Almost 8 million homes with more than $1.9 trillion in reconstruction cost value are at risk of storm surge damage in 2021, according to the 2021 Hurricane Report [1] from property data analytics provider CoreLogic.

Almost 8 million homes with more than $1.9 trillion in reconstruction cost value are at risk of storm surge damage in 2021, according to the 2021 Hurricane Report [1] from property data analytics provider CoreLogic.

The report—focused on single and multifamily residences along the Gulf and Atlantic coasts—takes a closer look at how the hurricane damage to a property affects the owner's ability to pay the mortgage. It also examines the impact of hurricanes on the nation's housing supply, which is already alarmingly short.

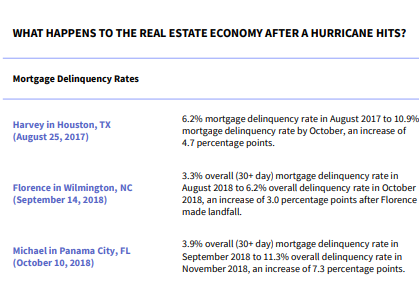

For homeowners, the result of a financial catastrophe results in a significant increase in mortgage delinquency rates as people, crippled by expenses and lost wages, fail to make monthly payments, according to the report. After Hurricane Laura made landfall in Lake Charles, for example, the already-elevated delinquency rate went up from 9.8% in August 2020 to 16.1% in September 2020, an increase of 6.3 percentage points, according to the report.

“To provide a 360-degree view of the impact of climate change, we took a look at the U.S. housing economy after a hurricane strikes and noticed a significant spike in mortgage delinquency rates and loss in housing inventory,” said Frank Nothaft, Chief Economist at CoreLogic. “Communities most affected by natural and financial catastrophe include those with already-high delinquency rates such as in Lake Charles, Louisiana, as reflected in the pre- and post-Hurricane Laura landfall rates.”

Last week we listened in as CoreLogic held its webinar on hurricanes and climate change [2] and panelists discussed why assessing hurricane risk is so important for financial institutions, borrowers, and whole communities.

"We've already established that 2020 and previous years have been record-breaking financial impacts across many communities," said George Gallager, Principal, Hazard and Spatial Solutions. "I summarize this as a key reminder we cannot overlook the human impact and community impact that devastating hurricanes and other natural disasters have on borrowers homeowners and the communities they live in."

Historically, housing inventory is depleted following a categorized storm. After Harvey, for instance, Houston, Texas experienced a 23% decrease in its supply over the next five months. Wilmington, North Carolina lost 26% of its stock in four months following Florence in 2018. Panama City, Florida's inventory dipped 13% in the two months after Hurricane Michael in 2018.

As climate change continues to affect the way storms present, the risk in these hurricane-prone areas will continue to increase, according to the report's authors: Tom Larsen, Dr. Thomas Jeffery, Rhea Turakhia, Denise Moore, Molly Boesel,

Elizabeth Greeves, Maiclaire Bolton Smith, and Jose Acosta.

"Based on data from NOAA National Centers for Environmental Information, over the past four decades we've seen a 70-90% increase every decade in total inflation-adjusted losses from weather events in the United States—and this trend isn’t slowing down."

They say the trend toward migrating [3] out of city centers to coastal towns could cause more households to be at-risk.

These areas are typically low-lying, hurricane-prone and especially subject to the climate-related factors at play including, sea-level rise, extreme rainfall events, and possible increases in hurricane intensity, according to the hurricane report.

The resilience of these coastal communities—high income or low—continues to be a focal point of prevention and preparation.

"The only way forward is to understand what really is at risk and educate, prepare and collaborate with

everyone who has a stake in the ongoing crisis, including insurance companies, lenders, government agencies, and the families on the front line," they noted.

Access the full report [1], which provides insight into property risk, both nationally and by metro area via CoreLogic.com.