DSNews The homepage of the servicing industry

DSNews The homepage of the servicing industry

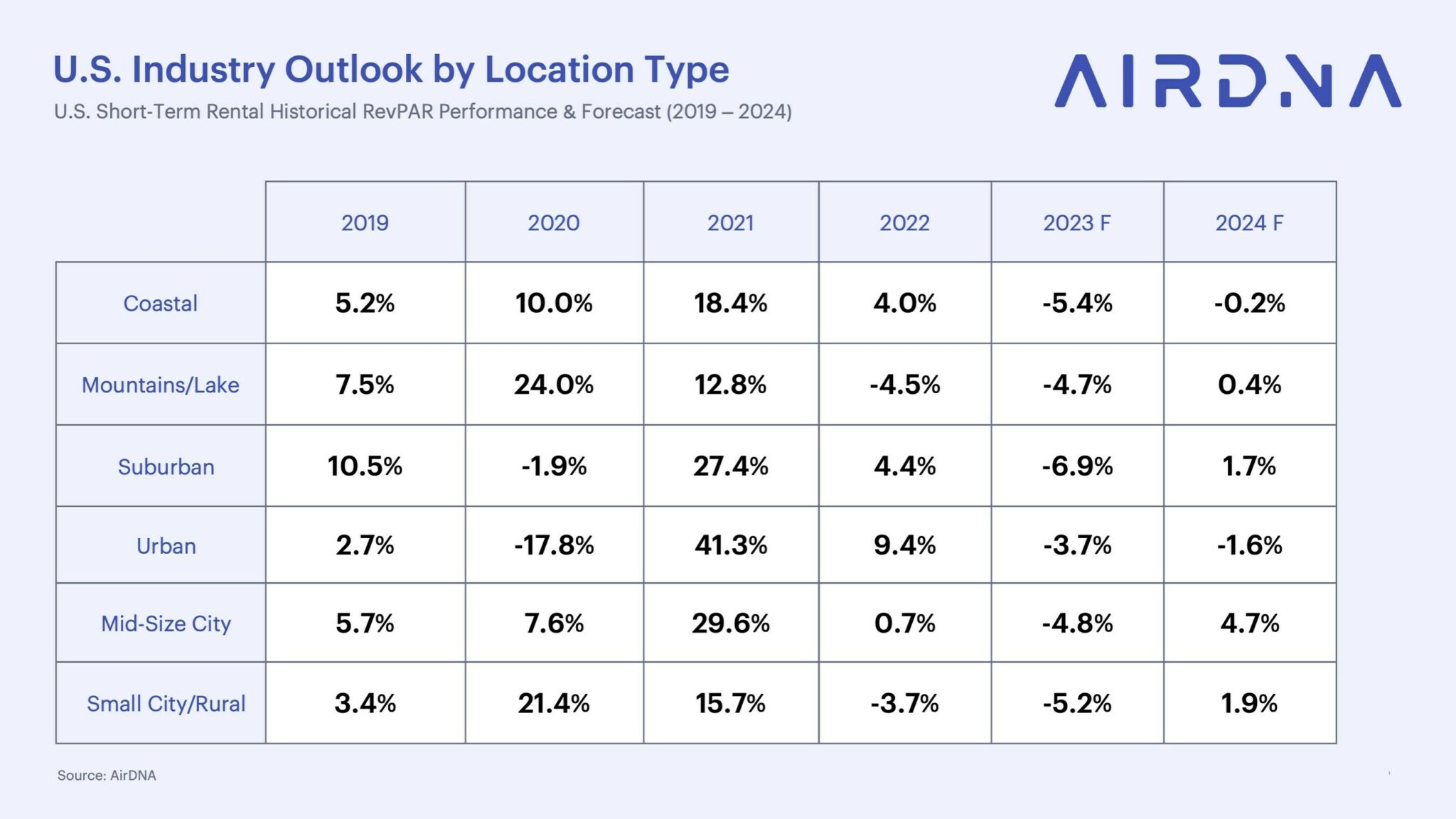

AirDNA, a provider of short-term rental (STR) analytics, has released its 2024 outlook report, forecasting measured growth for the U.S. STR industry in the coming year. Demand is projected to rise by 10.7% year-over-year, surpassing the 6.7% increase in 2023, supported by a stable economic backdrop.

