DSNews The homepage of the servicing industry

DSNews The homepage of the servicing industry

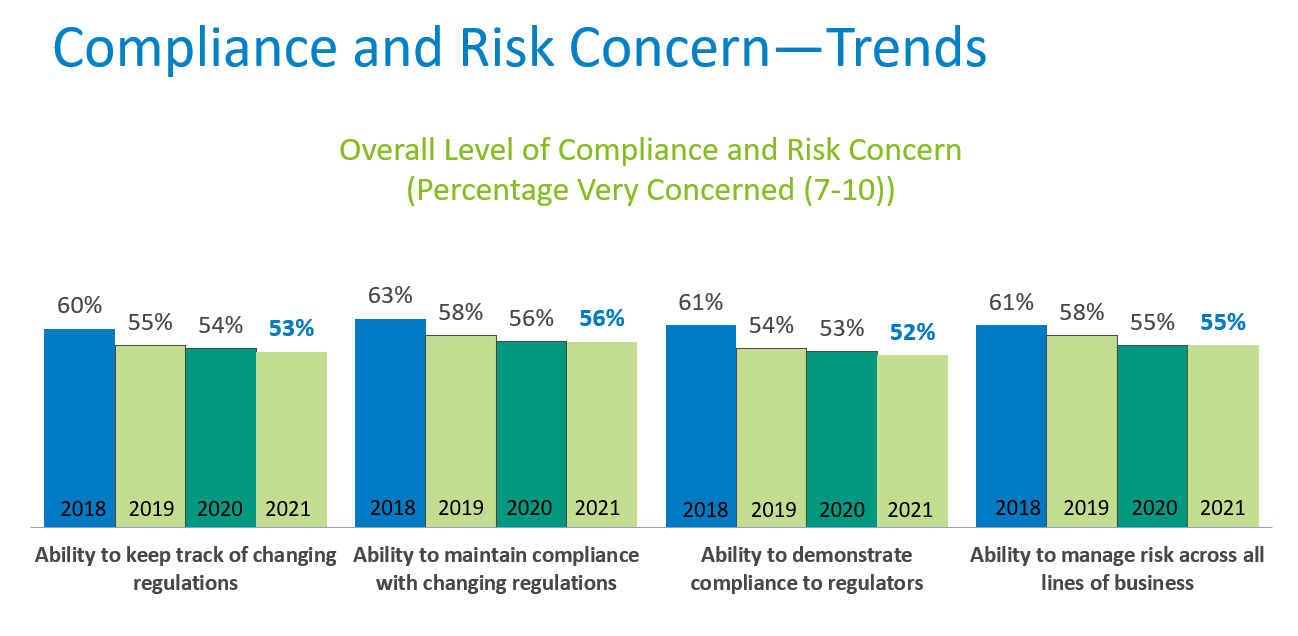

According to the latest Wolters Kluwer’s 2021 Regulatory & Risk Management Indicator, regulatory compliance and risk concerns remain elevated in a number of key areas for U.S. banks and credit unions.

According to the latest Wolters Kluwer’s 2021 Regulatory & Risk Management Indicator, regulatory compliance and risk concerns remain elevated in a number of key areas for U.S. banks and credit unions.

Conducted by Wolters Kluwer Compliance Solutions, continuing concerns about navigating regulatory changes, managing risk across all lines of business, and an increase in the dollar amount of fines imposed by regulators all resonated as areas of concern amongst those polled.

The threat of ransomware attacks led the list of factors in organizations’ enterprise risk planning, with 63% giving it “significant consideration,” and another 22% marking it for “some consideration” in their planning. The pandemic’s ongoing impacts continued to weigh heavily on respondents’ minds with 49% citing it as a significant concern in enterprise risk planning, followed by loan default risk (46%), and inflation concerns (42%). Other areas of concern include business resilience and adaptability (41%), recession fears (34 %), and climate-related financial risks (21%).

“Relatively high levels of concern remain across a range of areas, reinforcing the fact that regulatory compliance and risk management issues continue to pose challenges for financial institutions,” said Timothy R. Burniston, Senior Advisor for Regulatory Strategy with Wolters Kluwer Compliance Solutions. “Respondents expressed their highest levels of confidence in the past four years regarding their organizations’ ability to track regulatory changes and document compliance with those requirements to regulators. Nonetheless, the level of concern is still high.”

Among the top obstacles cited in implementing effective compliance programs, 45% of respondents ranked manual compliance processes as a “7” or higher concern on a 10-point scale, and 41% cited inadequate staffing, virtually the same as 2020’s levels. Of those polled 41% felt that regulatory scrutiny of fair lending programs remained unchanged, down just 1% from last year’s survey.

When asked about the prospects for reduced regulatory burden over the next two years, respondents revealed greater pessimism, with 72% citing the likelihood of regulatory relief as either “somewhat unlikely,” or “very unlikely” compared to 56% in 2020.

“The concerns expressed by survey respondents reflect another year of challenges for the U.S. banking industry as it navigates through the pandemic—and the evolving regulatory and risk landscape,” said Steven Meirink, EVP and General Manager for Wolters Kluwer Compliance Solutions. “The industry’s resiliency has enabled it to address these challenges admirably, and we continue to support our clients in staying compliant so they can serve customers with confidence.”

Looking forward to 2022, top risk management priorities identified include cybersecurity (70%), compliance risk and credit risk (both at 43%), with concerns about credit risk having decreased 18 percentage points from 2020’s survey results. More than 45% of respondents anticipate an acceleration of investments in their regulatory change management processes.

Respondents cited the following as the most pressing regulatory compliance challenges over the next year:

- Bank Secrecy Act/Anti-Money Laundering requirements

- Forthcoming Beneficial Ownership requirements

- Fair lending laws and regulations, along with Dodd-Frank Section 1071 small business reporting rules

- UDAAP standards and looming Community Reinvestment Act (CRA) rule changes

- Current Expected Credit Losses (CECL) standards

- State-issued regulatory requirements

Click here for more information on Wolters Kluwer’s 2021 Regulatory & Risk Management Indicator survey.