DSNews The homepage of the servicing industry

DSNews The homepage of the servicing industry

A new analysis from Redfin has found that nearly 7% of homes for-sale posted a price drop during the four weeks ending October 29, on average, the highest portion on record.

A new analysis from Redfin has found that nearly 7% of homes for-sale posted a price drop during the four weeks ending October 29, on average, the highest portion on record.

The record comes as mortgage rates hover at elevated levels, according to Freddie Mac, hitting their highest level in 23 years last week and cutting deep into buyers’ budgets. High rates have forced some sellers to lower their asking price to make up for high interest rates on monthly payments.

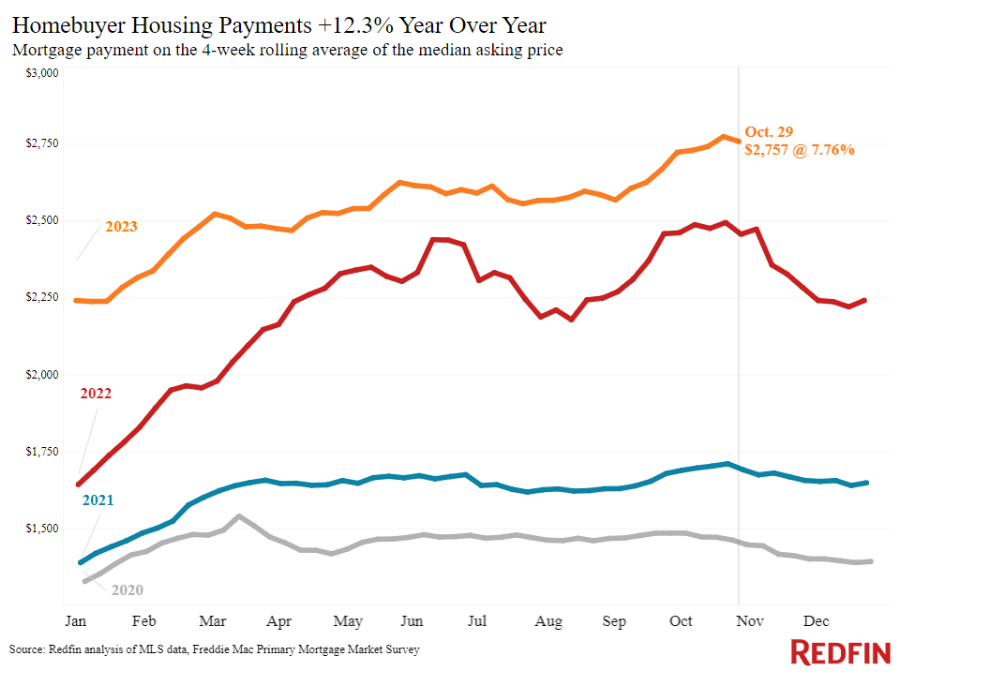

Redfin reports that prospective buyers are getting a bit of temporary relief this week, as economic events sent daily average mortgage rates downward to 7.76% as of November 2, 2023, led by the Federal Reserve’s second consecutive pause in increasing the nominal interest rate.

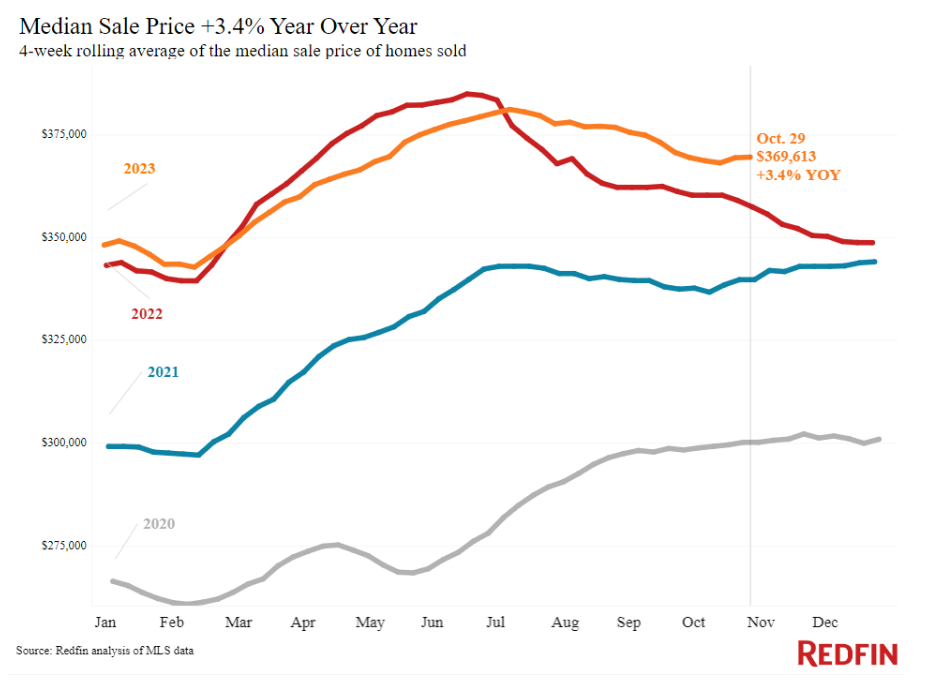

Despite the slight dip in rates, home sale prices are still up 3% year-over-year, partly due to sale-price data as a lagging indicator, reflecting deals that went under contract a month or two ago. Growth in sale prices may slow in the coming months as it starts to reflect sales that went under contract as mortgage rates hit 8% in October.

