DSNews The homepage of the servicing industry

DSNews The homepage of the servicing industry

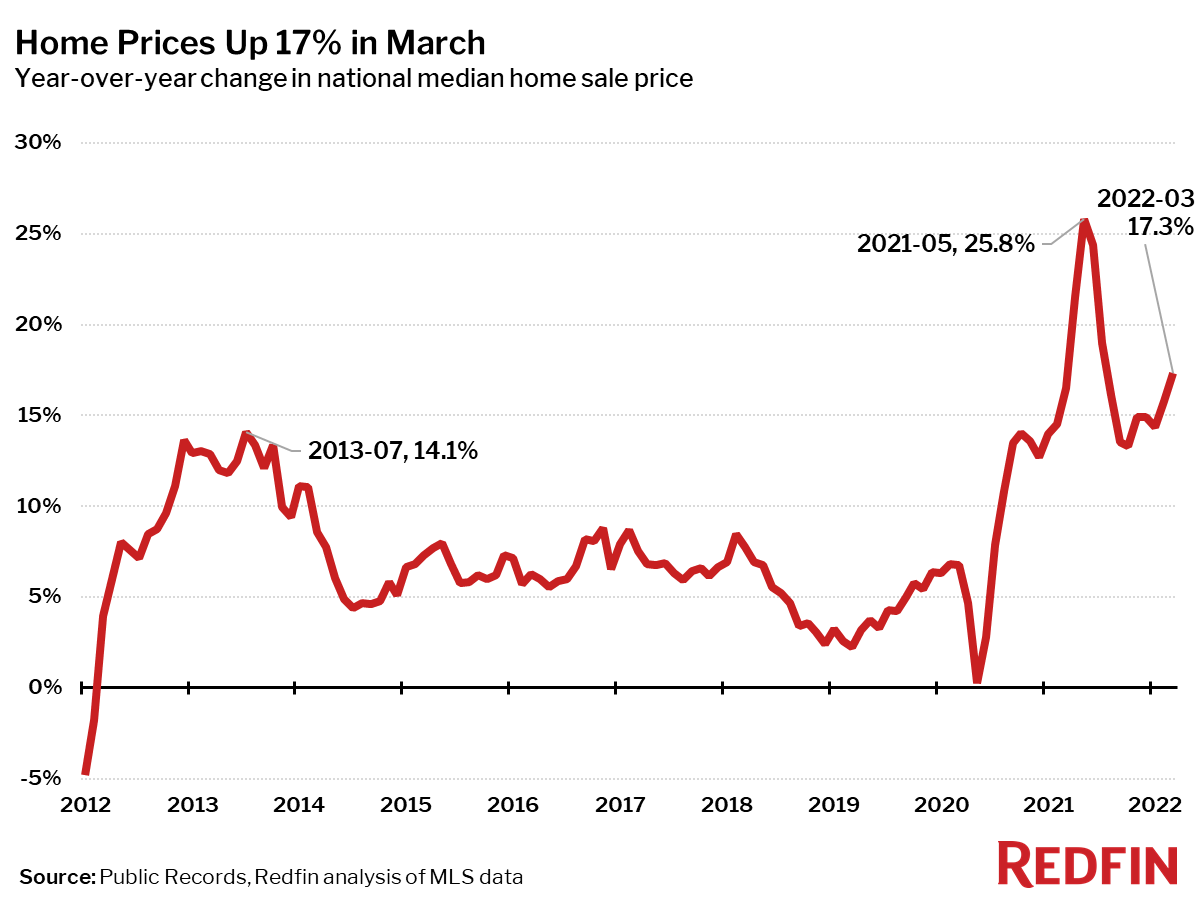

According to a new report from Redfin, it was the hottest March ever recorded for the housing market, with homes selling at their fastest pace and for more above list price than any other March on record. The median home-sale price rose 6.2% in March, the fastest month-over-month gain at this time of year since 2013, to an all-time high of $412,700.

Seasonally adjusted home sales fell 4% as soaring mortgage rates, and prices sidelined more buyers, whose options were severely limited due to a decline in homes being listed.

“Although pricey coastal markets began showing early signs of a slowdown in late March, nationwide sales data for the full month reflects the hottest March market on record, since homes that sold last month mostly went under contract in February,” said Redfin Chief Economist Daryl Fairweather. “We expect the combination of surging mortgage rates and record-high home prices to cause more homebuyers to drop out of the market. Unfortunately, homeowners are turning their back on the market too. Instead of being motivated to list before prices weaken, potential home sellers may be choosing to wait-out the impending market cooldown.”

Median sale prices increased from 2021 in all of the 88 largest metro areas, with the largest price increases in Tampa, Phoenix, and McAllen, Texas.

Seasonally-adjusted home sales in March were down 4% from a month earlier and down 8% from a year earlier. Home sales fell from the prior year in 79 of the 88 largest metro areas Redfin tracks. The biggest sales declines were in North Port, Florida, down -30%, West Palm Beach, Florida, down -24%, and Lake County, Illinois, down -21%. The largest gains were in Fresno, California, up +6%, Philadelphia, up +6%, and Oxnard, California, up +3%.

Seasonally adjusted active listings—the count of all homes that were for sale at any time during the month—fell 13% year over year to an all-time low in March.

82 of the 88 largest metros tracked by Redfin posted year-over-year decreases in the number of seasonally adjusted active listings of homes for sale. The biggest year-over-year declines in active housing supply in March were in Allentown, Pennsylvania, down -47%, Greensboro, North Carolina, down -41%, and Fort Lauderdale, Florida, down -37%. The only metro areas where the number of homes for sale increased were Elgin, Illinois, Chicago, Illinois, Detroit, Michigan, and Lake County, Illinois.

New listings fell from a year ago in 69 of the 88 largest metro areas. The largest declines were in Allentown, Pennsylvania, down -56%, Greensboro, North Carolina, down -39%, and Honolulu, down -25%. New listings rose the most in McAllen, Texas, up +17%, Rochester, New York, up +7%, and Detroit, Michigan, which rose +7%.

Home sales that closed in March spent less time on the market and sold for further above list price than a year ago. The typical home that sold in March went under contract in 20 days—six days faster than a year earlier--and the shortest time on market ever for March.

Approximately 54% of homes sold above list price, up 12 percentage points from a year earlier, and the highest March level on record. The average sale-to-list price ratio in March was 102.4%, up from 100.6% a year earlier, another record-high for this time of year.

To read the full report, including charts and additional metro-level highlights, click here.