DSNews The homepage of the servicing industry

DSNews The homepage of the servicing industry

By writing policy that prioritizes Americans' access to homeownership, lawmakers could address both the affordable home shortage and the racial wealth gap, deduces Urban Institute visiting fellow Mike Loftin. He bases his assessment—that such access will foster financial stability and mobility for millions of Americans—on data collected by Urban Institute and Zillow researchers.

By writing policy that prioritizes Americans' access to homeownership, lawmakers could address both the affordable home shortage and the racial wealth gap, deduces Urban Institute visiting fellow Mike Loftin. He bases his assessment—that such access will foster financial stability and mobility for millions of Americans—on data collected by Urban Institute and Zillow researchers.

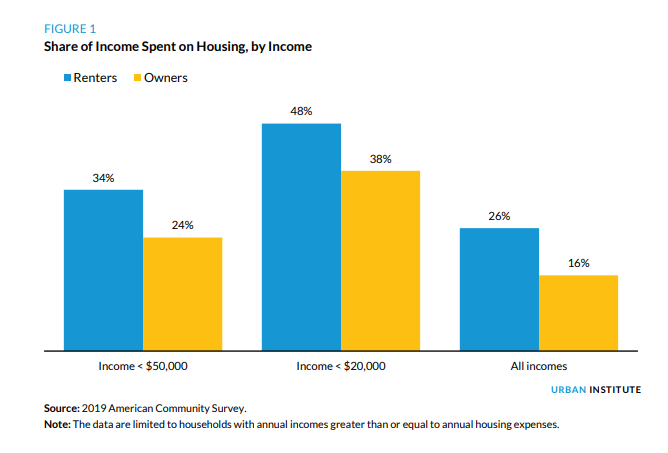

"Some believe homeownership is reserved for people who achieve some level of financial success, that it’s not for people still on the path to financial security. This may explain why most federal, state, and local efforts to create more affordable housing narrowly focus on the rental market," he noted. "However, the data disprove this thinking. The typical homeowner spends 10 percentage points less of their income on housing than the typical renter."

Loftin points out that there is no shortage of policy proposals to address the housing problem—some think the federal government should invest in building more public housing. Others suggest increasing subsidies to builders of affordable apartments, and many recommend dramatically increasing the availability of rent vouchers that pay landlords a portion of the rent so that tenants can pay less. He says that while we clearly need affordable rental housing, the aforementioned tactics do not take into account the country's biggest source of affordable housing, which is homeownership.

Loftin argues that this holds true when controlling for income as well as for race and ethnicity.

In households with $50,000 annual income or less, renters spend about 34% of their intake on housing. Owners spend about 24%, according to Urban Institute's study. In households earning less than $20,000 a year, homeowners spend 38% to renters' 48% on house payments.

Though Black and Latinx homeowners have steeper home payment expense ratios than white homeowners, they have lower housing expense ratios than all renters, including white renters. The median housing expense ratio for Black and Hispanic homeowners is 19%, and the average white renter household spends 24% of its income on housing.

Data shows the average monthly rent payment is higher than a mortgage payment: Zillow Home Value Index estimated the median home value at $263,351. Assuming a 30-year fixed-rate mortgage at a 3.5% interest rate, the monthly mortgage payment would be $1,464. For the same period, the Zillow Observed Rent Index found the median monthly rent was $1,734, meaning the average renter paid $270 more per month than the average homebuyer.

In addition to being more affordable, in general, mortgage payments, unlike rent, do not rise. The only potential changes in homeowners’ housing expenses are taxes and insurance.

The income to payment ratio also has a better long-term outlook for homeowners, according to Loftin. Annual increases in housing costs will almost always grow faster for renters than for homeowners, according to Urban Institute's assessment.

Loftin takes into account the argument that the homeowner is responsible for maintenance, unlike renters. According to the American Housing Survey, he says, the typical homeowner spends about $167 per month on maintenance and home improvements. He says that still puts the owners of a median-priced home paying $93 less per year than someone renting the same house.

Homeownership is partly an investment as opposed to 100% consumer spending (like rent).

"The homeowner’s real housing expenses decline over time because the principal portion of the mortgage payment is not really an expense," Loftin explains. "Instead, it builds the homeowner’s equity."

And the biggest payoff comes in the long-term. After a homeowner makes their final mortgage payment, housing expense drops precipitously, often just in time for retirement, when incomes tend to decline. It is what Loftin refers to as "homeownership's affordability big bang."

Thus, Loftin says, lawmakers aiming to effectively address America's affordable housing crunch, as well as its racial wealth gap, would do well to focus on increasing accessibility of homeownership.

"Affordable homeownership is not the capstone of economic well-being," he said, "it is the cornerstone."

The full report on rent versus owning is available at Urban.org.