DSNews The homepage of the servicing industry

DSNews The homepage of the servicing industry

According to a new report from the CoreLogic Property Data Science Team , properties with higher wildfire risks sell for less and appreciate at a slower rate than those that are not in wildfire prone areas.

According to a new report from the CoreLogic Property Data Science Team , properties with higher wildfire risks sell for less and appreciate at a slower rate than those that are not in wildfire prone areas.

It’s no secret that California’s wildfire propensity has increased in severity over the past decade, somewhat in part due to global warming with the year 2020 standing out particularly badly. These fires have a clear connection to property values according to CoreLogic, and found that properties located in close proximity to wildfire perimeters experienced significantly lower appreciation than those located farther away.

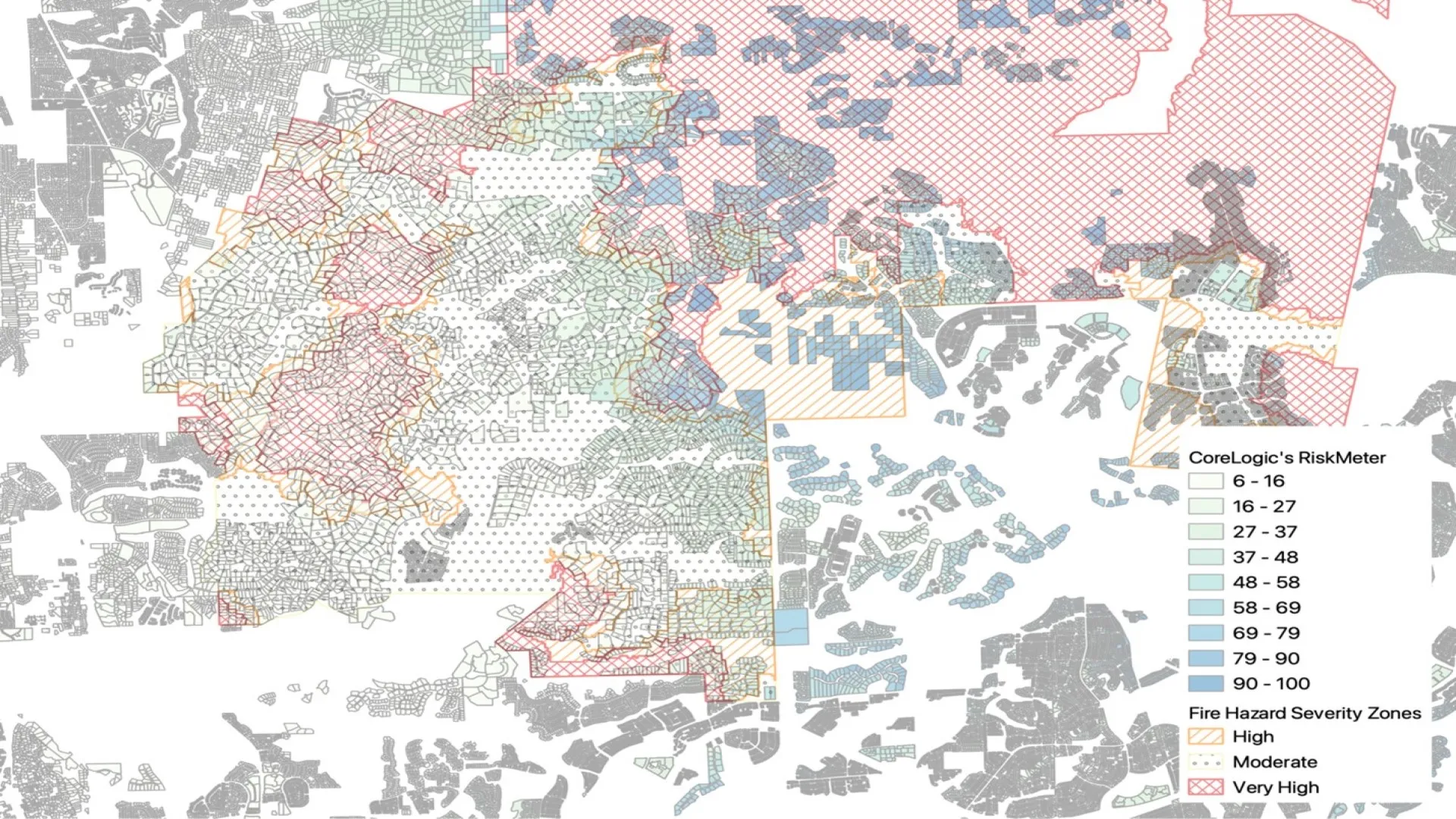

The California State Fire Marshal classifies lands into three Fire Hazard Severity Zones (FHSZs): Moderate, High and Very High. While the increased cost of constructing wildfire-resistant homes in California has led developers to build more homes in Moderate FHSZs, it is important to recognize that properties outside the High and Very High areas still face risks of wildfire damage.

In CoreLogic’s latest study, they examined the impact of wildfire risks on property values in San Diego County, since it is one of the states most vulnerable counties to fire. The property data used in this analysis includes all transactions since 2011 in San Diego County and is from the CoreLogic property database, which encompasses addresses, sales prices, property attributes and geospatial information.

