DSNews The homepage of the servicing industry

DSNews The homepage of the servicing industry

First American Financial Corporation has released its latest iteration of their Real House Price Index (RHPI) for December 2021, which measures the price changes of single-family properties across national, state, and metropolitan areas, which are adjusted based on income, interest rates, and home-buying power. The ultimate goal of this is to provide a clearer picture of housing affordability.

First American Financial Corporation has released its latest iteration of their Real House Price Index (RHPI) for December 2021, which measures the price changes of single-family properties across national, state, and metropolitan areas, which are adjusted based on income, interest rates, and home-buying power. The ultimate goal of this is to provide a clearer picture of housing affordability.

According to First American, the three key points of the First American RHPI are income, mortgage rates and an unadjusted house price index. Incomes and mortgage rates are used to inflate or deflate unadjusted house prices in order to better reflect consumers' purchasing power and capture the true cost of housing.

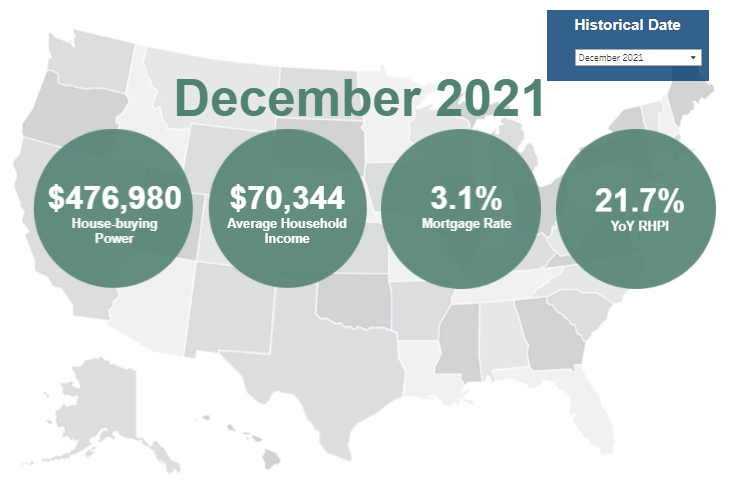

for the month of December, First American found that real house prices increased by 21.7% year-over-year or 1.9% from November 2021. This represents the highest annual growth rate seen since 2014. It also found that the average house now costs $476,980 up $1,800 from $475,180 in November while the average household income is $70,344, up by $537 from $69,807.

“In December 2021, the RHPI increased 21.7% compared with December 2020, the highest annual growth rate since 2014. The record increase was driven by rising mortgage rates and rapid nominal house price appreciation, which make up two of the three drivers of the RHPI,” said Mark Fleming, Chief Economist at First American. “The 30-year, fixed-rate mortgage and the unadjusted house price index increased by 0.4 percentage points and 21.4% respectively.”

“Even though household income increased 5% since December 2020 and boosted consumer house-buying power, it was not enough to offset the impact of higher mortgage rates and rising nominal prices on affordability,” Fleming continued. “In the near term, affordability is likely to wane further, as mortgage rates are expected to continue to rise and the pace of house price appreciation exceeds gains in household income. How buyers and sellers react to higher rates may help the housing market regain some balance.”

Late last year, the Federal Reserve signaled through a series of monetary moves that interest rates will be rising this year in the face of declining affordability and rising inflation. This period of “easy money” could end as soon as March. Still, mortgage rates remained flat between November and December, sitting at 3.1%.

“When mortgage rates fall, a potential home buyer can buy the same amount of home for a lower monthly payment or buy more home for the same monthly payment. The 40-year tailwind of declining mortgage rates has allowed homeowners to buy a home at one mortgage rate and then later sell and move into a more expensive home when rates are lower,” said Fleming. “This long-run decline in mortgage rates has encouraged existing homeowners to move out and move up.”

“Faster house price appreciation, modestly rising mortgage rates and record low levels of homes for sale have been the economic dynamics dominating the housing market during the second half 2021. While existing homeowners have historically high levels of equity and may feel wealthier because of it, many have also secured historically low fixed-rate mortgages,” said Fleming. “There is a financial ‘lock-in’ effect that increases as mortgage rates rise and as the size of a mortgage increases. Rising mortgage rates increase the monthly cost of borrowing the same amount that a homeowner owes on their existing mortgage. The higher the prevailing market mortgage rate is relative to the homeowner’s existing mortgage rate, the stronger the lock-in effect. Why move out and move down?”

“Additionally, the record low level of houses for sale makes it difficult to find a better, more attractive house to buy, so sellers—who are also prospective buyers—don’t sell for fear of not finding something to buy,” said Fleming. “The good news is that builders have been breaking ground on more new homes, which may alleviate some of the supply crunch and encourage existing buyers to move.”

“Nonetheless, buying a home is often prompted by lifestyle decisions more so than financial considerations,” said Fleming. “Despite the financial lock-in, homeowners will still make the decision to move based on lifestyle changes, such as needing more space to accommodate a growing family or relocating for a new job or other reason.”

Fleming continued that buyers will continue to see challenges in the market in 2022, he believes that the market will eventually adjust.

“Homeowners may feel rate-locked into their homes, but first-time home buyers have no such financial lock. Yet, first-time home buyers must also contend with the record low supply of homes in a declining affordability environment. But what goes up, must eventually moderate,” said Fleming. “Rising rates may be a housing market headwind in 2022, but as some buyers pull back from the market due to affordability and supply constraints and as new construction adds more supply, house prices will moderate, resulting in a more balanced housing market.”

Other highlights found by the report include:

- Consumer house-buying power, how much one can buy based on changes in income and interest rates, increased 0.04 percent between November 2021 and December 2021, and decreased 0.2% year over year.

- Median household income has increased 5.2% since December 2020 and 69.3% since January 2000.

- Real house prices are 4.8% less expensive than in January 2000.

- While unadjusted house prices are now 44.5% above the housing boom peak in 2006, real, house-buying power-adjusted house prices remain 33.2% below their 2006 housing boom peak.

- The five states with the greatest year-over-year increase in the RHPI are: Arizona (+34.3 percent), Florida (+32.0), South Carolina (+29.4 percent), Connecticut (+28.6 percent), and Georgia (+28.4),

- There were no states with a year-over-year decrease in the RHPI.

- Among the Core Based Statistical Areas (CBSAs) tracked by First American, the five markets with the greatest year-over-year increase in the RHPI are: Phoenix (+36.3 percent), Charlotte, N.C. (+36.0), Tampa, Fla. (+32.9 percent), Raleigh, N.C. (+31.5 percent), and Atlanta (+31.5 percent).

- Among the Core Based Statistical Areas (CBSAs) tracked by First American, there were no markets with a year-over-year decrease in the RHPI.