DSNews The homepage of the servicing industry

DSNews The homepage of the servicing industry

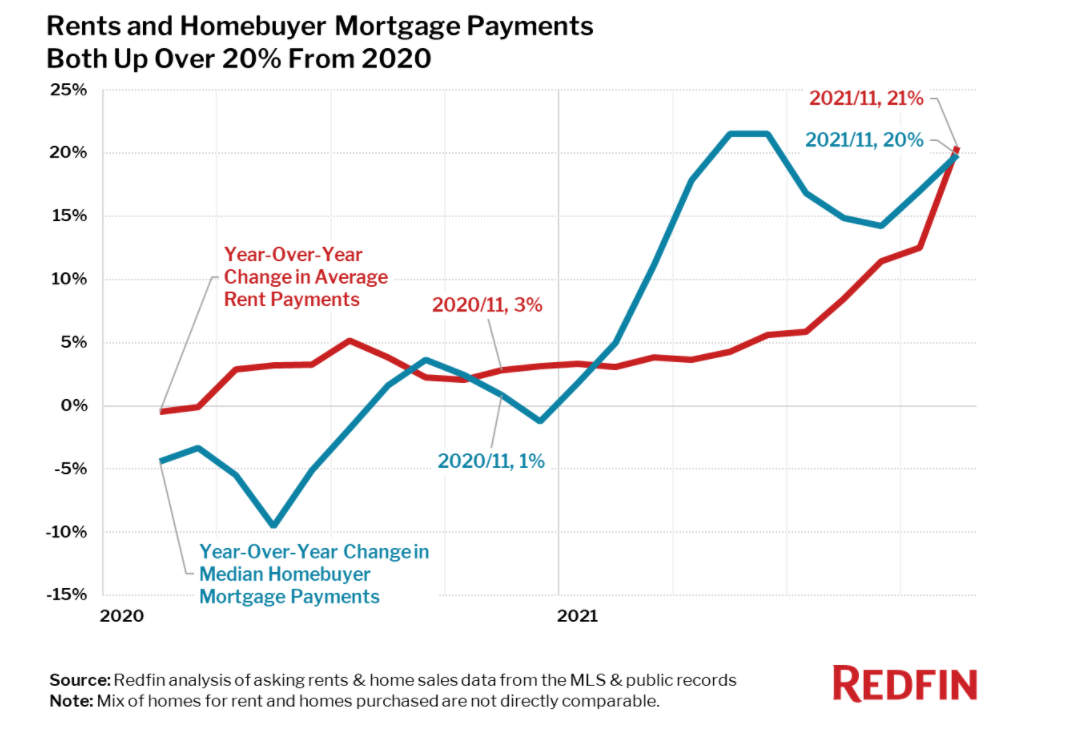

According to a new report from Redfin, average monthly rents in November increased 21% nationwide over the past year and 7% in a single month—resulting in the highest annual and monthly growth rates in the past two years, as far back as Redfin's rental data goes.

According to a new report from Redfin, average monthly rents in November increased 21% nationwide over the past year and 7% in a single month—resulting in the highest annual and monthly growth rates in the past two years, as far back as Redfin's rental data goes.

The national median monthly mortgage payment for homebuyers climbed at about the same annual rate of 20%, and rose just 1% from October. Rapidly increasing housing costs are found to be a large contributor to overall inflation. Percentages hit 6.8% in November, reaching its highest level since 1982. Surging prices for food, energy and shelter costs accounted for much of the increases.

"First inflation came for the for-sale housing market, and now it is coming for the rental market," said Redfin Chief Economist Daryl Fairweather. "Many people have been priced out of the for-sale market and are looking to rent instead, but that demand is pushing up rents. Anyone who bought a home before this year can pat themselves on the back because their mortgage payments are fixed, meaning their biggest recurring expense is immune to inflation.”

Rent-price increases surpassed mortgage payment increases for new homebuyers in 19 of the 50 largest metro areas in the U.S. during November. Areas with the biggest increases in rent prices—up 28% since 2020—were almost exclusively in Florida and New York. The exception is Austin, TX, where rents were up 30%.

The top 10 metropolitan areas with the fastest-growing rents year-over year are:

- Miami, Florida (35%)

- Fort Lauderdale, Florida (35%)

- West Palm Beach, Florida (35%)

- New York, New York (34%)

- Newark, New Jersey (34%)

- Nassau County, New York (34%)

- New Brunswick, New Jersey (34%)

- Jacksonville, Florida (33%)

- Austin, Texas (30%)

- Tampa, Florida (28%)

Only two populous cities saw a decrease in rent in November compared to last year, as rents fell 2% in Kansas City, Missouri (-2.3%) and less than 1% in St. Louis, Missouri (-.03%).

“If you are looking to buy or rent now, there's nowhere to hide from inflation when it comes to housing costs," said Fairweather. "The good news is that the tight labor market means it's a great time to move somewhere more affordable. Chances are good that no matter where you go, you'll be able to find a new job relatively quickly."

Inflation is expected to rise at a dull pace in the coming year and shows no sign of stopping, leading to continuous unpredictable rent prices and monthly housing costs.

Click here to read more on Redfin's latest analysis of nationwide rental prices.