DSNews The homepage of the servicing industry

DSNews The homepage of the servicing industry

Independent mortgage banks (IMBs) and mortgage subsidiaries of chartered banks reported a pre-tax net loss of $1,015 on each loan they originated in Q3 2023, an increase from the reported loss of $534 per loan in Q2 of 2023, according to the Mortgage Bankers Association’s (MBA) Quarterly Mortgage Bankers Performance Report.

Independent mortgage banks (IMBs) and mortgage subsidiaries of chartered banks reported a pre-tax net loss of $1,015 on each loan they originated in Q3 2023, an increase from the reported loss of $534 per loan in Q2 of 2023, according to the Mortgage Bankers Association’s (MBA) Quarterly Mortgage Bankers Performance Report.

“A decline in originations volume worsened net production losses in the third quarter of 2023,” said Marina B. Walsh, CMB, MBA’s VP of Industry Analysis. “While production revenues stayed relatively flat, per-loan production costs reverted to the third-highest level in the history of MBA’s survey, which reversed a portion of the cost improvements made in the second quarter.”

Major takeaways from the MBA’s Q3 2023 Quarterly Mortgage Bankers Performance Report include:

- Including all business lines (both production and servicing), 51% of the firms in the study posted pre-tax net financial profits in Q3, down from 58% in Q2.

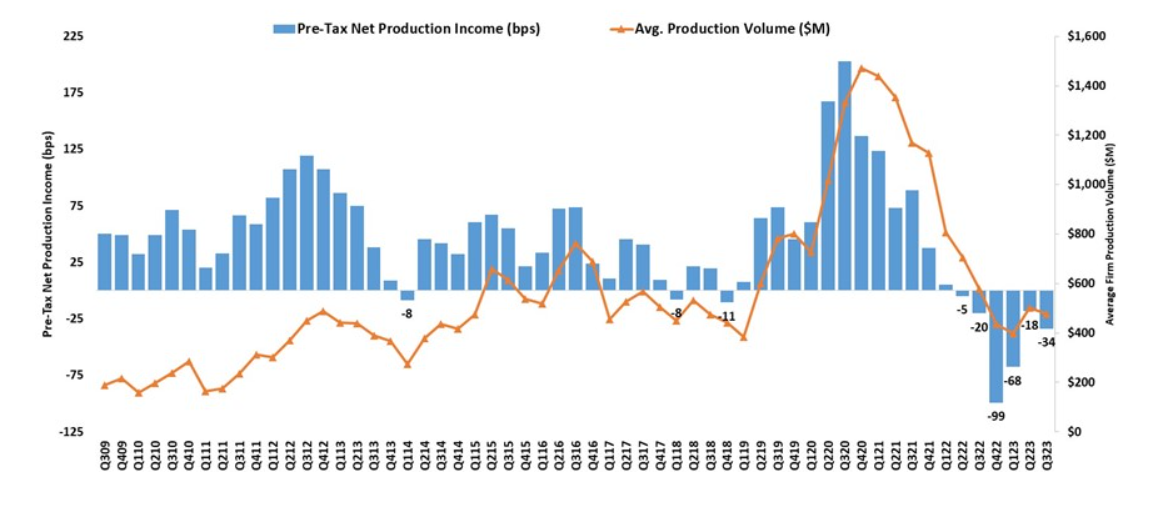

- The average pre-tax production loss was 34 basis points (bps) in Q3 of 2023, compared to an average net production loss of 18 bps in Q2 of 2023, and a loss of 20 basis points one year ago. The average quarterly pre-tax production profit, from Q3 of 2008 to the most recent quarter, is 45 basis points.

- The average production volume was $477 million per company in Q3, down from $502 million per company in Q2. The volume by count per company averaged 1,497 loans in Q3, down from 1,553 loans in the second quarter.

- Total production revenue (fee income, net secondary marketing income and warehouse spread) increased to 329 bps in Q3, up slightly from 328 bps in Q2. On a per-loan basis, production revenues decreased to $10,426 per loan in Q3, down from $10,510 per loan in Q2.

- The purchase share of total originations, by dollar volume, was constant at 89%. For the mortgage industry as a whole, MBA estimates the purchase share was at 82% in Q3 of 2023.

- The average loan balance for first mortgages decreased to $341,708 in Q3, down from $343,386 in Q2.

- Total loan production expenses–commissions, compensation, occupancy, equipment, and other production expenses and corporate allocations–increased to $11,441 per loan in Q3, up from $11,044 per loan in the second quarter of 2023. From Q3 of 2008 to the last quarter, loan production expenses have averaged $7,305 per loan.

- Servicing net financial income for Q3 (without annualizing) was $90 per loan, down from $94 per loan in Q2. Servicing operating income, which excludes MSR amortization, gains/loss in the valuation of servicing rights net of hedging gains/losses, and gains/losses on the bulk sale of MSRs, was $104 per loan in Q3, down from $105 per loan in Q2.

“Net production income has been in the red for six consecutive quarters,” added Walsh. “MBA forecasts lower industry volume over the next two quarters compared to last quarter, which means a turnaround is unlikely until the second quarter of 2024. One silver lining is that mortgage servicing continues to be a bright spot for many companies. Combining both the production and servicing business lines, roughly half of mortgage companies stayed profitable in the third quarter of 2023. Were it not for mortgage servicing, only about one in three companies would have been profitable.”

MBA's Mortgage Bankers Performance Report series offers a variety of other performance measures on the mortgage banking industry including revenue and cost breakouts, productivity, product mixes for originations and servicing volume, and pull-through rates. Eighty-two percent of the 348 companies that reported production data for Q3 2023 were independent mortgage companies, and the remaining 18% were subsidiaries and other non-depository institutions.