DSNews The homepage of the servicing industry

DSNews The homepage of the servicing industry

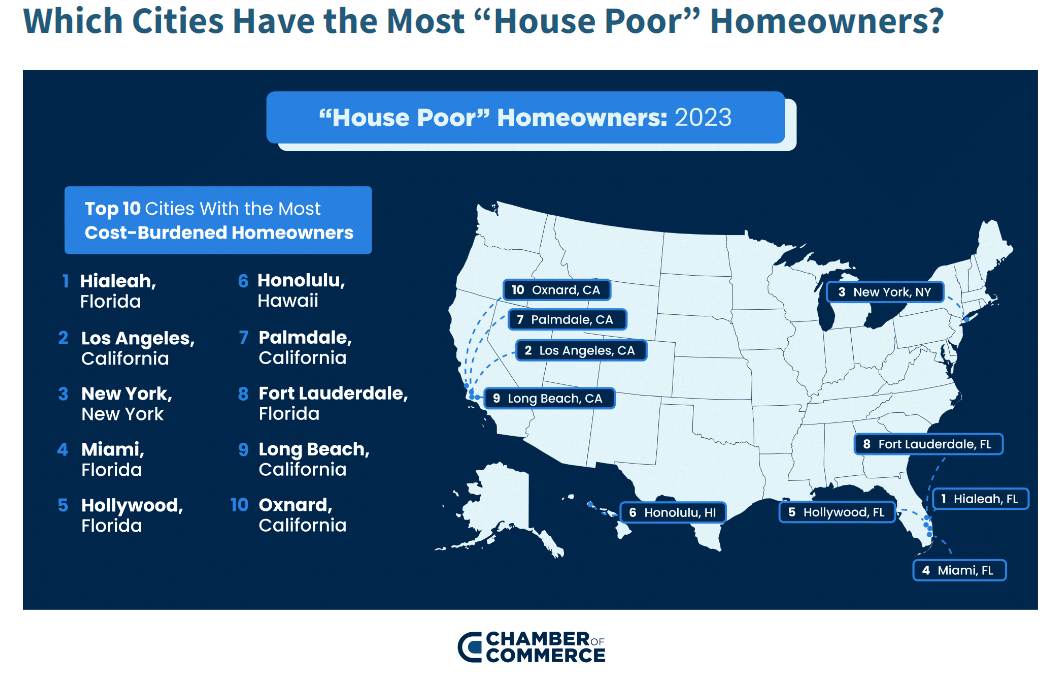

Through an analysis of U.S. Census Bureau data, researchers have ranked the nation’s most “house poor” cities where many homeowners find themselves stuck in homes they cannot afford. Homeowners who are spending more than 30% of their income on housing costs are considered “house poor.”

Through an analysis of U.S. Census Bureau data, researchers have ranked the nation’s most “house poor” cities where many homeowners find themselves stuck in homes they cannot afford. Homeowners who are spending more than 30% of their income on housing costs are considered “house poor.”

According to the study, these cost-burdened homeowners have found themselves facing budget-busting housing expenses, including monthly mortgage payments, property taxes, homeowners insurance, and utilities.

Nationwide, 27.4% of homeowners were considered “house poor” according to the researchers, with Miami, Los Angeles, and New York City ranking as the top three cities with the most homeowners living beyond their means. More than four in 10 homeowners are considered to be “house poor” in these cities. Cities located in Florida and California dominated the list of top 30 cities. Overall, six cities within the top 30 were found in Florida, and 14 were located in California.

Nearly three in 10 (27.4%) of U.S. homeowners with a mortgage are considered to be cost-burdened with housing expenses, according to the Census Bureau. Overall, 21% of cost-burdened homeowners have a household income of less than $75,000.

Top Five U.S. Cities With the Most House Poor Homeowners

#1. Hialeah, Florida

- Percentage of House Poor Homeowners: 59.3%

- Number of House Poor Households: 10,918

- Median Household Income: $64,386

- Median Monthly Household Costs: $1,632

- Median Yearly Household Costs: $19,584

#2. Los Angeles

- Percentage of House Poor Homeowners: 48.7%

- Number of House Poor Households: 179,821

- Median Household Income: $122,032

- Median Monthly Household Costs: $2,972

- Median Yearly Household Costs: $35,664

#3. New York City, New York

- Percentage of House Poor Homeowners: 45.3%

- Number of House Poor Households: 272,355

- Median Household Income: $120,618

- Median Monthly Household Costs: $2,848

- Median Yearly Household Costs: $34,176

#4. Miami, Florida

- Percentage of House Poor Homeowners: 44.6%

- Number of House Poor Households: 14,565

- Median Household Income: $92,897

- Median Monthly Household Costs: $2,308

- Median Yearly Household Costs: $27,696

#5. Hollywood, Florida

- Percentage of House Poor Homeowners: 44.3%

- Number of House Poor Households: 10,180

- Median Household Income: $98,131

- Median Monthly Household Costs: $2,039

- Median Yearly Household Costs: $24,468

To determine the ranking, researchers analyzed median household income and median monthly housing costs across more than nine million households located in the most populated 170 census-defined places via the U.S. Census Bureau’s American Community Survey. Cities were ranked based on the percentage of homeowners who spend more than 30% of their household income on monthly housing costs. The Census Bureau defines monthly housing costs as the sum of payments for mortgages, deeds of trust, contracts to purchase, or similar debts on the property (including payments for the first mortgage, second mortgages, home equity loans, and other junior mortgages); real estate taxes; fire, hazard, and flood insurance on the property; utilities (electricity, gas, and water and sewer); and fuels (oil, coal, kerosene, wood, etc.).