“Some sellers are pricing too high because they have FOMO after their neighbor’s house sold well over asking price two years ago,” said Seattle Redfin Premier Agent Patrick Beringer. “While low inventory is driving some competition and relatively affordable homes in popular neighborhoods are still selling fast, they’re getting two or three offers as opposed to 20 offers at the height of the market. With mortgage rates in the 7.5% to 8% range, buyers simply don’t have the budget they would have had two years ago or even one year ago.”

Redfin cites that another reason for the rise in sale prices is that despite slow demand, low inventory continues to prop up prices. The total number of homes nationwide for sale is down 10% year-over-year, with new listings up 1% from just one year ago—just the second increase since July 2022.

In the Seattle metro, for instance, the typical homebuyer’s monthly mortgage payment is $232 more than it would have been a year ago. It’s nearly $2,000 more than it would have been two years ago.

The Mortgage Bankers Association (MBA) reported that homebuyer affordability improved slightly in the month of September, with the national median payment applied for by purchase applicants decreasing $15 monthly from $2,170 in August 2023 to $2,155 in September. Year-over-year, the national median payment applied was up $214 from one year ago, an 11% year-over-year increase.

Key highlights reported by Redfin for the four weeks ending October 29, 2023, include:

- The median U.S. home sale price averaged $369,613, up 3.4%year-over-year, as prices were up partly due to elevated mortgage rates hampering prices during this time last year.

- The median U.S. asking price was $383,200, up 5.4% year-over-year, marking the biggest increase in a year.

- The median monthly mortgage payment averaged $2,757 at a 7.76% mortgage rate, up 12% year-over-year, which was $16 shy of the all-time high set a week earlier.

- Pending sales nationwide stood at 68,693, down 8.8% week-over-week.

- New listings averaged 79,906 nationwide, up just 1.1% year-over-year, marking the second year-over-year increase since July 2022. The increase is partly due to new listings falling at this time last year.

- Active listings stood at 858,570, down 10.2% year-over-year, marking the smallest decline since July 2023.

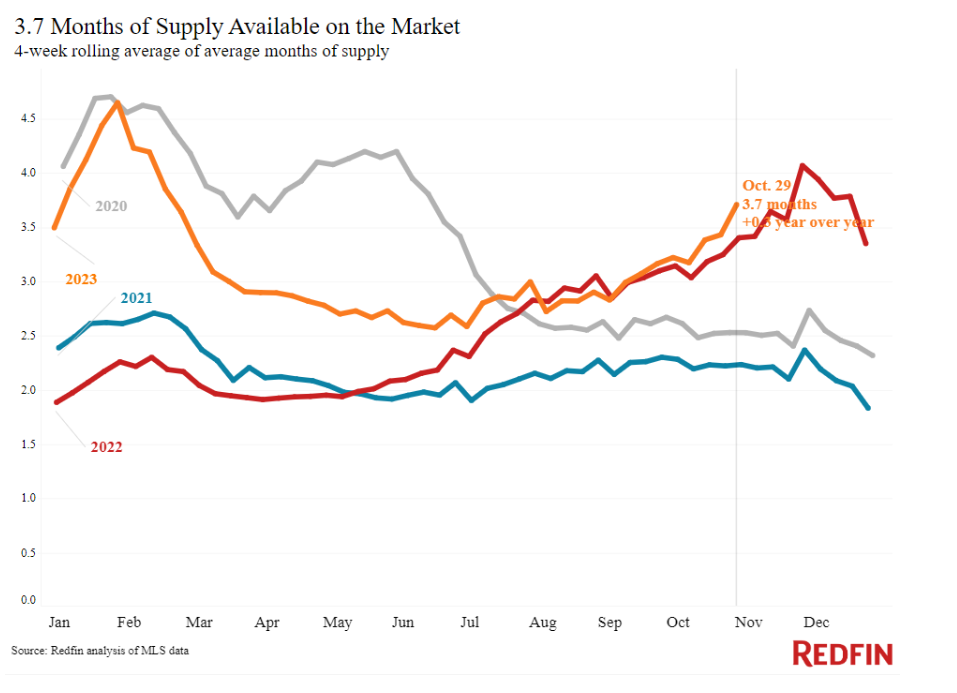

- The months of the nation’s home supply stood at 3.7 months, up 0.3 points, marking the highest level reported since February 2023. A four to five months of supply is considered balanced, with a lower number indicating seller’s market conditions.

- The median days homes spent on the market was 33 days, down two days year-over-year.

Click here for more findings from Redfin’s latest analysis of U.S. housing data.