According to CoreLogic, using a hedonic regression model, we calculated price per square foot on CoreLogic’s Wildfire Risk Score to examine the effect of wildfire risks on property values (while controlling for other factors).

CoreLogic’s Wildfire Risk Score provides a property-level hazard risk assessment that accounts for various factors, such as risk rating, proximity to higher-risk areas, slope, vegetation and other variables. The Wildfire Risk Score uses a precise and graduated evaluation, differentiating between incremental levels of risk for properties within and outside of FHSZs. Properties with higher risk scores are more likely to experience wildfires.

The figure below illustrates the overlay of the Wildfire Risk Score in San Diego County, showing high-risk areas outside the FHSZ or within the Moderate FHSZ, as well as varying risk levels within the FHSZ areas.

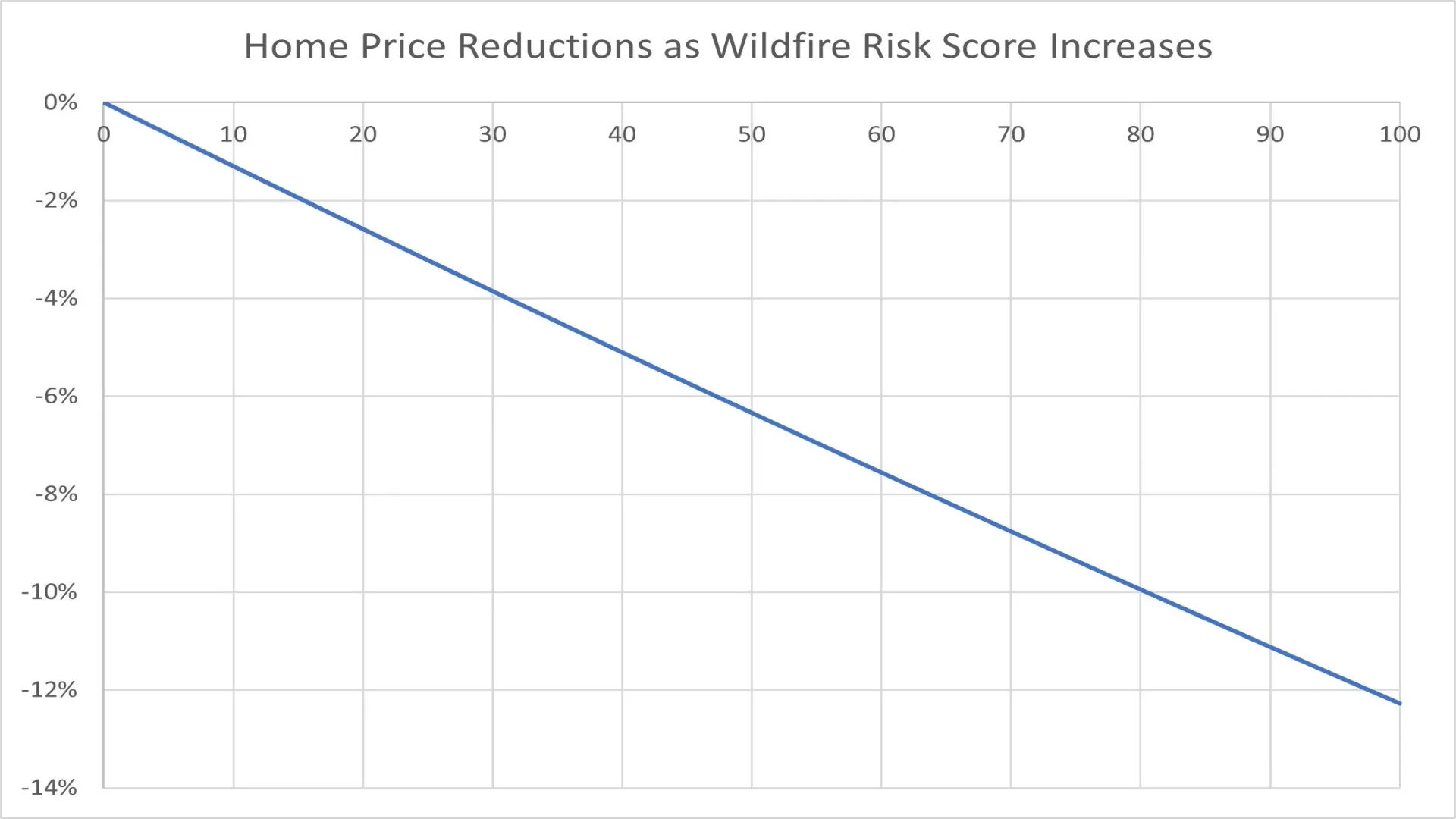

The next figure shows the impact of wildfire risks on home prices in San Diego County. For every 10-point increase on the Wildfire Risk Score, home prices decreased by approximately 1.3%. In May 2023, the median sales price for a home in San Diego County was $910,000. If a similar home’s wildfire risk score increased from 40 to 60 due to climate change issues, it would be projected to sell for $886,000. Mortgage lenders and originators often overlook this negative impact of climate change risks on property values.

