DSNews The homepage of the servicing industry

DSNews The homepage of the servicing industry

While rural areas of the United States have maintained the same approximate population (54 million in 1960 and 57 million in 2020), urban areas have gained nearly 150 million inhabitants in the last six decades, according to a study by The Zebra, a home insurance comparison site. Analysts for The Zebra dove deep into today's most pressing housing matters to understand how they compare to the same issues some 60 years ago.

While rural areas of the United States have maintained the same approximate population (54 million in 1960 and 57 million in 2020), urban areas have gained nearly 150 million inhabitants in the last six decades, according to a study by The Zebra, a home insurance comparison site. Analysts for The Zebra dove deep into today's most pressing housing matters to understand how they compare to the same issues some 60 years ago.

"We wanted to dig deeper into the ways that housing has affected the lives of Americans both historically and in the present," The Zebra's researchers said. "Using U.S. Census Bureau data, we explored how housing has changed for Americans since 1960."

And here are some of the main things The Zebra's analysts discovered:

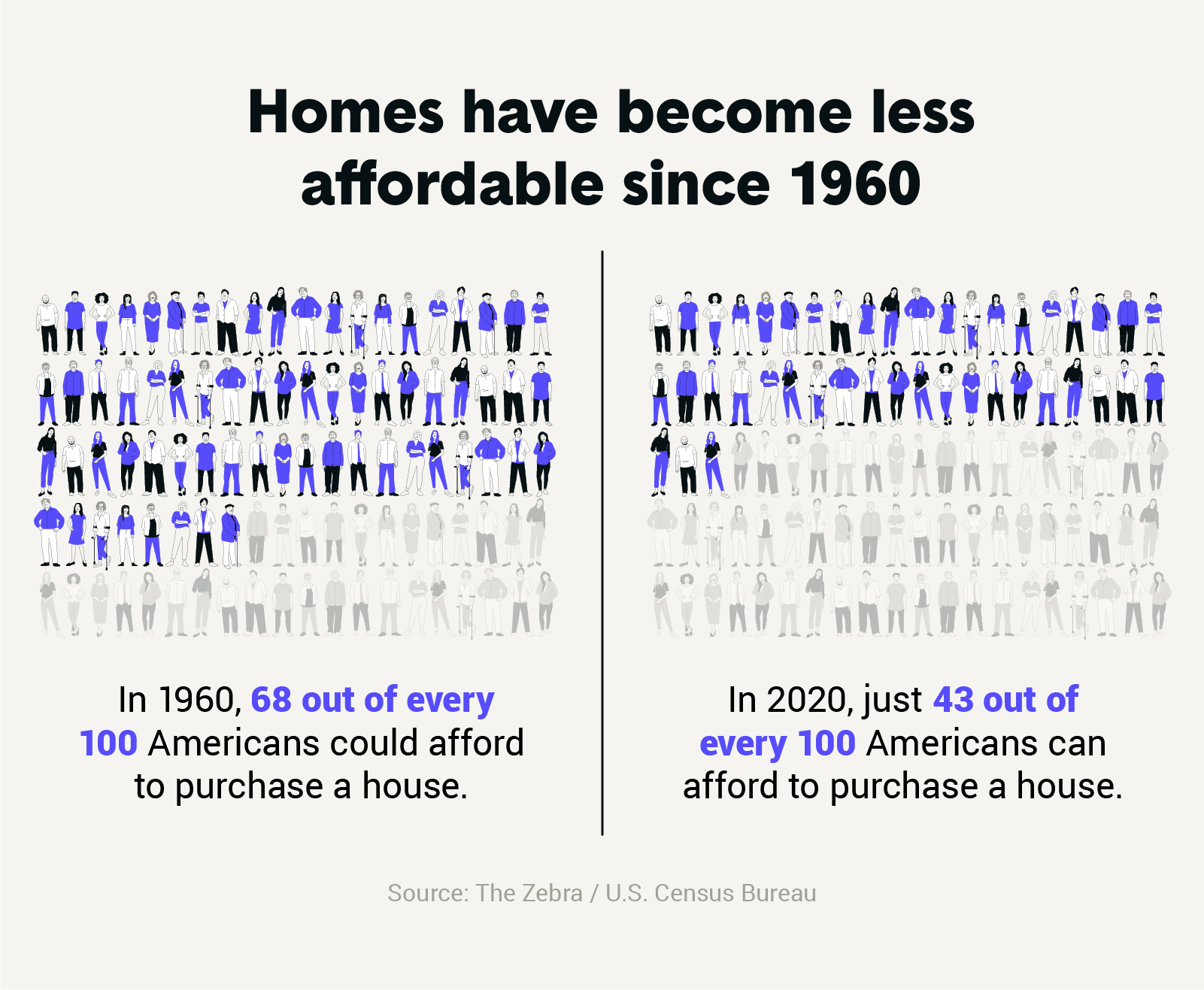

- An increasingly unaffordable dream of homeownership — 3 million homeowners will have delinquent mortgages in 2021; 5% of homeowners are in serious danger of losing their homes; communities of color are disproportionately affected by issues of housing security, with Black and Latinx individuals making up 80% of those facing eviction.

One common measure of housing affordability is the relationship between the median cost of a home and the median income (price-to-income ratio). The Zebra used Census intel to calculate the price-to-income ratio for Americans in 1960 as well as 2019 and found that in 1960, the median home cost $11,900, while the median income was $5,600, indicating a price-to-income ratio of 2.1. By contrast, in 2019 the median home cost $240,500 with an estimated median income of $68,703, a price-to-income ratio of 3.5.

- Housing costs have far exceeded growth in wages — the median house of 1960 would cost just $104,619 in 2020 dollars, far below the actual cost of $240,500, meaning housing costs have increased by 229%. Median household income has only grown by 140% in that same time period, from $49,232 (2020 dollars) in 1960 to $68,703 today.

