DSNews The homepage of the servicing industry

DSNews The homepage of the servicing industry

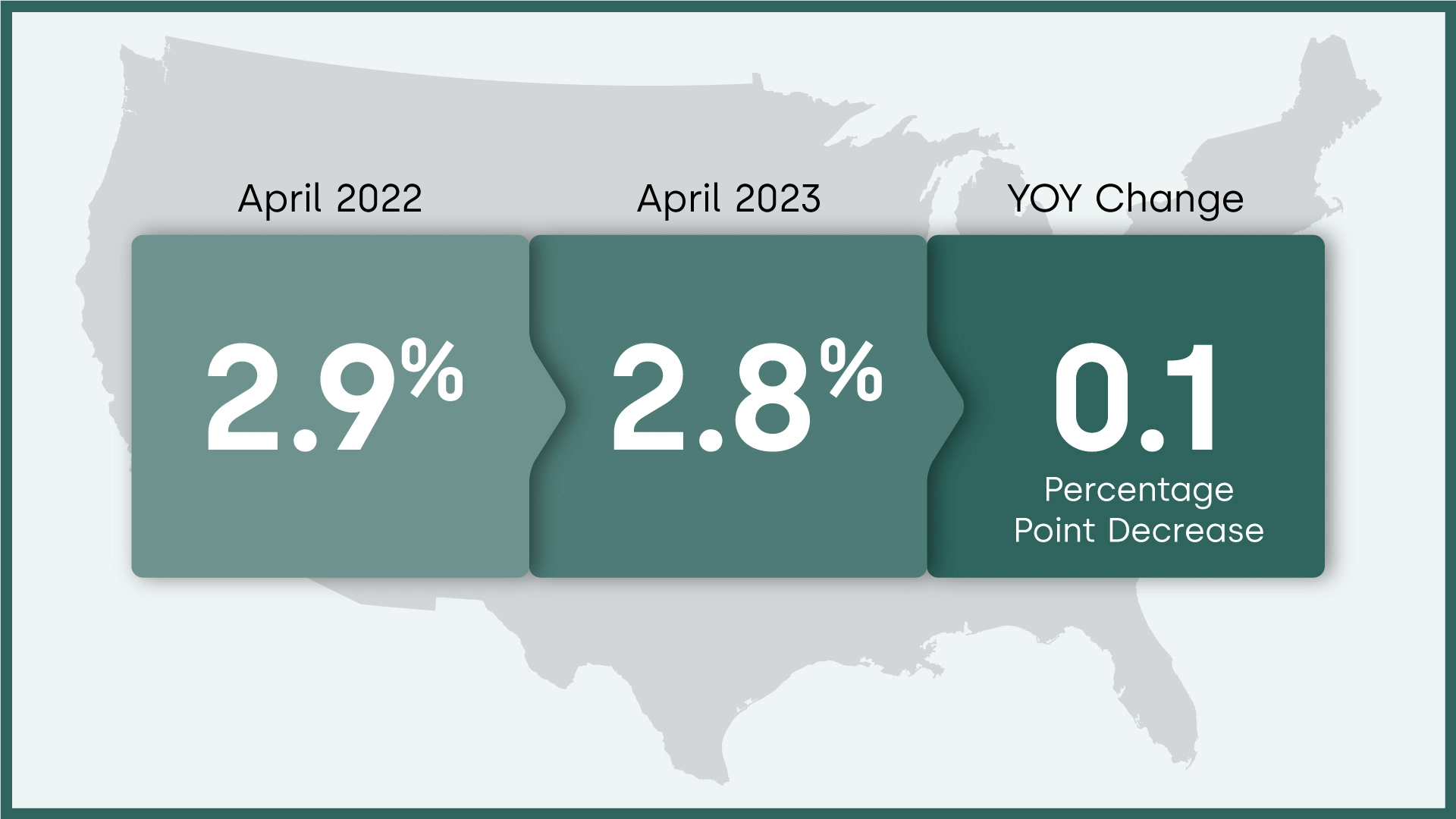

The Loan Performance Insights Report covering April 2023 and published by CoreLogic found that for the month of April, 2.8% of all mortgages in the U.S. were in some form of delinquency (at least 30 days past due, including those with foreclosure filings against them) representing a 0.1% percentage point decrease year-over-year when compared to April 2022, but a 0.2 percentage point increase from the 2.6% in March 2023.

The Loan Performance Insights Report covering April 2023 and published by CoreLogic found that for the month of April, 2.8% of all mortgages in the U.S. were in some form of delinquency (at least 30 days past due, including those with foreclosure filings against them) representing a 0.1% percentage point decrease year-over-year when compared to April 2022, but a 0.2 percentage point increase from the 2.6% in March 2023.

To gain a complete view of the mortgage market and loan performance health, CoreLogic examines all stages of delinquency. In April 2023, the U.S. delinquency and transition rates and their year-over-year changes, were as follows:

- Early-Stage Delinquencies (30 to 59 days past due): 1.4%, up from 1.2% in April 2022

- Adverse Delinquency (60 to 89 days past due): 0.4%, up from 0.3% in April 2022.

- Serious Delinquency (90 days or more past due, including loans in foreclosure): 1.1%, down from 1.4% in April 2022 and a high of 4.3% in August 2020.

- Foreclosure Inventory Rate (the share of mortgages in some stage of the foreclosure process): 0.3%, unchanged from April 2022.

- Transition Rate (the share of mortgages that transitioned from current to 30 days past due): 0.8%, up from 0.7% April 2022.

