DSNews The homepage of the servicing industry

DSNews The homepage of the servicing industry

“Turbulent” is an apt word to describe the current state of the housing market—from record-breaking inflation, to continually rising interest rates, high home prices, and mortgage rates above 7% for the first time in over 20 years, those in still in the market to purchase a home are fighting an uphill battle.

While the state of the market has made purchasing a home more difficult, military servicemembers—both past and present—face additional challenges such as frequent relocations due to changing orders.

But according to House Method’s most recent servicemember survey, respondents remained relatively optimistic about their chances of buying a house.

Overall, 68% of respondents reported it was a “very good” or “somewhat good” time to purchase a home, while 46% said their ability to purchase a home is better than it was last year. Looking deeper, 21 said this was due to a better credit score, 19% said it was do to increased savings, 17% said it was additional income, and a final 17% indicated that there were more affordable homes in their price range.

64% of the 550 service members surveyed reported that they are renting, but have been actively looking to purchase a home over the last 12 months. 71% indicated they would prefer to own versus rent a home.

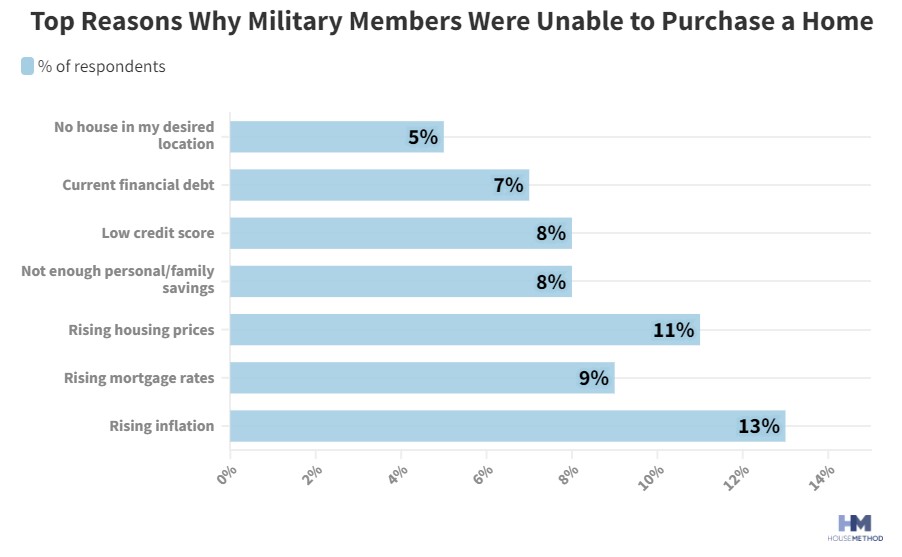

Respondents indicated the most common reasons for not purchasing a home are rising inflation, low credit scores, and rising housing prices.

“Optimism continues to grow for prospective buyers looking to purchase in 2023. Twenty-one percent think it will be a somewhat bad time to buy, with only 6% thinking it will be very bad,” House Method wrote in their findings. “These figures are the lowest of the three years, showing few believe home prices will become more severe next year. Interestingly, 37% said it would be a somewhat good time to buy, which is the lowest of all three years. However, 36% said it would be a very good time to buy a home, 7% more than in 2022 and 22% more than in 2021.”

Barriers to homeownership for servicemembers includes: no houses available in their area (5%), debt (7%), low credit score (8%), no savings (8%), rising housing prices (11%), rising mortgage rates (9%), and inflation (13%).

“When it comes to buying a home, one of the benefits available to all service members is the Basic Allowance for Housing (BAH),” House Method said. “BAH are funds the U.S. military provides to its service members to offset the cost of housing. It only applies to service members who choose not to live in government-provided housing. BAH rates are determined by regional housing costs, pay grade, and dependency status. The nice thing about BAH rates is that they reflect the areas in which service members are deployed, meaning they’ll go up in high-cost areas. However, while BAH can offset housing costs greatly, it does not provide enough funds to cover everything.”

Finally, looking ahead, just under 40% of respondents believe that 2023 will be an excellent year to buy a home.

Click here to see House Method’s findings in their entirety.