Black Americans face an even greater challenge when it comes to housing affordability, as Black families earn an average of $29,000 less annually than white families, which would represent a price-to-income ratio of 6.1.

- Racial disparity has widened since 1960 — Citing a report from the U.S. Department of Housing and Urban Development (HUD), The Zebra reported that, while both white and Black Americans now have higher homeownership rates than they did in 1960, the gap between these two groups has widened.

In 1960, 64.4% of white Americans and 38.4% of Black Americans owned homes, a difference of 26 percentage points. In 2020, 75.8% of white Americans and 46.4% of Black Americans owned homes, a difference of 29.4 percentage points.

- More single women own homes — Less than 0.1% of women ages 18–34 lived alone in their own homes 60 years ago, but that same group now represents 1% of all homeowners in the United States.

- Living alone is more common among all Americans — just 6.4% of Americans lived alone in 1960, whereas 28.3% of Americans now live alone.

- Fewer Americans live with spouses — more than 70% of Americans lived with a spouse in 1960, but today that group comprises only 51.5% of adults. By contrast, many more Americans now live as unmarried partners — 7.3% in 2020 compared to only 0.4% 60 years ago.

- More than half of all young Americans now live with their parents — Among 18 to 34 year olds, nearly twice as many people live at home with their parents in 2020 than in 1960. 22% of 18-34 year old men live at home now as opposed to just 10.9% in 1960.

- Older Americans live alone rather than with family — in 1960, 20% of men and 40% of women over age 75 lived with their families. In 2020, just 6% of men and 19% of women over 75 live with their families. Today, one of every two older American women live alone, and 4.5% of all Americans over 65 live in nursing homes or other similar facilities.

The authors of the report surmise that 2021 presents its share of obstacles for Americans who hope to achieve and maintain homeownership and those who represent them.

"With growing housing issues related to affordability, foreclosure, eviction, racial disparity and homelessness, the coming years represent a formidable challenge for politicians and community leaders hoping to provide stable lives for Americans," the researchers conclude.