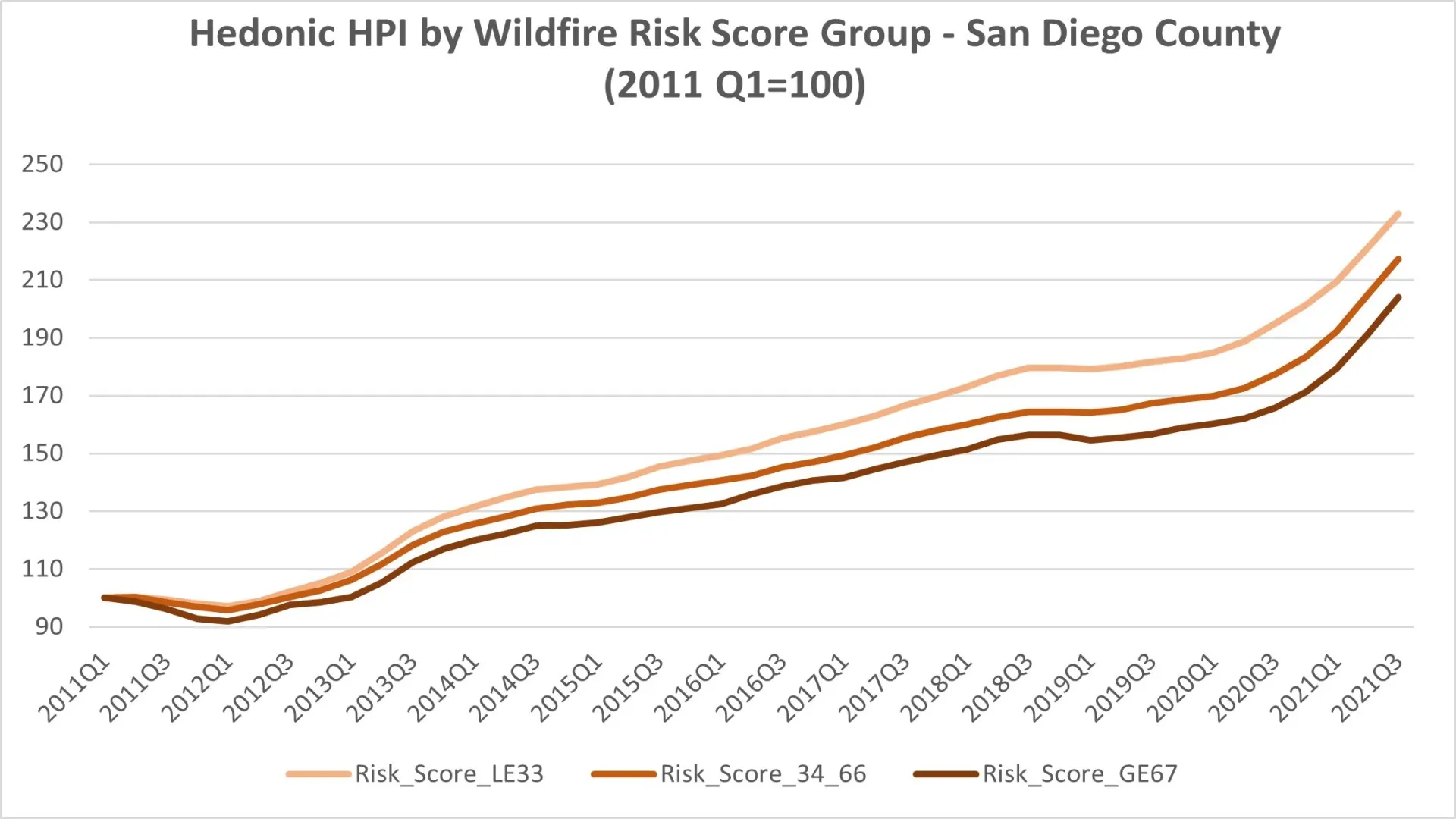

As a result of the hedonic regression analysis, CoreLogic has developed home price indexes that measure property appreciation over time, while controlling for housing stock quality differences. After grouping the wildfire risk scores into three categories — High, Moderate and Low — we conducted separate regressions for each category to compare how prices might have appreciated under different risk levels due to wildfires in San Diego.

The final figure illustrates the home price indexes for the three aforementioned wildfire risk zones, indicating that higher risk corresponds to lower appreciation. Since 2011, homes with low wildfire risks have appreciated by more than 230%, while those with high wildfire risks have appreciated roughly 200%.

The analysis clearly demonstrates that properties with higher wildfire risks in San Diego sell for less and appreciate at a slower rate than similar properties with lower wildfire risks, assuming all other factors are equal.

Understanding the role of collateral value in loan origination and portfolio management makes it critical for homeowners, mortgage lenders, insurers and policymakers to consider the impact of climate risk on property values. Adopting a proactive approach to this challenge and its effect on the property market is essential to foster a healthy housing ecosystem.