DSNews The homepage of the servicing industry

DSNews The homepage of the servicing industry

Factors including supply chain issues and climate change could mean a 9% rise in homeowners insurance rates in 2023, to an average $1,784 per year, data analysts predict in a new study by the research team at Insurify.

Factors including supply chain issues and climate change could mean a 9% rise in homeowners insurance rates in 2023, to an average $1,784 per year, data analysts predict in a new study by the research team at Insurify.

In 2022, home insurance rose approximately 7%, to $1,636 per annum, from the previous year, according to analysts who based estimates on Insurify’s collected property data.

“U.S. auto and homeowner insurance premium rates lagged behind the inflation rate in 2020 and 2021, laying the groundwork for the premium increases which occurred last year and will continue into 2023,” Mark Friedlander, Director of Corporate Communications at Insurance Information Institute, said, referring to Insurify’s study Insuring the American Homeowner.

The study revealed homeowners in Florida, Oklahoma, and Louisiana pay the most for homeowners insurance—Florida’s average premium is $7,788 a year, making it the country’s most expensive. That’s compared to $6,853 in Oklahoma, $5,353 in Louisiana. Nebraska rounds out the top 10 priciest states at $4,064 per annum.

At a hyperlocal level, unsurprisingly, beachfront property owners pay the highest premiums. Those in Hallandale Beach, Florida pay a whopping $12,578 annually, followed by three other Floridian metros—Hialeah, Miami, and Lake Worth — where annual premiums average $12,319, $11,258, and $10,741, respectively.

Nine of the 10 most expensive cities for homeowner insurance are located in just three states—Florida, Louisiana and Oklahoma—all of which are historically at high risk of severe weather events such as hurricanes and tornadoes. Alabama’s Orange Beach ranks 5th most expensive at $9,264.

Costs in America’s 10 priciest cities and states for insurance are detailed in the study at insurify.com.

Multiple factors contribute to this rise in premiums, inflation, climate, material costs, supply chain issues, and increased claims for fire and water damage, to name a few, experts say. Homeowner credit score, ZIP code, and the coverage level needed also affect the cost.

Colleen Finn, Managing Director at Boston-based insurer Plymouth Rock, said that those inflationary pressures that are driving up Americans’ grocery bills are now driving up homeowner insurance rates. “It is costing more and taking longer to repair your home, increasing the average cost per claim and ultimately the cost of homeowners insurance for everyone,” Finn said.

Experts add that severe weather and natural disasters, such as floods, earthquakes, hurricanes, and wildfires are also inflating coverage costs.

The Federal Emergency Management Agency (FEMA) assigns a risk rating denoting the probability and severity of natural disasters across the United States. Homeowners in “very high risk” areas pay almost 2.5 times more for home insurance than those living in areas of “very low risk,” according to Insurify’s analysis.

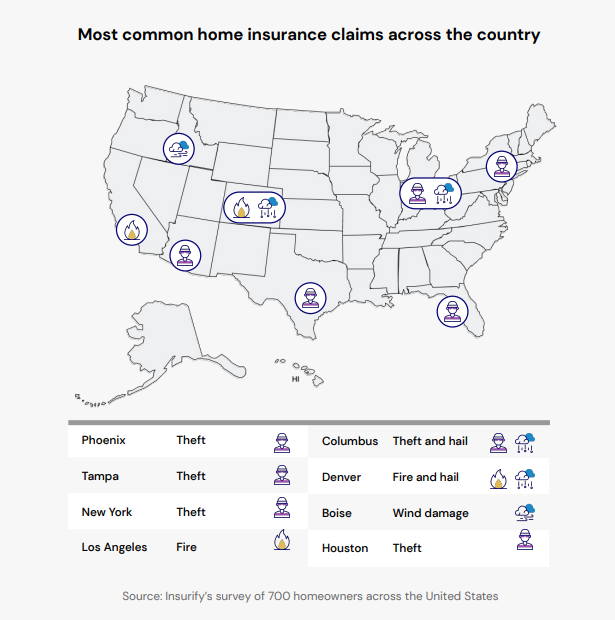

Nearly half (45%) of homeowners already believe climate change has affected their homes’ values, according to Insurify’s survey of 700 homeowners in key housing markets.

And 76% reported a mild to high level of concern that climate change could eventually affect their homes’ values.

Agents at Insury suggest homeowners install secure rooftop HVAC systems, reinforce the roof of their houses, and install hurricane shutters, to name a few; insurers may offer reduced rates to homeowners who take these risk-reduction measures, they report.

For a more detailed look at the future of homeowners insurance costs and how borrowers are reducing premiums, see Insuring the American Homeowner at insurify.com.