DSNews The homepage of the servicing industry

DSNews The homepage of the servicing industry

“Not so fast!” said the buyer to the seller …

“Not so fast!” said the buyer to the seller …

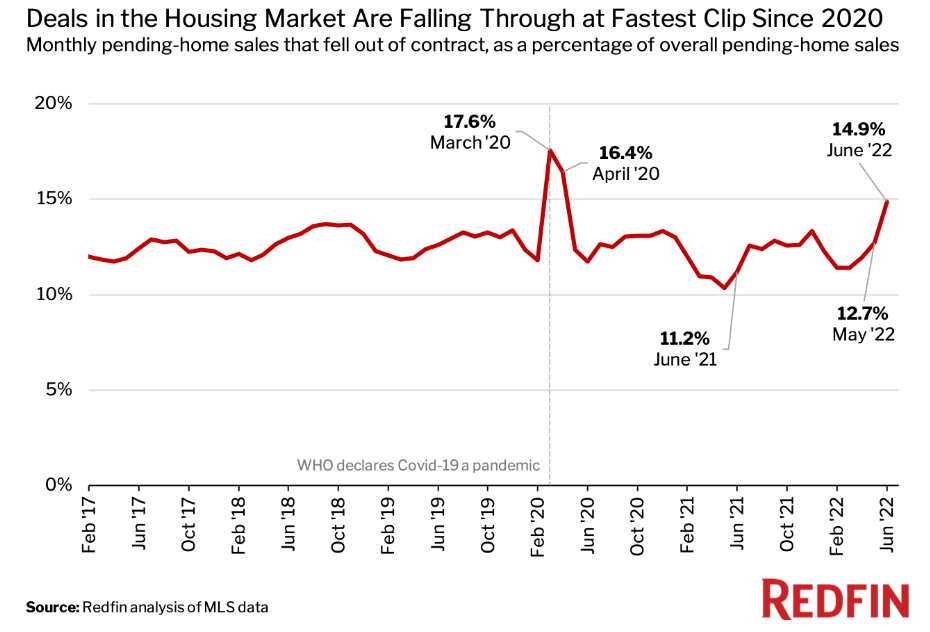

A new analysis of MLS data by Redfin has found that roughly 60,000 of home-purchase agreements fell through in June, equal to 14.9% of homes that went under contract that same month, marking the highest percentage since March and April 2020, when the housing market all but ground to a halt due to the onset of the pandemic. This total compares with 12.7% a month earlier, and 11.2% a year earlier.

“The slowdown in housing-market competition is giving homebuyers room to negotiate, which is one reason more of them are backing out of deals,” said Redfin Deputy Chief Economist Taylor Marr. “Buyers are increasingly keeping rather than waiving inspection and appraisal contingencies. That gives them the flexibility to call the deal off if issues arise during the homebuying process.”

Redfin notes that the housing market has cooled in recent weeks as the Federal Reserve has taken action to hike interest rates to slow inflation. That has given house hunters more freedom to seek concessions from sellers, but higher rates also make housing less affordable. Buyers did get a slight reprieve this past week, when the average 30-year fixed-rate mortgage (FRM) fell to 5.30% for the week ending July 7, 2022, according to Freddie Mac’s Primary Mortgage Market Survey (PMMS).

Soaring housing costs caused many house hunters to drop out in recent weeks, but Redfin recently reported that the share of sellers slashing their asking prices hit a record high during the four weeks ending July 3, and the portion of homes going for above list price fell for the first time since June 2020, as sellers are beginning to heed the call of diminishing homebuyer demand.

“Rising mortgage rates are also forcing some buyers to cancel home purchases,” said Marr. “If rates were at 5% when you made an offer, but reached 5.8% by the time the deal was set to close, you may no longer be able to afford that home or you may no longer qualify for a loan.”

Compounding matters for these seller who have had buyers withdraw their offers, Redfin also reported that fewer people searched for “homes for sale” on Google, searches during the week ending July 2 were down 2% year-over-year. Redfin’s Homebuyer Demand Index—a measure of requests for home tours and other home-buying services from Redfin agents—was also down 15% year-over-year during the week ending July 3, while touring activity as of July 3 was down 14% from the start of the year, compared to a 7% increase at the same time last year, according to home tour technology company ShowingTime.

“When mortgage rates shot up to almost 6% in June, we saw a number of buyers back out of deals,” said Lindsay Garcia, a Miami-based Redfin Real Estate Agent. “Some had to bow out because they could no longer get a loan due to the jump in rates. Buyers are also more skittish than usual due to economic uncertainty.”