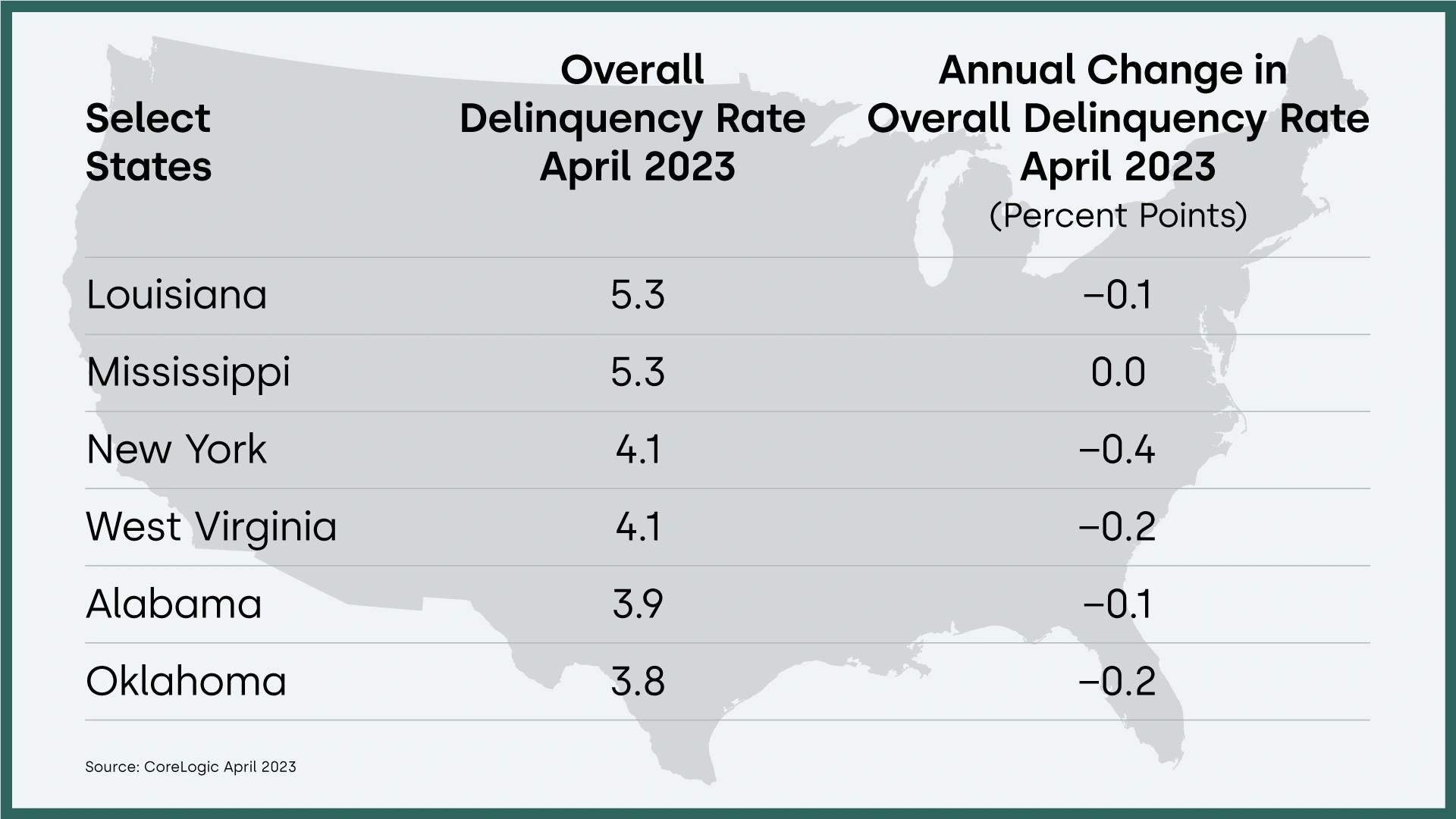

Though nearly a dozen states and 150 metropolitan areas posted year-over-year increases in overall delinquency rates, loan performance overall remains resilient as delinquencies and foreclosures continue to hover near record lows.

CoreLogic notes that delinquency and foreclosure numbers are seasonal, as tax bills can strech homeowners’ budgets in the short term and result in late mortgage payments for some borrowers.

“Mortgage performance remained strong in April, with overall delinquencies at minimal levels and serious delinquencies at a 23-year low,” said Molly Boesel, Principal Economist for CoreLogic. “However, there is concern that mortgages originated in a rising-interest-rate environment may have higher instances of delinquencies, as borrowers become stretched financially. While early delinquencies for 2022 mortgage originations are about the same rate as those in other rising interest-rate environments, loans with low down payments are exhibiting comparably higher-than-usual early delinquencies.”

State and Metro Takeaways:

- Eleven states posted an annual increase in overall delinquency rates in April. The states with the largest increases were Idaho, Indiana, Michigan and Utah (all up by 0.2 percentage points). An additional 11 states saw no change in overall delinquency rates year over year. The remaining states' annual delinquency rates dropped between 0.7 and 0.1 percentage points.

- In April, 161 U.S. metro areas posted an increase in overall year-over-year delinquency rates. Cape Coral-Fort Myers, Florida (up by 1.2 percentage points) led, followed by Punta Gorda, Florida (up by 1 percentage points) and Bloomsburg-Berwick, Pennsylvania (up by 0.8 percentage points).

- Four U.S. metro areas posted an increase in serious delinquency rates (defined as 90 days or more late on a mortgage payment) in April, while five showed no change. The metros that saw serious delinquencies increase were Cape Coral-Fort Myers, Florida (up by 0.9 percentage points); Punta Gorda, Florida (up by 0.8 percentage points); and Elkhart-Goshen Indiana and Idaho Falls, Idaho (both up by 0.1 percentage points).