DSNews The homepage of the servicing industry

DSNews The homepage of the servicing industry

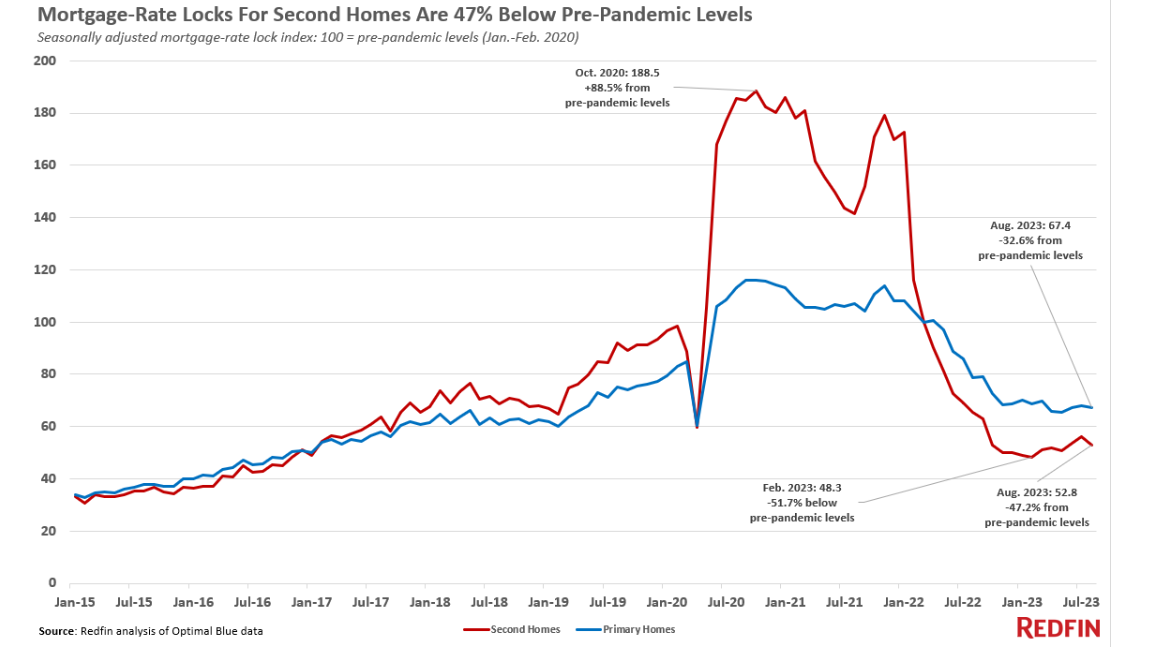

Redfin reports that mortgage-rate locks for second homes and investment properties were down 47% from pre-pandemic levels on a seasonally adjusted basis in August, compared to a 33% decline for primary homes.

Redfin reports that mortgage-rate locks for second homes and investment properties were down 47% from pre-pandemic levels on a seasonally adjusted basis in August, compared to a 33% decline for primary homes.

August marked the 14th consecutive month that second-home demand has hovered at least 30% below pre-pandemic levels, as high housing costs and limited inventory deter would-be buyers. Rate locks for second homes hit a seven-year low in February, dropping to 52% below pre-pandemic levels.

A mortgage-rate lock is an agreement between a homebuyer and a lender that allows the homebuyer to lock in an interest rate on a mortgage for a certain period of time; roughly 80% of rate locks result in purchases.

Demand for second homes is also down year-over-year as mortgage-rate locks for second homes is down 19% year-over-year, bigger than the 14% decline for primary homes.

The decline in mortgage locks for vacation homes comes after a boom during the pandemic, hitting a peak of 88.5% above pre-pandemic levels in October of 2020. Many jumped at the chance to snap up second homes with record-low mortgage rates during a time when many could work remotely from vacation towns at a time of record low mortgage rates. Demand for primary homes jumped during that time, too, but the increase was much more modest, reaching a peak of 16% above pre-pandemic levels in late 2020.

Mortgage rates rose to a two-decade high in August exceeding the 7% mark and keeping demand for both primary homes and second homes at bay. Still-high home prices, the elevated cost of other goods and services, an unsteady economy, and a lack of new listings are also holding back buyers of both home types.

However, the dip in demand for vacation homes and investment properties is due to a number of factors:

- It’s more expensive to buy a second home: The typical home in a seasonal town—where many second homes are located—sells for $564,000, up 5% from a year earlier. That’s compared with $421,000 for homes in non-seasonal towns, also up 5%. Mortgage rates for second homes are also typically higher. Finally, the federal government increased loan fees for second homes in 2022, often adding tens of thousands of dollars to the cost of purchasing a home.

- Many workers are returning to the office: The allure of second homes has diminished as many companies call workers back to the office, at least part of the time.

- Short-term rentals are less attractive: Buying a vacation home to rent it out on a short-term rental site like Airbnb may be less attractive than it once was. Local governments including New York City are instituting new short-term rental regulations, like new taxes and strict permitting, that cut into profits and make the business more difficult.

- The long-term rental market is cooling: Buying a vacation home to rent it out long term is less attractive, too. The rental market has cooled from its pandemic peak; although asking rents are still high, many landlords are being forced to offer concessions to attract renters. Plus, there’s a rising number of vacancies for landlords to fill, with many new units set to hit the market soon.

- Demand for second homes is up slightly from the bottom it hit in the beginning of the year: That’s likely because home prices have come down in some second-home hotspots, including Austin, Texas; and Phoenix, and some affluent Americans are investing in vacation homes before prices rise. Interest in second homes first fell below pre-pandemic levels in April 2022, the month the loan-fee increase took effect and several months after mortgage rates started jumping.