DSNews The homepage of the servicing industry

DSNews The homepage of the servicing industry

According to the redesigned J.D. Power 2022 U.S. Mortgage Servicer Satisfaction Study released today, customer satisfaction suffers when there is a lack of trust in the servicer. As a recession seems increasingly likely and mortgage loan delinquencies are on the rise, customers want to be assured their mortgage servicers are on their side.

"Mortgage servicing has always been an opaque experience for customers with the firms originating, owning and servicing the loans often being different and changing over time,” said Craig Martin, Executive Managing Director and Global Head of Wealth and Lending Intelligence at J.D. Power. “In a time when brand reputation, customer trust and customer satisfaction are going to be even more critical for attracting and retaining business, different business models will be put to the test in different ways. Managing to the average is dangerous. Firms that are selling the value of the end-to-end relationship and working to build customer advocates will not succeed if they are satisfied with only being technically proficient. Even for firms primarily focused on sub-servicing—an area where compliance, efficiency and resource optimization are paramount—it’s critical to realize that customer perceptions heavily influence actions and, as a result, affect the bottom line.”

Key findings of the 2022 study:

- Loan transfers hurt satisfaction, erode trust for all parties: Overall customer satisfaction for mortgages that are originated and serviced by the same company is 646 (on a 1,000-point scale). That number drops 133 points to 513 when the mortgage is transferred to a servicer that is different from the originator. Likewise, customer trust in the mortgage servicer falls 145 points to 511 when a loan is transferred vs. those that are originated and serviced by the same company. Critically, the originating firm that made the transfer is affected, too, with only 15% of transferred customers saying they are “very likely” to consider using the original lender in the future.

- Going paperless? Trust matters: More than half (52%) of mortgage servicing customers get a paper statement, but 43% of those customers say their primary means of reviewing their statement is via digital channels, so the paper bill isn’t used. The disconnect often goes back to trust. Among customers who have gone paperless, brand image attributes are rated significantly higher, including “can rely on lender to keep promises” and “lender provides honest communication,” compared with those who do not receive paperless statements. Among those who say they “never will” go paperless, the same brand image attributes are rated significantly lower. Servicers need to understand which customers are open to going paperless and what it will take to convert them.

- Transfers create administrative headaches for customers: More than four in 10 mortgage customers who had a loan transferred say the transfer process was not “very easy.” Among this group, problem incidence is substantially higher (27%) than the problem incidence among customers who say the process was “very easy” (12%). When the transfer process is perceived as “very easy,” satisfaction is 183 points higher than when the process is “somewhat easy,” “somewhat difficult” or “very difficult,” these customers are significantly less likely to need to interact with a live representative. Servicers need to be sure sufficient servicing information is sent from the beginning to better ensure a “very easy” transfer process to improve the customer experience and reduce call volume.

“Transparency has become the financial services industry’s favorite buzzword for a reason: customers respond favorably when brands communicate their intentions and provide clear guidance on what is happening and why,” said Tom Lawler, head of consumer lending intelligence at J.D. Power. “The complexity of the mortgage industry creates challenges in customer understanding, particularly when it comes to mortgage transfers. We’re entering a market environment where customer satisfaction is going to play a critical role in the success of mortgage brands, and transparency will be a big part of creating the trust that will determine business success.”

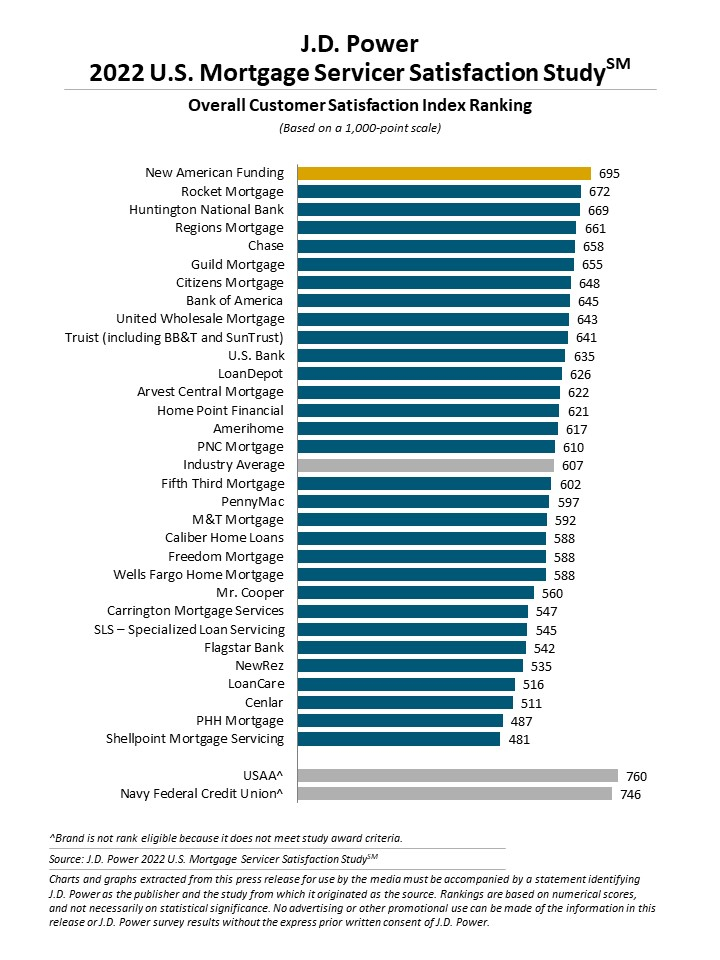

New American Funding ranks highest among mortgage servicers with a score of 695. Rocket Mortgage (672) ranks second and Huntington National Bank (669) ranks third.

Read the full press release here.