DSNews The homepage of the servicing industry

DSNews The homepage of the servicing industry

Editor's note: This piece originally appeared in the October issue of DS News.

Editor's note: This piece originally appeared in the October issue of DS News.

Lessons learned from past recessions tell us that neighborhood blight can lower surrounding property values and create havens for crime and illegal activity. Abandoned homes can also threaten the public health and safety of our communities. Never has this been more concerning than at the present time. We are living in an unprecedented era in which schools are shut down across America, unemployment rates are expected to reach 20-25%, and the very strategy that can help Americans stay in their home could unintentionally harm neighborhoods.

While coronavirus kept most Americans at home during “Stay at Home” orders, many cities experienced temporary reductions in property related crimes. New York City, as the “hardest hit” municipality, was not so lucky. NYC experienced a 31.6% increase in burglaries in April, up +28.9% YTD.

With June 2020’s unemployment rate of 11.1%, already higher than it has been since 1940, “property-related” crimes are expected to increase. Many economists expect unemployment rates to continue to rise.

Why Is This Concerning?

For the first time in U.S. history, the government has mandated that banks and servicers provide up to 12 months of mortgage forbearance, with the only requirement being that the borrower must state that they have a COVID-19 hardship. While typically these programs are not available for investment properties and second homes, the CARES Act states that these borrowers also qualify. Per the Mortgage Bankers Association (MBA), as of August 4, 2020, forbearances accounted for 7.67% of mortgages, with over 3.8M homeowners now in active forbearance plans.

It is estimated that 35% are investment properties and almost 6% are second homes. The U.S. had a 6.7% nationwide vacancy rate in 2019 (including rental and homeowner vacancy rates). Given these difficult economic times, the U.S. could quickly see 6.4M properties (incudes single-family to four-plex, and mobile homes from U.S. Census data), that could be vacant and abandoned during the next 12 months. Unemployed investors may not have the available capital to cover turn-over expenses. Tenant qualifying ratios will be hard to meet, with some economists predicting that 1:4 or 1:5 Americans in the workforce could become unemployed as a result of COVID-19.

The Federal Housing Finance Agency, which provides oversight for Fannie Mae and Freddie Mac, announced new inspection requirements regarding CARES Act forbearances. They issued directives to banks and servicers stating that monthly occupancy inspections should no longer be done on any property under forbearance that is not already known to be vacant. They will also not reimburse for inspections. With banks and servicers already having liquidity challenges, they do not have the extra financial resources to absorb these much-needed inspections.

The anticipated abandoned and blighted properties will be left to neighborhoods to deal with. It will put added burdens on communities to take care of issues themselves. With governments already feeling the economic hardships of COVID-19, they will not have the additional resources needed to keep these properties safe, sound, secure, and sanitary.

Additionally, the risk of failing to provide routine occupancy inspection oversight could be dire and will negatively impact the iInvestor’s portfolios. For instance, many forced place hazard insurance policies may not pay out for theft, vandalism, and sur-chargeable damage, if vacancies are not properly identified quickly. Property values will likely depreciate. Property-related crime is expected to increase, and includes heating, ventilation, and air conditioning (HVAC) and copper wiring and plumbing theft, appliances and fixture theft, as well as vandalism. These unmonitored assets also create a higher risk for health and safety concerns, such as unsecured swimming pools, that could result in loss of life. Unnoticed roof damage and exposure to the elements can cause major water damage, including mold, which can cost tens of thousands of dollars to remediate. Investors may also have to deal with increased code violations and daily penalty fees for failure to promptly rectify.

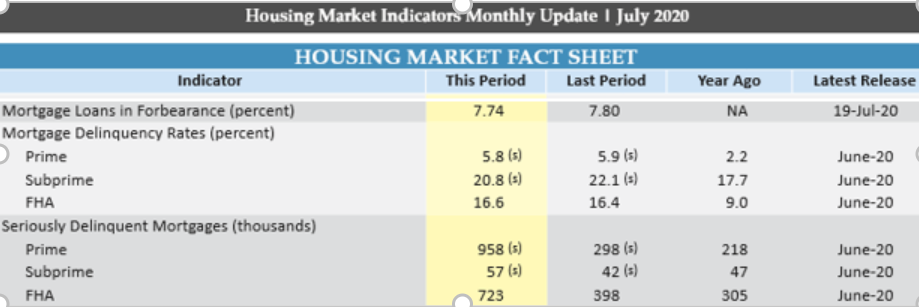

HUD’s July 2020 Housing Indicator Report shows:

To ensure properties are not abandoned and at risk to cause community blight, all investors, including the Federal Housing Administration (FHA), who has 41.6% of all seriously delinquent mortgages, the investors should seriously consider putting strategies together to include a “risk-based” inspection cadence for high-risk assets. Without these precautions, all of us will have to live with the consequences, and the communities most in need, will pay the highest cost.