DSNews The homepage of the servicing industry

DSNews The homepage of the servicing industry

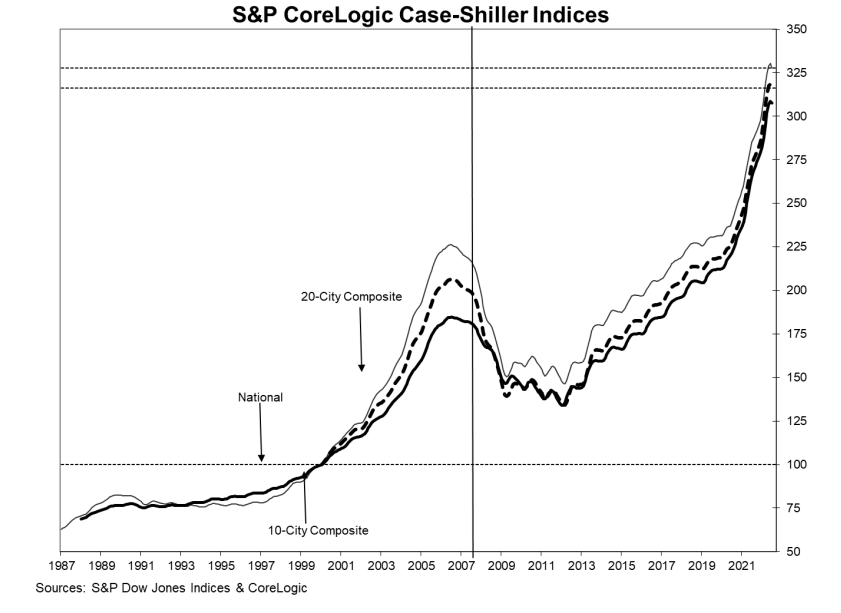

An analysis of data from the July 2022 S&P CoreLogic Case-Shiller Indices has concluded that home price gains decelerated across the United States in July. The S&P CoreLogic Case-Shiller U.S. National Home Price NSA Index—which reports on all nine U.S. Census Divisions, reported a 15.8% annual gain in July—down from 18.1% reported in June 2022.

An analysis of data from the July 2022 S&P CoreLogic Case-Shiller Indices has concluded that home price gains decelerated across the United States in July. The S&P CoreLogic Case-Shiller U.S. National Home Price NSA Index—which reports on all nine U.S. Census Divisions, reported a 15.8% annual gain in July—down from 18.1% reported in June 2022.

The 10-City Composite annual increase came in at 14.9%, down from 17.4% in the previous month. The 20-City Composite posted a 16.1% year-over-year gain, down from 18.7% in the previous month.

The Tampa, Miami, and Dallas areas reported the highest year-over-year gains among the 20 cities in July, with Tampa leading the way with a 31.8% year-over-year price increase, followed by Miami with a 31.7% increase, and Dallas with a 24.7% increase. All 20 cities reported lower price increases in the year ending July 2022 compared to the year ending June 2022.

“Although U.S. housing prices remain substantially above their year-ago levels, July’s report reflects a forceful deceleration,” said Craig J. Lazzara, Managing Director at S&P DJI. “For example, while the National Composite Index rose by 15.8% in the 12 months ended July 2022, its year-over-year price rise in June was 18.1%. The -2.3% difference between those two monthly rates of gain is the largest deceleration in the history of the Index. We saw similar patterns in our 10-City Composite (up 14.9% in July vs. 17.4% in June) and our 20-City Composite (up 16.1% in July vs. 18.7% in June). On a month-over-month basis, all three composites declined in July.”

And that “forceful deceleration” as described by Lazzara came in the form of continuous rate hikes by the Federal Reserve, four of which were handed down over the past five months alone. The Fed’s efforts to control inflation began May 5, 2022, with a 50-point rise in the Fed Funds Rate from 0.75% to 1.00%. Two more increases of 75 points each on June 16 and July 27 preceded last week’s hike yet again of 75 points, raising the Fed Funds Rate to its current reading of 3.25%. The intent of the rate hikes is to bring balance to an unbalanced housing marketplace.

“Housing market participants have reached an impasse, and surging mortgage rates are the culprit,” said CoreLogic Deputy Chief Economist Selma Hepp. “Many buyers moved to the sidelines as the cost of home ownership became prohibitively high, while sellers were unwilling to give up locked-in record low rates and expectations of peak sales price. As a result, home price growth continues to decelerate from April’s 20% peak and is anticipated to reach half of April’s rate by December. Home price deceleration and seasonal price decline in some markets will provide opportunities for potential buyers who are now facing lessened competition than earlier this year.”

Before seasonal adjustment, S&P CoreLogic’s U.S. National Index posted a -0.3% month-over-month decrease in July 2022, while the 10-City and 20-City Composites both posted decreases of -0.8%. After seasonal adjustment, the U.S. National Index posted a month-over-month decrease of -0.2%, and the 10-City and 20-City Composites posted decreases of -0.5% and -0.4%, respectively. In July, only seven cities reported increases before and after seasonal adjustments.

Despite these moves by the Fed, affordability challenges remain for a market plagued by rising prices across the board.

“The median sales price of new houses sold in August 2022 was $436,800, which is up 8% compared with one year ago, but a decline of 6.3% compared with July,” said First American Deputy Chief Economist Odeta Kushi. “While still above the pre-pandemic average annual pace of appreciation, this is the slowest year-over-year price growth since November 2020.”

Affordability may allude many for the foreseeable future, as ahead of the Fed’s latest rate hike last week, Freddie Mac reported the 30-year-fixed-rate mortgage hitting a 14-year high of 6.29%.

“Mortgage rates are now within striking distance of the 7% threshold, pushing a home purchase further out of many Americans’ reach, especially first-time homebuyers,” said George Ratiu, Senior Economist & Manager of Economic Research for Realtor.com. “Not surprisingly, deals are not getting done, with sales of new and existing homes declining for over half a year. Given that demand is cooling due to high borrowing costs, incomes falling behind inflation and the still-limited supply pipeline, it is becoming increasingly clear that prices have to decline to restore market liquidity and balance.”

Kushi added, “The housing market is cooling, but it remains a struggle for potential first-time home buyers. One year ago, 25% of new-home sales were priced below $300,000. In August 2022, only 12% of new-home sales were priced below $300,000. That’s dramatic change from the pre-pandemic level in August 2019 of 43%.”