DSNews The homepage of the servicing industry

DSNews The homepage of the servicing industry

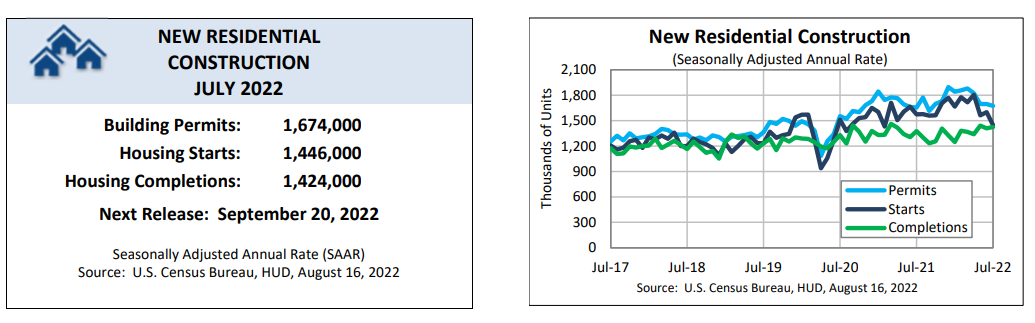

The U.S. Census Bureau and the U.S. Department of Housing & Urban Development (HUD) have announced its new residential construction data for July 2022, reporting that privately‐owned housing starts in July were at a seasonally adjusted annual rate of 1,446,000—9.6% below the revised June estimate of 1,599,000, and 8.1% below the July 2021 rate of 1,573,000.

The U.S. Census Bureau and the U.S. Department of Housing & Urban Development (HUD) have announced its new residential construction data for July 2022, reporting that privately‐owned housing starts in July were at a seasonally adjusted annual rate of 1,446,000—9.6% below the revised June estimate of 1,599,000, and 8.1% below the July 2021 rate of 1,573,000.

Single‐family housing starts in July were at a rate of 916,000—10.1% below the revised June figure of 1,019,000. The July rate for units in buildings with five units or more was 514,000.

“U.S. housing starts were expected to fall to an annual pace of 1.52 million in July, but instead fell further, coming in at 1.45 million,” said First American Deputy Chief Economist Odeta Kushi. “The decrease in single-family housing starts mirrors the decline in homebuilder confidence, which turned negative in August, driven by declines in all three components of the index: current single-family home sales, future sales expectations, and traffic of prospective buyers.”

The National Association of Home Builders (NAHB) reported that builder confidence fell for the eighth straight month in August, with volatile mortgage rates, continued supply chain issues, and record high home prices continuing to exacerbate housing affordability challenges.

“Builder confidence slipped for an eighth month in August as traffic from potential new homebuyers continued to deteriorate, mirroring similar concerns among a broad set of homebuying consumers about high home prices, elevated mortgage rates, and an uncertain economic outlook,” said Danielle Hale, Chief Economist for Realtor.com. “Alongside confidence, single-family permits declined from last month and one year ago, while multifamily permits grew in the same periods. The increase in multifamily permits was not quite enough to offset single-family declines in July, and overall permits dropped 1.3% in the month but are up 1.1% from a year ago.”

HUD and the Census Bureau reported that privately‐owned housing completions in July were at a seasonally adjusted annual rate of 1,424,000, 1.1% above the revised June estimate of 1,409,000, and 3.5% above the July 2021 rate of 1,376,000. Single‐family housing completions in July were at a rate of 1,009,000—0.8% below the revised June rate of 1,017,000. The July rate for units in buildings with five units or more was 412,000.

“Housing is a primary transmission mechanism for the Federal Reserve and, as monetary tightening has intensified, so has the impact to homebuilding,” added Kushi. “Builders are responding to a pullback in demand, as rising mortgage rates have dampened affordability and caused would-be buyers to sit on the sidelines.”

Also in July, privately‐owned housing units authorized by building permits were at a seasonally adjusted annual rate of 1,674,000—1.3% below the revised June rate of 1,696,000, but 1.1% above the July 2021 rate of 1,655,000. Single‐family authorizations in July were at a rate of 928,000, which is 4.3% below the revised June figure of 970,000. Authorizations of units in buildings with five units or more were at a rate of 693,000 in July.

Doug Duncan, Chief Economist at Fannie Mae, noted, "On a more positive note, single-family completions hit six consecutive months above a seasonally adjusted annualized rate (SAAR) of one million and are 7% above their July 2021 level. We believe this is evidence of a gradual easing to supply chain issues that have plagued home builders for months, an encouraging sign that more new homes will be ready for move-in in the coming months.”

“With homeowner and rental vacancy rates hovering at or near record lows, the housing supply gap continues to impact the housing market,” said Hale. “Home prices generally continue to climb, albeit at a slightly slower pace. Meanwhile, rents also hit new highs, and are only very gradually losing upward momentum. Builders are working to fill the gap, while managing the shift in demand for housing. The seasonally adjusted number of units under construction in July (1.678M) was just shy of June’s all-time record (1.68M), driven by large numbers of single-family and 5+ unit buildings. As these projects are completed, they will add to supply, ensuring that the return to balance in the housing market is driven by an increase in for-sale options as well as demand that has been moderated by higher mortgage rates.”

As more are re-considering purchasing in the current market due to rate and price instability, many have no choice but to rent until the time is right to jump into purchasing a home.

The National Association of Realtors (NAR) reported that price of a median single-family home in Q1 hit $400,000 for the first time on record—then surpassed it—finally settling at $413,500 by the end of Q1. And after hitting a four-month low the previous week, erratic mortgage rates leapt back above the 5%-mark, rising to 5.22% last week, according to Freddie Mac.

“The rental and purchase markets are inextricably tied together–a household chooses to rent or buy a home, substituting one for the other based on market conditions, cost effectiveness and lifestyle preferences,” added Kushi. “Would-be home buyers priced out of the purchase market may add to rental demand.”