AirDNA, a provider of short-term rental (STR) analytics, has released its 2024 outlook report, forecasting measured growth for the U.S. STR industry in the coming year. Demand is projected to rise by 10.7% year-over-year, surpassing the 6.7% increase in 2023, supported by a stable economic backdrop.

"Heading into 2024, the industry is set for balanced growth with slower supply expansion, anticipated at 10.9%," said Jamie Lane, SVP of Analytics at AirDNA. "While reports of an STR 'collapse' have been greatly overstated, the market's increasing competitiveness demands that hosts and property managers closely follow data trends. This approach will be key to outperforming competitors and maintaining high revenues, capitalizing on a stronger economy and travelers' growing preference for STR lodging."

Despite a record-breaking July 2023 with 24.1 million nights booked and a peak of 1.6 million listings in September 2023, the industry saw its first Revenue per Available Rental (RevPAR) drop of 4.9%.

“Occupancy rates returned to pre-pandemic levels at 54.8%," said Bram Gallagher, Ph.D. Economist at AirDNA. "In response, hosts lowered rates to attract budget-conscious travelers, impacting revenue, but adapting to market shifts. Successful hosts were those who adeptly navigated these changes and maintained high-quality service."

While high mortgage rates and soft per-unit revenue performance have moderated the pace of new listings compared to 2022, the STR market still expanded significantly, leading to a 12.8% increase in the number of available nights in 2023. With more options available, lead times for bookings shortened, meaning travelers waited an additional week to book on average in 2023 compared to the prior year.

When looking ahead to 2024, the report outlined a number of factors that will come into play in the STR marketplace:

- Demand: A year of economic uncertainty and changing international travel patterns slowed demand growth in 2023, to 6.7% year-over-year (YOY). In 2024, economic growth and recovery in domestic leisure travel will reaccelerate demand growth to 10.7%.

- Supply: High mortgage rates and soft per-unit performance have dampened supply growth from the extreme highs of 2022, but perhaps not as much as originally anticipated. Surprisingly strong listing growth in October and a relatively low percentage of listing churn will increase the number of available nights by 12.8% in 2023. Performance will return to long-running averages and bring supply growth back to 10.9% in 2024, striking a better balance with demand.

- Occupancy: Occupancy has been steadily falling since the highs seen in 2021. By the end of 2023, the yearly average will land approximately at the pre-pandemic level of 54.8%. In 2024, balance in supply and demand growth will maintain occupancy at 54.7%, about the same as in 2023.

- Average Daily Rates (ADRs): Inflation-weary travelers looking for affordable options kept rate growth to only 0.5% in 2023. As changes to the price level normalize in 2024, so too will ADR growth. ADRs should increase by about 2.1% in 2024.

- Revenue per Available Room (RevPAR): The significant decrease in occupancy and near-standstill in ADR has caused RevPAR to decline 4.9% in 2023, the first such annual decline we’ve recorded. We can interpret the decline in 2023 as a return to more normal performance after the STR market’s meteoric rise in 2021. The year 2024 will see RevPAR rise by 1.9% thanks to steady occupancy and a 2.1% increase in ADR.

"The alignment of supply growth with rising demand indicates a healthier, more sustainable market dynamic," said Lane. "This equilibrium is a sign of the market's maturity and resilience in adapting to various economic conditions."

Assisting the overall market, 2023’s anticipated recession never materialized, as the Federal Reserve took action to combat inflation, and its efforts seem to have been effective, with inflation dropping from a high of nearly 9% in June 2022, to its current rate of 3.2%.

Economic retraction was also a possibility, but at least two factors have mitigated this effect: diversification and savings. The current economy is more diversified than the last one which experienced inflation rates this high. In addition, considerable excess savings helped to keep spending and employment consistently high throughout 2023.

Click here to access the full 2024 Outlook Report for the STR marketplace.