DSNews The homepage of the servicing industry

DSNews The homepage of the servicing industry

As the nation closes in on a full calendar year of lockdowns, quarantines, remote working and other “new norms” courtesy of COVID-19, the pandemic’s stranglehold on the housing market continues its ripple effect nationwide.

As the nation closes in on a full calendar year of lockdowns, quarantines, remote working and other “new norms” courtesy of COVID-19, the pandemic’s stranglehold on the housing market continues its ripple effect nationwide.

March 11, 2020 is the day the World Health Organization (WHO) declared COVID-19 a pandemic, and since that date, record-low mortgage rates and remote work situations are driving scores of Americans to buy bigger homes in more affordable places, but those same factors are fueling fierce bidding wars, skyrocketing prices and an intensifying housing shortage.

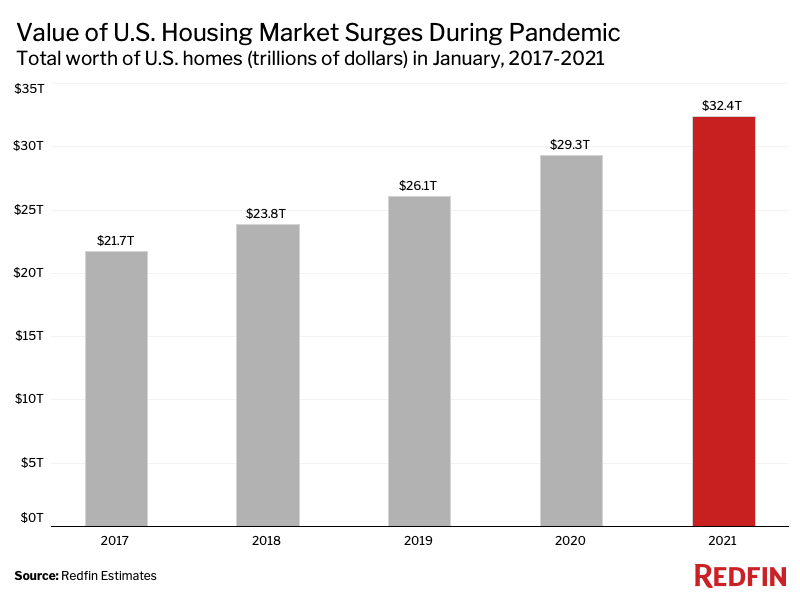

According to Redfin, U.S. homeowners have reaped $3.1 trillion in home value during the pandemic as a result of rising housing prices. The total worth of U.S. homes was $32.4 trillion in January, up 10% from $29.3 trillion a year earlier. The median home sale price was $330,500 in January, up 14.3% from a year earlier, the biggest annual jump during a given month since at least 2013.

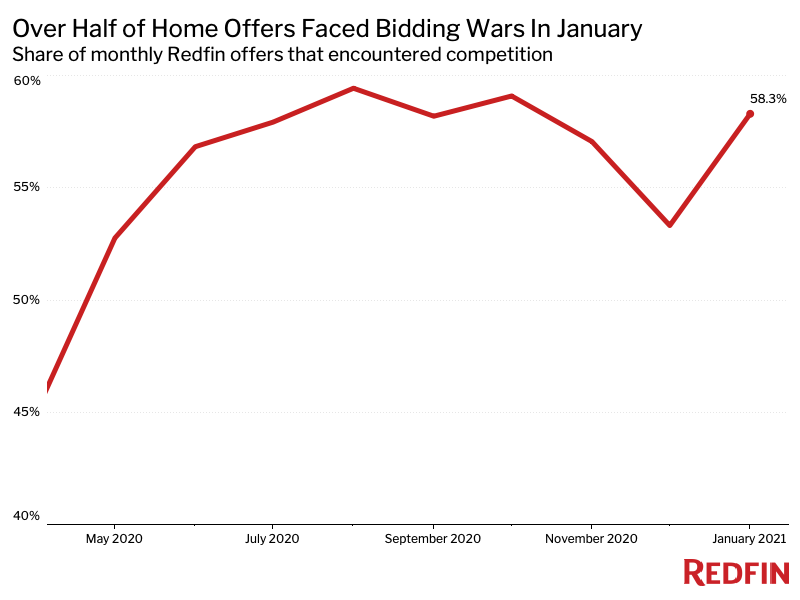

Bidding wars have heated up as well, as the glut of buyers in the market have far outweighed the short supply of homes available. The supply of homes for sale plummeted a record 23.6% year-over-year in January, as scores of Americans relocated and purchased homes. The inventory shortage has acted as a catalyst for many of the other housing-market shifts seen over the past year, including skyrocketing prices and fierce bidding wars.

“Inventory is so low that it has even been tough to get in to see homes at all,” said Danielle Parent, a Redfin real estate agent in Cleveland, Ohio. “It’s a very, very challenging market for buyers, so I’m telling my clients that they should always have second- and third-choice homes in mind and may want to consider making offers sight-unseen.”

Redfin recently reported that, for 400-plus metro areas during the four-week period ending February 21, 2021, a record 43% of homes for sale spent just a week or less on the market. The typical home that sold in January went under contract in 34 days—22 days fewer than a year earlier—and a third (32.9%) of homes sold for above their listing prices, compared with 18.9% a year earlier.

“One four-bedroom home in Ontario, Calif. just sold for $165,000 above its $445,000 listing price. A lot of my clients just don’t have enough money to go that high, or even $25,000 over asking,” said local Redfin agent Sheri Comeau. “Most of the folks I work with are first-time buyers who barely have enough to put 5% down. I’m seeing many clients pull from their retirement savings to supplement their downpayments, which helps boost their buying power.”

Click here for more information on Redfin’s latest data.