DSNews The homepage of the servicing industry

DSNews The homepage of the servicing industry

People were not just fighting to get gifts this holiday season, they were also eager to get into homes entering the market in droves. But those that entered the market were not just fighting astonishingly low inventory levels, but record high prices as well.

People were not just fighting to get gifts this holiday season, they were also eager to get into homes entering the market in droves. But those that entered the market were not just fighting astonishingly low inventory levels, but record high prices as well.

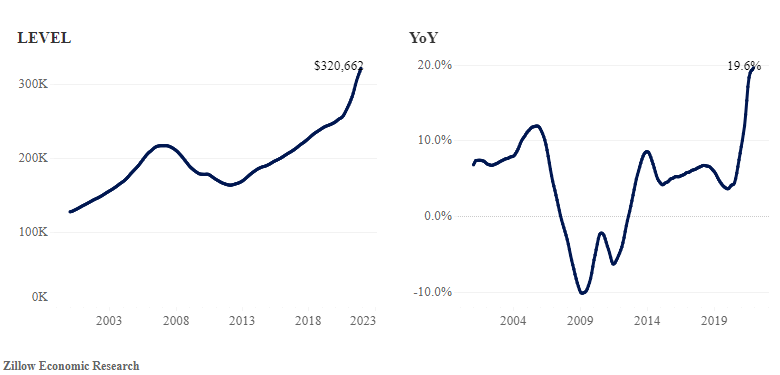

According to Zillow's December Home Market Report, home values grew a record 1.6% month-over-month in December, and that appreciation accelerated throughout much of the U.S. The typical American home is worth $320,662, up 19.6% from a year ago—a new high according to Zillow.

According to a recent survey by Zillow, homeowners have been hesitant to list their houses due to them not wanting to wade into the market themselves, on top of employment uncertainties caused by the new Omicron COVID-19 variant.

"Home shoppers picked the shelves clean this December, leaving fewer active listings than ever before in the U.S. housing market," said Jeff Tucker, Senior Economist at Zillow. "Enough determined buyers kept up their house hunt to reignite monthly price appreciation. Rising mortgage rates could be the next potential headwind, but demand has proven persistent; neither high prices nor slim inventories have deterred buyers so far."

The big takeaway from the December report is just how low inventory has sunk to. It was found that inventory levels in December dropped by 11.1% to 923,000 units, an all time low recorded by Zillow. This number represents a 19.5% reduction from levels seen at the end of 2020 and a 40.5% drop from pre-pandemic times at the end of 2019.

“Inventory’s stalled-out rebound is even more striking in light of the near-complete expiration of mortgage forbearance, which some (Zillow included) speculated may trigger a wave of forced listings this autumn,” Tucker wrote in the report. “It is still possible that some distressed homeowners will list their homes for sale later this year if they are unable to reach repayment agreements with their lenders.”

“But so far, it appears the forbearance program was largely successful in achieving its goal of keeping people in their homes and avoiding the wave of foreclosures and distressed sales that characterized the 2008-2012 era housing market,” Tucker continued. “To whatever extent that homeowners exited forbearance by selling their homes, contributing to Q3’s modest inventory rebound, those listings seem to have been digested already by eager homebuyers.”

Locally, inventory was down across the board among all major metropolitan areas; the largest annual inventory declines in December among the largest 50 markets were in Miami (-48.0%), Denver (-40.3%), and Raleigh (-39.2%). However, inventory was up year-over-year in Austin (+14.6%).

On another note, the speed at which homes are selling has steadily trended up over the past few months and now sits at 13 days, up from the 11 days seen in November. While that is still a blistering pace, it is higher than the seven days seen in June of this year giving buyers more time to assess their options.

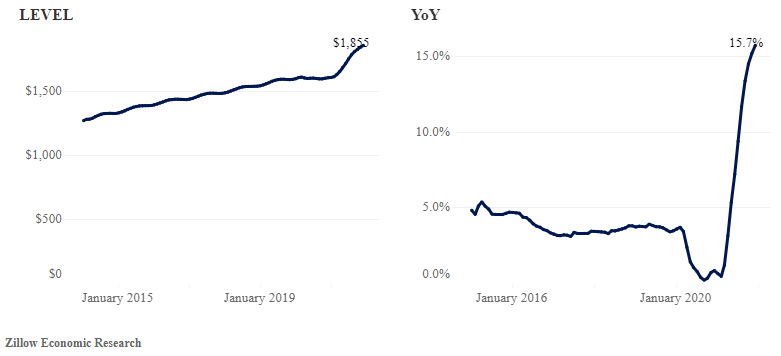

In terms of rent, the Zillow Observed Rent Index rose a record 15.7% year-over-year in December, to $1,855 a month, representing a 0.7% increase from November. Annual rent appreciation was fastest across the Sunbelt, led by Miami (29.6%), Tampa (28.6%), Phoenix (26.0%), and Las Vegas (25.1%).

“The rapid growth in rents is now being picked up, after a delay earlier this year, in official measures of inflation,” Tucker concluded. “The main Consumer Price Index component measuring rents, the Rent of Primary Residence, rose 3.3% year-over-year in December, or almost 0.5% month-over-month. Combined with rising Owners’ Equivalent Rent, which was also up 0.4% in December, the rising shelter components of the CPI are contributing to overall inflation—now registering its fastest growth in almost 40 years.”

Looking ahead, Zillow expects inventory to remain low, pushing existing home sales to highs not seen since 2005. Further, they expect home prices to increase by 4.1% in the first quarter of 2022 and reach 16.4% by the end of the year which represents an estimated 6.6 million existing home sales in 2022, up 7% from 2021.