. “The COVID-19 federal health emergency is still in effect and in most cases, borrowers can still seek initial COVID-19 hardship forbearance.”

One event which impacted the nation in September which may cause a rise in the number of forbearances is the wreckage left behind by Hurricane Ian. Updated estimates from CoreLogic of the damage and loss totals from Hurricane Ian found that total flood and wind losses will total in the $41-$70 billion range, making Hurricane Ian the costliest Florida storm since Hurricane Andrew made landfall in 1992.

“In the near-term, the number of loans in forbearance will likely increase for another reason–the recent devastation caused by Hurricane Ian in Florida, South Carolina, and other states,” added Walsh. “MBA’s Loan Monitoring Survey requests that servicers report all loans in forbearance regardless of the borrower’s stated reason–whether pandemic-related, due to a natural disaster, or another cause.”

Total completed loan workouts from 2020 and onward (repayment plans, loan deferrals/partial claims, loan modifications) that were current as a percent of total completed workouts increased to 78.70% last month from 78.31% in August.

Of the cumulative forbearance exits for the period from June 1, 2020, through September 30, 2022, at the time of forbearance exit:

- 6% resulted in a loan deferral/partial claim.

- 3% represented borrowers who continued to make their monthly payments during their forbearance period.

- 3% represented borrowers who did not make all of their monthly payments and exited forbearance without a loss mitigation plan in place yet.

- 0% resulted in a loan modification or trial loan modification.

- 0% resulted in reinstatements, in which past-due amounts are paid back when exiting forbearance.

- 6% resulted in loans paid off through either a refinance or by selling the home.

- The remaining 1.2% resulted in repayment plans, short sales, deed-in-lieus or other reasons.

Regionally, the five states with the highest share of loans that were current as a percent of servicing portfolio included:

- Idaho

- Washington

- Colorado

- Utah

- Oregon

The five states reporting the lowest share of loans that were current as a percent of servicing portfolio:

- Mississippi

- Louisiana

- New York

- West Virginia

- Indiana