DSNews The homepage of the servicing industry

DSNews The homepage of the servicing industry

When the coronavirus pandemic prevented many Americans from working, many wondered what would happen in the housing market. After all, no employment, no paycheck, no paying the mortgage. The Federal Housing Finance Agency (FHFA) says that calculating the number of Americans who are having difficulty paying for their homes may be difficult considering new rules and regulations related to the pandemic response.

When the coronavirus pandemic prevented many Americans from working, many wondered what would happen in the housing market. After all, no employment, no paycheck, no paying the mortgage. The Federal Housing Finance Agency (FHFA) says that calculating the number of Americans who are having difficulty paying for their homes may be difficult considering new rules and regulations related to the pandemic response.

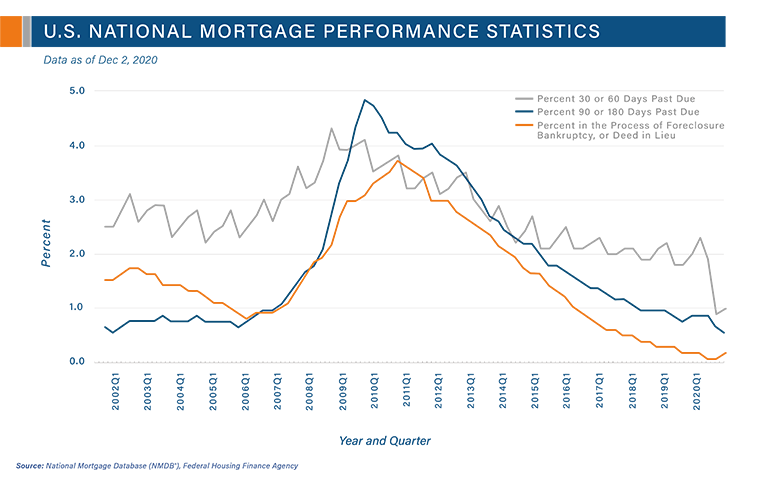

During 2020, mortgages reported to the credit bureaus as delinquent plunged to 1.0% (as shown in the figure below). The percentages over the past year for mortgages that were seriously delinquent and mortgages in the process of foreclosure, bankruptcy, or deed-in-lieu remained flat," according to an FHFA press release. "As a result of these trends, the median credit score of mortgage borrowers, as measured by VantageScore on borrowers of active mortgage loans, has actually risen slightly in 2020."

Based on that information, it would appear that most borrowers aren’t having any trouble keeping up with their mortgages. However, the CARES Act (short for Corona Virus Aid, Relief, and Economic Security Act) allowed people to skip payments without damaging their credit scores or having their mortgages flagged as past due on their credit reports.

Data presented in the figure below, drawn from the National Mortgage Database (NMDB) sponsored by FHFA and CFPB, show the national impact of these components of the CARES Act. The data shown are based on what the past-due status of mortgages reported to the credit bureaus would be if a credit report were pulled for every borrower on the last day of the month.

Their mortgage status would remain at whatever it was when the CARES Act passed. Therefore, if they were current on their payments, but then missed one after the act passed, no harm would come to their credit and their actual status would be difficult to determine.

So, when looking at mortgage performance statistics, it’s important to keep all of this in mind.

In 2020, mortgages reported 30 to 60 days late fell to 1.0%. Mortgages that were 90 to180 days past due fell to 0.6%. And mortgages that resulted in foreclosure, bankruptcy, or deed-in-lieu remained flat at 0.3%.

Overall median credit scores for mortgage borrowers rose slightly in 2020, according to VantageScore.

If the provisions in the CARES Act were removed, it’s likely that by the end of October 2020, past-due mortgages would be three percentage points higher. However, a more accurate assessment of how the pandemic impacted mortgages most likely won’t be available until after the crisis ends.